CIBC Mortgage Rates & Reviews

CIBC Background

CIBC (TSE: CM) is one of the largest banks in Canada in terms of assets and market capitalization, with a market cap of approximately $80 billion as of October 2024. CIBC is one of Canada’s Big 5 banks, making it a tier 1 bank as well. In 1961, the bank was formed through one of the largest chartered bank mergers in Canada, which was between The Canadian Bank of Commerce (established in 1867) and the Imperial Bank of Canada (established in 1874). Today, CIBC has operations around the world including in Canada, the United States, the United Kingdom, Asia and the Caribbean. CIBC provides a diversified portfolio of financial services to customers, including retail banking, commercial banking, wealth management, capital markets, and insurance. In total, CIBC has over 1,000 branches worldwide and over 48,000 employees, helping the bank to serve over 14 million customers around the world. CIBC is the leader among big banks in Canada when it comes to digital adoption rate, with CIBC’s digital adoption rate being 86% in Q1, 2024.

CIBC Fixed Mortgage Rates

A CIBC fixed rate mortgage reduces the risk of future interest rate fluctuations by allowing you to lock-in a specific interest rate for the entire term of your mortgage. This can give you peace of mind knowing that your interest payments will not increase over your mortgage term, which makes it fundamentally appealing to many new home buyers. If you are arranging a new mortgage for a future or current home, your fixed interest rate can be guaranteed for up to 120 days before the closing date of your home. If interest rates go up during that time, you will still be guaranteed the lower rate.

| Term | CIBC Rate | Lowest Rates of Big 6 Banks |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

CIBC Variable Mortgage Rates

A CIBC variable rate mortgage will still give you fixed payments over your mortgage term; however, the interest rate will fluctuate with any changes in CIBC’s prime rate. If the prime rate goes down, more of your payment will go towards paying off your principal balance, while if the prime rate goes up, more of your mortgage payment will go towards interest costs. As a result, this can be a good way to benefit if you are expecting interest rates to fall in the near future. A similar option to benefit from a fall in interest rates is a convertible mortgage. This is a variable rate mortgage that allows you to convert your mortgage terms to a fixed rate mortgage at any time in the future. This feature provides you the security of being able to lock in a fixed interest rate over your term, while providing you the flexibility to benefit from a fall in interest rates.

| Term | CIBC Rate | Lowest Rates of Big 6 Banks |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

