BMO Mortgage Rates & Reviews

Bank of Montreal Background

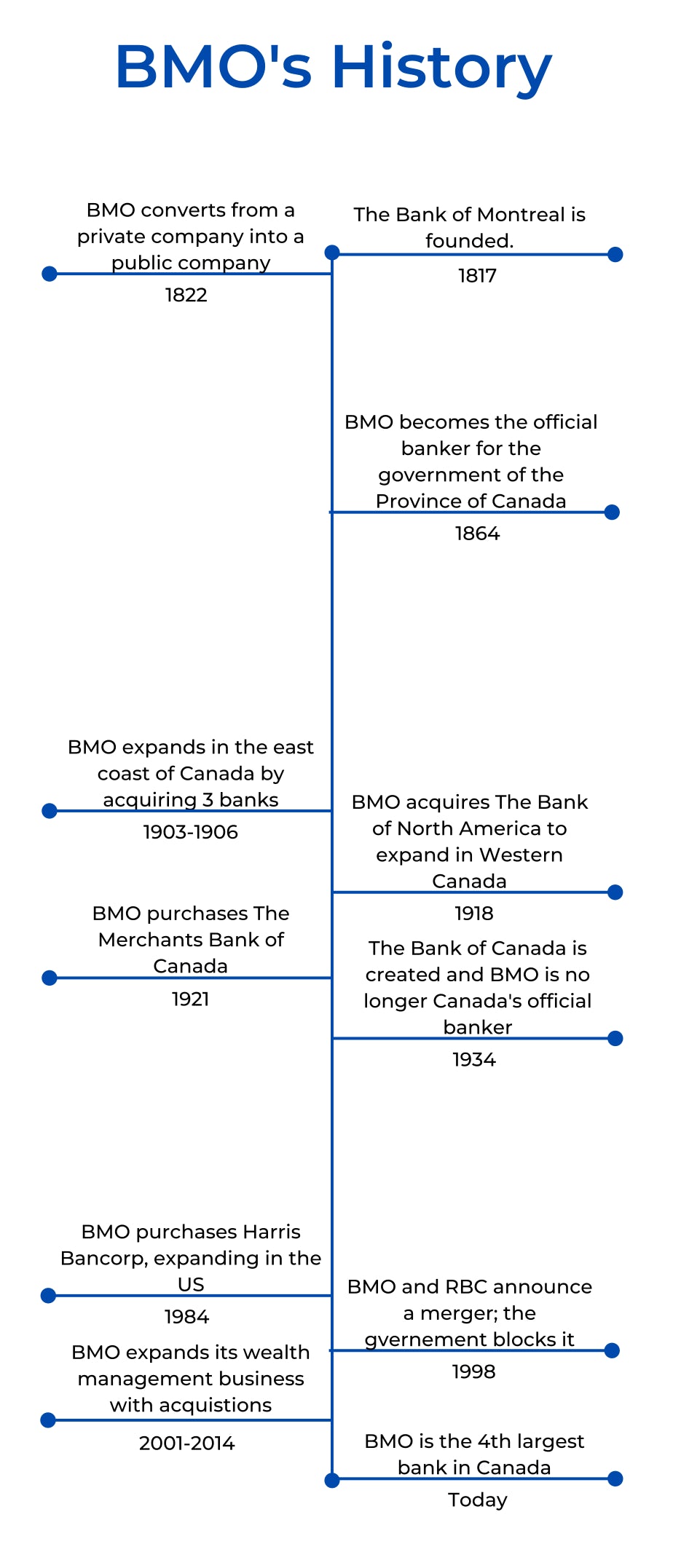

The Bank of Montreal (TSE: BMO) is the fourth largest bank in Canada in terms of market cap and is recognized as one of the Big 5 banks in Canada. BMO is known as a tier 1 bank,

