National Bank Mortgage Rates & Reviews

National Bank Background

National Bank may be a good fit for borrowers who want the convenience of a major bank along with a 120-day rate hold, flexible payment options, and specialized mortgage products. Its offerings may be particularly useful for self-employed borrowers, buyers purchasing a second home or cottage, and homeowners who want a readvanceable mortgage through National Bank’s All-In-One account.

Compare National Bank’s current fixed and variable mortgage rates below, including available terms, estimated payments, and how its rates compare with other lenders.

National Bank Fixed Mortgage Rates

With a fixed-rate mortgage, your mortgage rate and scheduled payment remain unchanged for the selected term. This provides payment certainty but can result in a larger prepayment charge if you break the mortgage before the end of the term.

National Bank offers fixed mortgage terms ranging from short-term options to longer terms. Through a mortgage pre-approval, National Bank may hold an eligible borrower’s rate for up to 120 days.

| Term | National Bank Rate | Lowest Rates of Big 6 Banks |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

National Bank Variable Mortgage Rates

With a National Bank variable rate mortgage, the interest rate and scheduled payment can increase or decrease when National Bank’s prime rate changes. As of August 9, 2026, National Bank’s prime rate is currently unavailable. A variable mortgage may benefit from falling interest rates, but borrowers must be prepared for payment increases when the prime rate rises. This means that getting a National Bank variable mortgage can be beneficial if you believe that interest rates won’t increase significantly during your term.

| Term | National Bank Rate | Lowest Rates of Big 6 Banks |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

Today’s National Bank Mortgage Rates

The current best 5-year fixed mortgage rate from National Bank is 4.69%, while its best 5-year variable mortgage rate is 4.10%. National Bank’s lowest mortgage rate is currently 4.10% for a 5-Year Variable mortgage.

About National Bank Mortgages

National Bank Mortgage Prepayment Privileges

National Bank allows borrowers with a closed mortgage to:

- Make one or more lump-sum payments totalling up to 10% of the mortgage’s initial principal each calendar year. Unused annual lump-sum privileges do not carry forward.

- Make additional payments by as much as the amount of your regular payment on each payment date

These options reduce the mortgage principal and total interest cost of the mortgage.

For National Bank’s All-In-One home equity line of credit (HELOC), you can also use Rewards Plan points from an eligible National Bank reward credit card to pay it down.

National Bank Mortgage Prepayment Penalties

National Bank’s mortgage prepayment penalty charge depends on the mortgage type.

- Variable-rate closed mortgage: Three months’ interest.

- Fixed-rate closed mortgage: The greater of:

- Three months’ interest; or

- The interest rate differential, plus one month’s interest capped at $500.

National Bank’s interest rate differential calculation uses its applicable standard rate for a term comparable to the mortgage’s remaining term. In other words, National Bank compares your mortgage rate with the rate it currently offers for a mortgage lasting about as long as the time remaining on your term. When the remaining term falls between available terms, the bank may interpolate between the closest rates.

An open mortgage can be repaid without a prepayment charge.

| Bank or Lender | Variable Rate Mortgage | Fixed Rate Mortgage |

|---|---|---|

| 3 Months’ Interest | Greater of 3 Months’ Interest or the IRD amount |

The interest rate differential method determines your mortgage break penalty by finding the difference between the posted rate for the time remaining on your mortgage, and your current mortgage rate. From there, multiplying the difference between the posted rate and your current rate by the amount of time left on your term will equal your mortgage break penalty.

Are you looking to pay off your mortgage early? Or refinance the terms of your mortgage at a lower interest rate? Maybe you sold your home. Whatever the case, you most likely will have to pay a mortgage break penalty set by your lender. Whatever the situation, our calculator will help you determine the cost to break your mortgage so you can be confident about your mortgage decisions.

What is the remaining balance on your mortgage?

What is your current regular mortgage payment amount?

What is the term-length and type of your current mortgage?

What is your current mortgage interest rate?

If applicable, what was the rate discount you received when you signed your current mortgage agreement?

When did your current mortgage start?