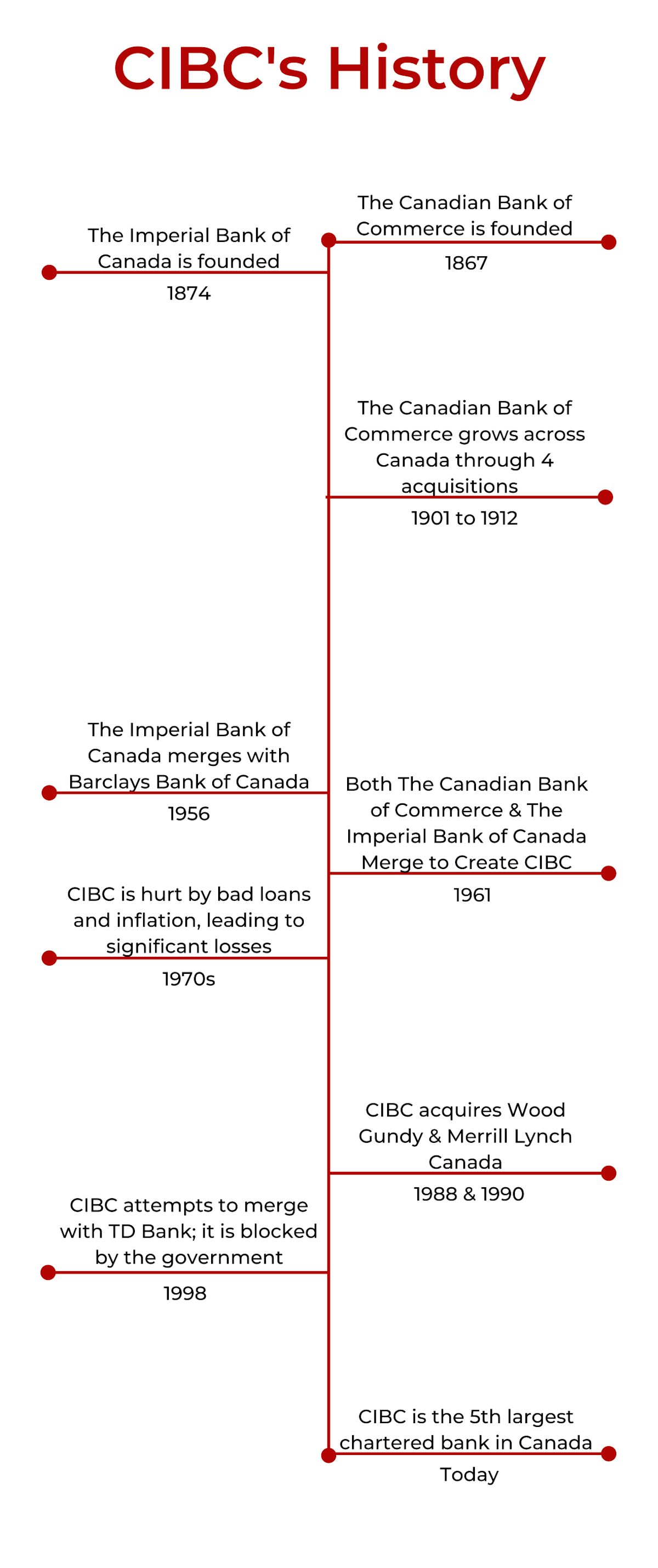

CIBC’s History

Inception - 1920s

The Canadian Bank of Commerce, which is one of the two banks that merged in 1961 to create CIBC, was founded in 1867. The Imperial Bank of Canada, the other bank that was part of the merger to create CIBC was founded in 1874 by a former VP at The Canadian Bank of Commerce. Both these banks continued to grow throughout the late 1800s in size, offerings, and locations. The Canadian Bank of Commerce grew faster than the Imperial Bank in the early 1900’s through acquiring other banks across Canada, including The Bank of British Columbia, The Bank of Halifax, and The Merchants Bank of PEI.

1920s - 1990s

As the 1920’s came around, The Canadian Bank of Commerce continued to purchase more banks across Canada. At the same time, The Imperial Bank of Canada decided to grow organically rather than by acquisition, leading to it being much smaller than The Canadian Bank of Commerce. In the 1950s as growth slowed for banks in Canada, The Imperial Bank of Canada merged with The Barclays Bank of Canada. Then in 1961, both The Canadian Bank of Commerce and The Imperial Bank of Canada merged to become The Canadian Imperial Bank of Commerce (CIBC), which was the 2nd largest bank in Canada at the time. In the 1970’s, CIBC struggled to operate in an environment with high inflation, as the bank had many bad loans. CIBC ended up being one of the most hurt banks over this period.

1990s - Today

During the 1990s, CIBC was back on the acquisition trail by purchasing Wood Gundy and Merrill Lynch Canada, while getting into asset management by acquiring a stake in TAL Investment Counsel. In 1998, CIBC attempted to merge with TD Bank, however this merger was blocked by the government. CIBC considered another large merger with Manulife Financial in 2002, however the talks failed with both parties not expecting to gain government approval. In 2010 to the present, CIBC has acquired multiple wealth management firms and has looked to expand its business in the US.

CIBC Posted Rates

CIBC posted rates are the official rates used when calculating your mortgage break penalty, which is the fee you pay if you break or refinance your mortgage early. Your mortgage payment, interest, and stress test will usually be based on a different rate however, which is usually lower than the current posted rate.

How Are Posted Rates Used to Calculate a Mortgage Break Penalty?