BMO Fixed Mortgage Rates

A BMO fixed rate mortgage protects you from the risk of future interest rate fluctuations, by allowing you to keep your current BMO mortgage rate for the life of your mortgage term. This can give you peace of mind knowing that even if the BMO prime lending rate changes, you will still have the same interest rate. If you are arranging a new mortgage for a future or current home, your BMO fixed interest rate can be guaranteed for up to 130 days before the closing date of your home. If interest rates do go up during that time period, you will still be guaranteed the lower rate.

| Term | BMO Rate | Lowest Rates of Big 6 Banks |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

BMO Variable Mortgage Rates

A BMO variable rate mortgage will provide you with the stability of having fixed payments over your mortgage term; however, the interest rate will move with any changes to the BMO prime rate. If the bank prime rate BMO offers goes down, more of your payment will go towards paying off your principal. However, if BMO’s prime rate goes up, more of your payment will go towards your interest costs. As a result, this can be a great financial tool for those expecting BMO rates to fall in the upcoming year. Another option that gives you the ability to have a variable rate mortgage while letting you convert to a fixed rate mortgage at any time is a convertible mortgage. This will give you both security and flexibility, as it lets you convert to a fixed term should BMO variable mortgage rates no longer meet your needs.

| Term | BMO Rate | Lowest Rates of Big 6 Banks |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

BMO History From 1817

BMO Mortgage Break Penalty

| Bank or Lender | Variable Rate Mortgage | Fixed Rate Mortgage |

|---|---|---|

| 3 Months’ Interest | Greater of 3 Months’ Interest or the IRD amount |

IRD is one way to calculate a penalty for paying off a mortgage early. It is calculated based on your current mortgage rate and the interest rate the lender will charge for a new mortgage with a term similar to the time remaining on your mortgage. It is calculated using BMO’s current posted rate for a comparable mortgage, reduced by any rate discount that you received.

To see how much you can expect to pay in prepayment charges, utilize the BMO mortgage penalty calculator below:

Are you looking to pay off your mortgage early? Or refinance the terms of your mortgage at a lower interest rate? Maybe you sold your home. Whatever the case, you most likely will have to pay a mortgage break penalty set by your lender. Whatever the situation, our calculator will help you determine the cost to break your mortgage so you can be confident about your mortgage decisions.

What is the remaining balance on your mortgage?

What is your current regular mortgage payment amount?

What is the term-length and type of your current mortgage?

What is your current mortgage interest rate?

If applicable, what was the rate discount you received when you signed your current mortgage agreement?

When did your current mortgage start?

Is the Property:

Who is your current mortgage lender?

What is BMO's current interest rate for a 1-year fixed rate mortgage?

What would you like to do?

Please complete all fields before calculating.

By using the calculator, you agree to our Terms of Service

BMO Posted Rates

BMO’s posted mortgage rates are the official rates the bank will use when determining your mortgage break penalty, which is the fee you will pay if you want to break or refinance your mortgage early. However, banks usually offer deals and will leave room to negotiate when you are actually getting a mortgage. Therefore, the actual payments, interest, and mortgage stress test are typically based on a different BMO mortgage rate that is usually lower than the posted rate.

| Term Length | BMO Posted Rate |

|---|---|

| 1-Year Fixed | 5.49% |

| 2-Year Fixed | 4.89% |

| 3-Year Fixed | 6.05% |

| 4-Year Fixed | 5.99% |

| 5-Year Fixed | 6.09% |

| 6-Year Fixed | 6.29% |

| 7-Year Fixed | 6.40% |

| 10-Year Fixed | 6.80% |

BMO Readiline®

The BMO Homeowner ReadiLine product is a combination of BMO’s mortgage and BMO’s HELOC. You can borrow up to a total of 80% of your home's value between a mortgage and a line of credit. If you made at least a 20% down payment or have built equity in your home already, you can get a ReadiLine and borrow from the equity over 20%. One of the features of Homeowner ReadiLine is that your HELOC's credit limit automatically increases as you make mortgage payments, allowing you to quickly tap into your home equity as you pay down your mortgage. Another benefit of BMO’s Homeowner Readiline is your ability to make interest-only payments on the line of credit, which can provide you flexibility in how you use this line of credit.