Is the Property:

Who is your current mortgage lender?

What is National Bank's current interest rate for a 1-year fixed rate mortgage?

What would you like to do?

Please complete all fields before calculating.

By using the calculator, you agree to our Terms of Service

National Bank All-In-One

National Bank’s All-In-One HELOC is a readvanceable mortgage. As the borrower repays principal, available credit can increase without requiring a new credit application.

It can consist of:

- A home equity line of credit on its own, or

- A mortgage loan combined with a revolving home equity line of credit

The revolving portion can generally provide access to up to 65% of the property’s value. Total borrowing can reach up to 80% of the property’s value when the HELOC is combined with a mortgage loan.

The All-In-One account currently has a $7 monthly account fee.

National Bank Mortgage for Self-Employed Borrowers

National Bank offers a mortgage option for eligible self-employed borrowers and small-business owners who may not qualify using a traditional income application. To qualify:

- At least two years of self-employment or business ownership

- A record of sound financial and credit management for at least two years

- A down payment starting at 10%

- A property containing no more than two dwelling units, with at least one occupied by the owner

- A maximum property value of $1.5 million

- A maximum loan of $750,000 in the Calgary, Toronto and Vancouver metropolitan areas, or $600,000 elsewhere

The available amount and required documentation depend on the borrower’s income, business structure, credit profile, down payment and property.

National Bank Second-Home Mortgage

National Bank’s second-home program can be used to finance an eligible second residence or cottage in Canada.

It allows maximum financing of:

- Up to 95% for an eligible year-round second home

- Up to 90% for an eligible seasonal property

National Bank Mortgage Protection Insurance

National Bank offers optional mortgage life insurance for eligible mortgage borrowers. Available coverage can include life insurance, disability insurance and critical illness insurance.

Published coverage details include:

- Disability benefits of up to $3,000 per month

- Critical illness coverage of up to $150,000, based on the insured balance

- Life coverage that repays some or all of the insured mortgage balance

Borrowers should review the insurance certificate carefully, since creditor insurance is optional and is separate from mortgage default insurance.

About National Bank of Canada

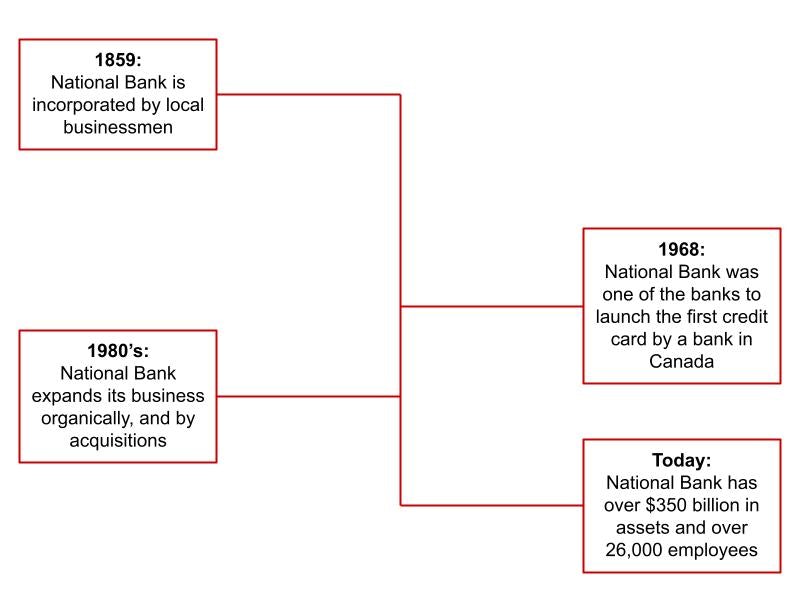

National Bank of Canada was founded in 1859 and is headquartered in Montreal. It is Canada’s sixth-largest bank and provides personal banking, commercial banking, wealth management and financial market services.

National Bank reported n/a in total assets as of its most recently reported quarter, and employs close to 34,000 people. Its acquisition of Canadian Western Bank expanded its client and branch presence in Western Canada.

National Bank History

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.