Similar to other banks and lenders in Canada, CIBC uses a method called an interest rate differential to calculate a mortgage break penalty. This method uses the difference between your current mortgage rate minus any discounts, and the posted interest rate closest to the length of time remaining on your mortgage term. This difference is then multiplied by your mortgage amount and the time remaining on your mortgage to get how much you will owe for a mortgage break penalty. If this amount is more than 3 months worth of interest at your current interest rate, then it will be the amount you will pay. If not, you will pay 3 months worth of interest instead as your mortgage break penalty.

You have $100,000 left on a mortgage with 2 years left on your term and an interest rate of 3.5%. The posted interest rate for a 2 year-term is 2.89%. This means that the difference between your interest rate and the posted rate for a 2 year term is 0.61%. This means that to find your mortgage break penalty, you will multiply 0.61% by how much is left on your mortgage, which is $100,000, and also by how many months are left on your mortgage, which is 24 months. This will result in you having to pay a mortgage break penalty of $1,220.

CIBC Mortgage Break Penalty

| Bank or Lender | Variable Rate Mortgage | Fixed Rate Mortgage |

|---|---|---|

| 3 Months’ Interest (at the CIBC Prime rate) | Greater of 3 Months’ Interest (at your current mortgage rate) or the IRD amount |

Difference in interest payable between the interest amount that you owe between the time of payment to maturity, calculated using your current mortgage rate plus any rate discount that you received, and the interest amount that you owe between the time of payment to maturity, calculated using CIBC’s current posted rate for a comparable mortgage.

Are you looking to pay off your mortgage early? Or refinance the terms of your mortgage at a lower interest rate? Maybe you sold your home. Whatever the case, you most likely will have to pay a mortgage break penalty set by your lender. Whatever the situation, our calculator will help you determine the cost to break your mortgage so you can be confident about your mortgage decisions.

What is the remaining balance on your mortgage?

What is your current regular mortgage payment amount?

What is the term-length and type of your current mortgage?

What is your current mortgage interest rate?

If applicable, what was the rate discount you received when you signed your current mortgage agreement?

When did your current mortgage start?

Is the Property:

Who is your current mortgage lender?

What is CIBC's current interest rate for a 1-year fixed rate mortgage?

What would you like to do?

Please complete all fields before calculating.