With ReadiLine using the equity in your home to offer a lower interest rate, you are able to use the money in many ways, with options such as:

- To consolidate higher interest debts,

- Renovate your home,

- Invest in other assets,

- Cover short term expenses, and

- As a way to pay for education costs

The process to set up your BMO Homeowner Readiline is simple. You can start by meeting with a mortgage advisor for either a new mortgage or to add on a BMO home equity line of credit to your existing mortgage. You will need to provide some documents, such as a government-issued ID and proof of employment, among others, depending on your situation. After you have set up Homeowner Readiline, you will have access to your line of credit through your bank account online or through your BMO bank branch.

Other Bank of Montreal Mortgage Products

BMO Self-Employed Mortgage

If you are self-employed or work a commission based job, you will have the same options as someone who is not self-employed. However, the main difference will be the documentation that you need to get a self-employed mortgage. In addition to the standard documents that everyone will need to get a mortgage, such as information about the property, and confirmation of a down payment, you will also need the following information:

- Last two years of tax returns,

- Last two years of Notice of Assessments, and

- One of the following documents:

- Audited business financial statements,

- Statement of business activities for your last two tax years,

- Financial statements with a review report done by an accountant, or

- Notice to reader financial statements done by a professional accountant

BMO Investment Property Mortgage

If you are looking to purchase an investment property with a BMO mortgage and are not occupying part of the property as your permanent residence, you will need at least a 20% down payment. However, if you plan on living in part of the property, you may be able to get mortgage insurance and put as little as 5% down. Besides your down payment and how your mortgage will be covered, other things to consider when purchasing an investment property are:

- The Price: While deciding what price you are willing to pay for an investment property, you must consider the returns it will generate. An investment property is usually valued based on comparable properties and off of a calculation called a capitalization rate, which is the operating income a property brings in, divided by the property’s price. The higher the cap rate, the higher the income generated compared to the price you paid for the property. This means that finding a property that has a reasonable cap rate is important and can help you pay down your mortgage quicker and build more equity.

- The Location: Purchasing a property in a neighborhood that is in-demand, safe, and has good amenities and job opportunities will make renting your property much easier, and over time may help the property appreciate in value.

- Your Expenses: As a landlord you will be responsible for many expenses, which may include: property management costs, home insurance, utilities, and property taxes.

BMO US Mortgage

If you are looking to purchase a property in the US as a Canadian, a BMO cross border mortgage can make the process much easier with the ability to leverage your Canadian credit history. This is possible because of BMO’s significant presence in the US. This can be very helpful if you have a limited or no credit history in the US. Without the ability to leverage your Canadian credit history, you may not be able to get a mortgage, or may require a very high down payment. To be eligible for a BMO mortgage in the US, you will need to bank with BMO already. BMO customers have access to both fixed-rate and adjustable-rate mortgage products and a mortgage value of up to $2 million (USD).

Some of the documents you will need to get a BMO mortgage in the US are:

- Your T1 income tax returns and Notice of Assessments,

- Proof of income depending on your income sources, which may include:

- Your last 2 years of T3 & T5 slips for investment income,

- Pay stubs and 2 years of T4 slips if you are a salaried or hourly employee,

- 2 years of business tax returns if you are self-employed, or

- Your most recent retirement letters if you have retired

- Your social insurance number and passport,

- Account statements with your assets, and

- Property tax and home insurance premiums on other properties you own

- Those living and working in the US can provide their US tax, employment and other documents.

BMO Mortgage Features

Accelerating your Mortgage Payments

BMO offers 2 ways to help you pay more money towards your mortgage:

1. Increase Your Mortgage Payments: Every calendar year BMO will allow you to increase your monthly mortgage payment depending on your mortgage terms and conditions. Your regular monthly payment can be increased by up to 20%, while for a BMO Smart Fixed Mortgage, you can increase it by up to 10%. This will help you be mortgage free faster by letting you put more money towards your mortgage balance each month, which will save you money in interest payments over your term.

2. Make a Lump Sum Payment: Another way to allocate more money towards paying down your mortgage balance is by making a lump sum payment, which BMO allows you to do once per year without incurring a prepayment penalty. If you have a regular BMO mortgage, you are eligible to make a lump sum payment for up to 20% of your original mortgage balance, while if you have a BMO Smart Fixed Mortgage, you can prepay up to 10% in a lump sum payment. This will help you pay much less interest, because this lump sum payment will go directly to paying down your mortgage balance.

Increase Your Payment Frequency

You are able to increase the frequency of your BMO mortgage payments, which can help save you interest over your mortgage term. You have three payment frequency options — monthly, bi-weekly, and weekly. You can save money on interest by paying more frequently because you are reducing your mortgage balance more than once per month. This means you will have less of a balance that is accruing interest each month. Over time, this can help you become mortgage-free faster.

BMO Mortgage Protection Insurance

As an add-on feature, BMO offers mortgage protection insurance products such as mortgage life insurance, critical illness insurance, disability insurance, and job-loss insurance. If something happens to you, and the event is covered under insurance, you will get part or all of your mortgage paid off. BMO mortgage protection insurance can give you the peace of mind that if something happens to you, your family will be able to remain in your home. Other benefits of the offerings from BMO are that your payments will not increase over time, and the process of getting covered is much easier than getting a general term or life insurance. Some of the drawbacks of getting mortgage protection insurance are that your coverage will naturally decline as your mortgage balance is paid off and the lack of flexibility in where you can use the insurance payout, as it automatically goes towards paying your mortgage balance.

Property Tax Payments

Your mortgage contract may need to pay your property taxes through BMO every month. This is common across all banks, where you will pay 1/12th of the estimated property tax amount owed on your home to BMO each month, and BMO will use this money to pay your property taxes on your behalf. The reason BMO requires this is to reduce the risk of you not paying your property taxes. If you were to not make your property tax payments, the municipality can place a lien on your property, which will automatically mean the city is to be paid back ahead of your bank in the event you default. In order to protect themselves, BMO will have you pay through them. However, you may not be required to pay property taxes through the bank depending on your mortgage terms. Even if you are not required to pay through BMO, you will still have the option to pay through the bank, which could be beneficial to help you budget and remember your payments.

BMO Mortgage Contact

BMO gives you the ability to get more information about a mortgage either online, in person at one of the 850+ branches in Canada, or over the phone through the number: 1-866-262-1618. If you are unsure about branches close to your location or want to learn more about each branch before making an appointment, the BMO branch locator can help. It will give you the BMO branch hours of operation, features each BMO branch has, directions to the branch, the languages that are spoken at the branch, and the option to book an appointment. Your mortgage payments will be directed to BMO’s institution number 001.

BMO Mortgage Reviews

Using reviews collected from third party websites such as InsurEYE, and WalletHub, we were able to get a better understanding of what it is like getting a mortgage and banking with BMO. Although most reviews are for the Canadian operations, some of these reviews may be related to the BMO Harris bank US operations.

InsurEYE: 3.6/5 from 50 reviews

WalletHub: 2.8/5 from 1,702 reviews

Pros & Cons of BMO

| ✔ Pros | ✖ Cons |

|---|---|

| You can leverage your Canadian credit history to get a mortgage in the US much easier. | Mortgage rates may be higher than other smaller lenders. |

| Extensive branch network with almost 900 locations across Canada make speaking with a representative easy. | Similar to other big banks, BMO mortgage representatives can only show you BMO products, making it harder to compare your options. |

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.