By using the calculator, you agree to our Terms of Service

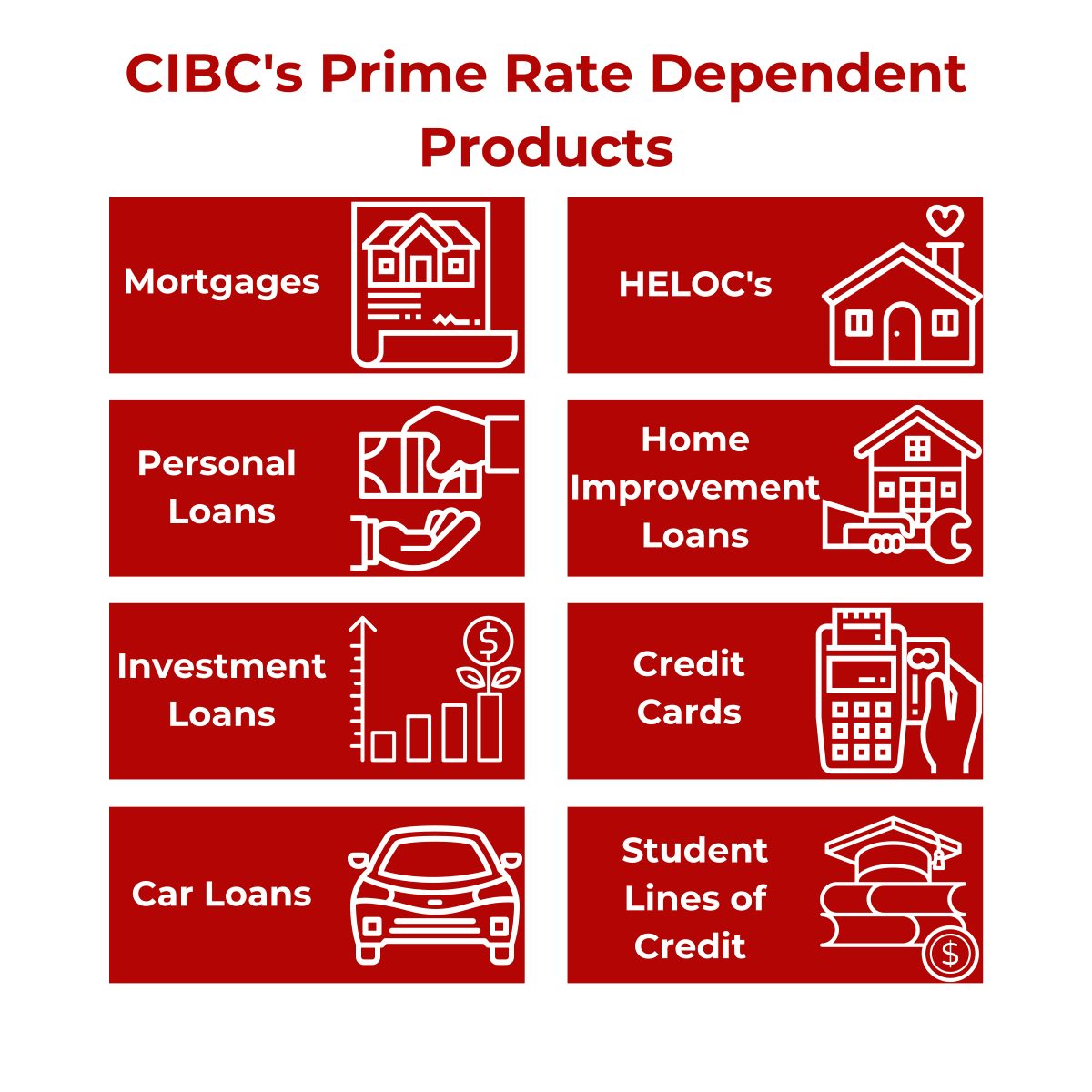

The CIBC prime rate is used as the basis for most of CIBC's lending products, including mortgages, HELOCs, home improvement loans, personal loans, credit cards, investment loans, student lines of credit, car loans, and many other products. The prime rate is normally combined with a spread to make up the final interest rate on a credit product. This spread is usually added in addition to the prime rate, especially for higher-risk loans such as credit cards, car loans, and personal loans. However, some loans may have a spread subtracted from the prime rate, which is more common with lower-risk loans and loans with collateral, such as a mortgage.

Other CIBC Mortgage Products

If you are new to Canada and have very limited or no Canadian credit history, CIBC offers 3 types of mortgage solutions:

Mortgages for Newcomers

- CIBC Newcomers to Canada Mortgage Program: This helps you to purchase a home if you have limited credit history in Canada. To qualify, you will need to meet the required income needed to purchase a home and to afford mortgage payments.

- CIBC Newcomers to Canada Mortgage Plus: This helps new citizens and those moving from abroad to Canada to purchase a home with a mortgage. You can qualify with limited or no credit history in Canada.

- CIBC Foreign Workers Program Mortgage: This is a mortgage for people with a valid work permit in Canada, where you may qualify with little to no Canadian credit history.

CIBC Vacation Property Mortgage

If you are interested in purchasing a vacation property where you can spend time throughout the year, CIBC offers second mortgages to help you make this dream a reality. If you are planning on living in the property as your permanent residence or if a family member is living in the property, you will be eligible for mortgage insurance. This would allow you to purchase with as little as a 5% down payment. If not, you will need a minimum down payment of 20%. If you already own a home, however; you may be able to leverage the equity in that property to cover the cost of a down payment for a vacation home.

One factor to consider besides the cost of a down payment is your ability to pass the mortgage stress test. This means you will need enough income to cover the mortgage payments and other associated expenses for the vacation home while having a GDS and TDS ratio below 39% and 44%. If you are currently making mortgage payments for your principal residence, they will also be accounted for in the TDS and GDS calculations. If you plan on renting out the vacation property when you are not using it, you may be able to include the income earned from rent in your mortgage stress test.

Investment Property Mortgage

Depending on if you plan on occupying part of the income property and making the property your primary residence, you may be able to get mortgage insurance which would allow you to put as little as 5% down. If not, then you will need a minimum downpayment of 20%. Purchasing an investment property to rent out can be a good way to have your money work for you, benefiting both through the rent that the property earns and potentially through property appreciation.

Factors To Consider When Purchasing An Investment Property

Price: What you end up paying for the property in relation to what other properties in the neighbourhood sold for, and what the capitalization rate of the property is will be important when determining if it is a good investment or not. A capitalization rate, which is commonly referred to as a “cap rate”, is the operating income the property produces, divided by the purchase price. The higher a cap rate is, the higher the potential returns from renting the property out are. However, a higher cap rate may be due to reasons such as a property not being in good shape or being located in an undesirable neighbourhood.

Expenses: Common expenses you can expect to have for an investment property include:

- Maintenance and repair costs,

- Property management expenses if you do not manage the property yourself, and administrative costs,

- Home insurance, and

- Property taxes

Location: Considering that a property can always be repaired or renovated to fix structural and cosmetic problems, a property's location is the most important factor in choosing a good investment property. When you are deciding on a location to purchase a property, it's important to consider the nearby amenities, neighbourhood crime rates, jobs in the area, and access to public transportation. Finding a property in a good location will not only be easier to rent out but will be more likely to appreciate in value.

Cash Back Mortgage

CIBC may offer cashback deals on mortgages from time to time, such as a 5% cashback up to a certain limit. As of October 2024, while CIBC isn’t offering a cashback mortgage, it is offering a cashback of up to $3,500 on select new mortgages and up to $4,500 when you switch to a CIBC mortgage. Depending on your eligibility and your mortgage terms, you may be able to get cash back when you get your mortgage. This cash may be used for anything, including covering closing costs, renovating your home, maintaining a savings buffer, or even consolidating your debts.

Pros & Cons of A Cashback Mortgage

| Pros | Cons |

|---|---|

| More financial flexibility to maintain an emergency fund, cover expenses or do renovations. | You may get worse mortgage terms or a higher mortgage interest rate with a cash back mortgage. |

| Can help save you money on interest costs by using it to consolidate higher interest debts. | It will mean a larger mortgage, causing you to have a mortgage longer. |

CIBC Mortgage Features

CIBC Mortgage Protection Insurance

As an add-on option to your mortgage, CIBC offers the ability to purchase mortgage protection insurance when you sign for your mortgage. Mortgage protection insurance will cover some or all of your mortgage balance if something bad is to happen to you depending on your coverage, with options for coverage being for critical illness, death, or a disability. This makes it a good peace of mind expense especially if you are a first time home buyer or have a large mortgage amount. CIBC does not underwrite the insurance, rather they offer mortgage protection insurance through Canada Life Insurance. For mortgage life insurance, which is the most common form of mortgage protection insurance, the maximum amount of coverage you are able to get for a mortgage is $750,000, with monthly premiums calculated on a per $1000 basis with the following rates:

| Age | Single Coverage (SC) | Cost for $400,000 in Coverage (SC) | Joint Coverage (JC) | Cost for $400,000 in Coverage (JC) |

|---|---|---|---|---|

| Under 30 | $0.08 | $32 | $0.15 | $60 |

| 30-35 | $0.13 | $52 | $0.22 | $88 |

| 36-40 | $0.20 | $80 | $0.34 | $136 |

| 41-45 | $0.29 | $116 | $0.49 | $196 |

| 46-50 | $0.43 | $172 | $0.68 | $272 |

| 51-55 | $0.64 | $256 | $0.9 | $360 |

| 56-60 | $0.82 | $328 | $1.19 | $476 |

| 61-64 | $0.97 | $388 | $1.62 | $648 |

Note: Premium rates are current as of October 2024

For those looking to get insurance to cover their mortgage in the tragic event that they become critically ill, the monthly rates are the following, and are also calculated on a per $1,000 coverage basis:

| Age | Single Coverage (SC) | Cost for $400,000 in Coverage (SC) |

|---|---|---|

| 18-29 | $0.10 | $40 |

| 30-35 | $0.17 | $68 |

| 36-40 | $0.27 | $108 |

| 41-45 | $0.45 | $180 |

| 46-50 | $0.68 | $272 |

| 51-55 | $1.01 | $404 |

| 56-60 | $1.65 | $660 |

| 61-64 | $2.40 | $960 |

| 65-69 | $2.70 | $1080 |

Note: Premium rates are current as of October 2024

How Does The Acceptance Process Work?

Anyone who is getting a mortgage with CIBC is eligible for insurance coverage as long as they are approved for the mortgage and are approved based on the health questions. Because mortgage protection insurance has a very easy approval process, it is a popular option for people who are unable to qualify for term or life insurance because of health issues. Once you are accepted for coverage with your mortgage, you will have 30 days to cancel the policy risk-free. This means that you can cancel your policy in the first 30 days and get your money back for the period. Mortgage protection insurance is also convenient because you have the option to cancel your policy at any time.

What Are Your Mortgage Protection Insurance Options At Canada’s Major Banks?

| Bank | RBC | TD | Scotiabank |

|---|---|---|---|

| Coverages | Critical Illness, Mortgage Life, and Disability Insurance | Critical Illness & Mortgage Life Insurance | Critical Illness, Mortgage Life, and Disability Insurance |

| Maximum Mortgage Life Insurance Coverage | $750,000 | $1,000,000 | $1,000,000 |

| Bank | BMO | CIBC | National Bank |

| Coverages | Critical Illness, Mortgage Life, Disability, and Job-Loss Insurance | Critical Illness, Mortgage Life, and Disability Insurance | Critical Illness, Mortgage Life, and Disability Insurance |

| Maximum Mortgage Life Insurance Coverage | $750,000 | $750,000 | $1,000,000 |

CIBC Mortgage Prepayment Allowance

You are able to prepay up to 20% of your original mortgage balance every year without a mortgage break penalty. The more mortgage balance you prepay, the less you will owe in interest over your mortgage term. If you do have the ability to prepay more of your mortgage, it is recommended that you do to give yourself added flexibility and to save on these interest payments.

Out of all the major Canadian banks CIBC is tied for having the highest prepayment allowance every year at 20%:

| Bank | RBC | TD | Scotiabank | BMO | CIBC | National Bank |

|---|---|---|---|---|---|---|

| Yearly Prepayment Allowance | 10% | 15% | 15% | 20% | 20% | 10% |

| Bank | Yearly Prepayment Allowance |

|---|---|

| RBC | 10% |

| TD Bank | 15% |

| Scotiabank | 15% |

| BMO | 20% |

| CIBC | 20% |

| National Bank | 10% |

Note: Limits are for closed mortgages and are current as of December 2024. Your actual limit may vary depending on your mortgage agreement.

CIBC Increase Your Mortgage Payment

This feature allows you to pay down your mortgage balance much faster by increasing your CIBC mortgage payment by up to 100% during your term. Every dollar you pay in addition to your regular payment amount will go directly to reducing your principal mortgage balance, meaning you will pay less interest over your term and will pay your mortgage down much faster.

CIBC is not the only bank that offers the ability to pay more towards your mortgage each month, with all 5 other major Canadian banks offering similar terms to help pay down a closed mortgage much faster:

| Bank | Feature |

|---|---|

| RBC | You can pay up to double your mortgage payment amount each payment date, or increase your mortgage payments by 10% every 12 months. |

| TD | You can increase your mortgage payment by up to 100% during a term, without charge once per year. |

| Scotiabank | You can pay up to double your regular mortgage payment amount each payment date. |

| BMO | Permanently increase your regular mortgage payment by up to 20%, once per year. |

| CIBC | You can increase your mortgage payment by up to 100% during the term. |

| National Bank | You can pay up to double your mortgage payment amount each payment date. |

CIBC Increase Your Payment Frequency

You are able to increase how often you pay your mortgage with CIBC. You can adjust your payment schedule to be either monthly, bi-weekly, or weekly. If you decide to adjust your monthly payment to be more frequent, such as from monthly to weekly or bi-weekly, you will save interest over your mortgage term because you are paying down your principal faster.

CIBC Property Tax Payments

Depending on your mortgage agreement with CIBC, you may be required to pay property taxes through CIBC instead of directly. Even if you are not required to pay directly through CIBC, you still will be able to include this in your mortgage agreement. How this works is when you are making your mortgage payments, you will also be required to pay an estimated property tax amount to the bank. This estimate will be based on the information that the municipality provides you on your property tax assessment. This tax amount will then sit in a separate account at CIBC, and when the time to pay your property tax comes, the bank will pay it on your behalf.

Who Will Usually Be Required To Pay Through CIBC?

Factors that CIBC uses to determine who will be required to pay through them include:

- If you are a first time home buyer,

- Your mortgage terms,

- Your credit score and payment history, and

- How large your down payment is

All of these factors go into CIBC’s decision making process. This usually means that younger buyers almost always will be required to pay through CIBC, while older buyers who have more equity and more homeownership experience will have the option to pay property taxes themselves.

Why Does CIBC Require Most Mortgage Holders to Pay Through Them?

The reason that CIBC puts this into most mortgage contracts is because of the costs and risks associated with having individuals pay themselves. If someone either forgets or doesn’t budget for property tax payments in advance, the city will put a lien on the home until the property tax payments are made. This lien would need to be paid before the bank took possession of the property in the event that the mortgage goes delinquent. By having you pay through them, the risk of this happening goes down. CIBC is not the only bank to require most people to pay property taxes through them, with all other major Canadian banks having similar policies.

Pros & Cons of Paying Property Tax Through CIBC

| Pros | Cons |

|---|---|

|

|

CIBC Mortgage Documents Needed

When you are getting a CIBC mortgage you will need to get certain information and documents for the approval process. This can include:

- Employment & Income Verification:

- Recent pay stubs,

- Notice of Assessment and a T1 General, and

- Previous employment information

- Confirmation of a down payment

- Savings or investment statement from the last 90 days, or

- The sale agreement from another property, or

- A gift letter

- Basic financial information

- Assets and liabilities list,

- Bank account and transit number, and

- A CIBC pre-approval certificate (if applicable)

- Property details

- Copy of the listing and purchase and sale agreement,

- Properties full address,

- Property tax estimates, and

- Your lawyer’s name and contact details

- Canadian home insurance policy

Getting these documents together before meeting with CIBC can help you to be prepared for getting a mortgage.

CIBC Mortgage Contact

With a large branch network, online applications, and over the phone mortgage advice, CIBC provides you with many ways to get a mortgage. If you would like to learn more over the phone, CIBC’s mortgage phone line is 1-866-525-8622. If you would prefer to speak to someone in person at one of the over 1,000 CIBC branches, you can find one through the CIBC branch locator. Once you find a branch nearby, you are able to learn more about the offerings the branch has, including the services that are provided, the languages that are spoken at the branch, and the hours of operation. As well, each branch will list the mortgage advisors names and contact information once you click on it, along with a button to book a bank appointment. However, all CIBC branches have the same financial institution number of 010.

CIBC Mortgage Reviews

After finding out more about CIBC and the level of services and offerings the company offers to customers, we have compiled a pros and cons list of getting a mortgage with CIBC, along with some data about user reviews for CIBC.

InsurEYE: 3.7/5 for 47 reviews

| Pros | Cons |

|---|---|

| Full service bank with over 1,000 branches to discuss your mortgage options at. | Potentially higher interest rates on mortgage products. |

| Variety of credit products and mortgages to help meet all your banking needs. | No mortgage feature to pause your monthly mortgage payment, unlike other major banks. |

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.