Stress Test Calculator 2026

Mortgage Stress Test Rates as of July 24, 2026

- Stress Test Rate: The higher of 5.25% and your mortgage rate + 2%

- The lowest stress test rate for insured mortgages (e.g. down-payment < 20%) is: NaN%% (Get This Rate) + 2%=

- The lowest stress test rate for uninsured mortgages (e.g. down-payment ≥ 20%) is: NaN%% (Get This Rate) + 2%=

- The lowest stress test rate for uninsurable mortgages (e.g. home prices ≥ $1.5 M or refinances) is: NaN%% (Get This Rate) + 2%=

What type of home are you looking for?

Enter your average monthly payment. If you have multiple sources of debt, enter the total.

How is my stress-test mortgage payment calculated?

To pass the stress test, you must still be able to afford your mortgage payments if your interest rate increases to a value called the qualifying rate.

The qualifying rate is the higher of:

- The benchmark rate of 5.25%, and

- Your current or target interest rate plus 2%.

5.25%

What You Should Know

- The mortgage stress test checks if you can still afford your mortgage at a higher interest rate

- The stress test rate is the higher of your interest rate + 2% and the benchmark stress test rate (currently 5.25%)

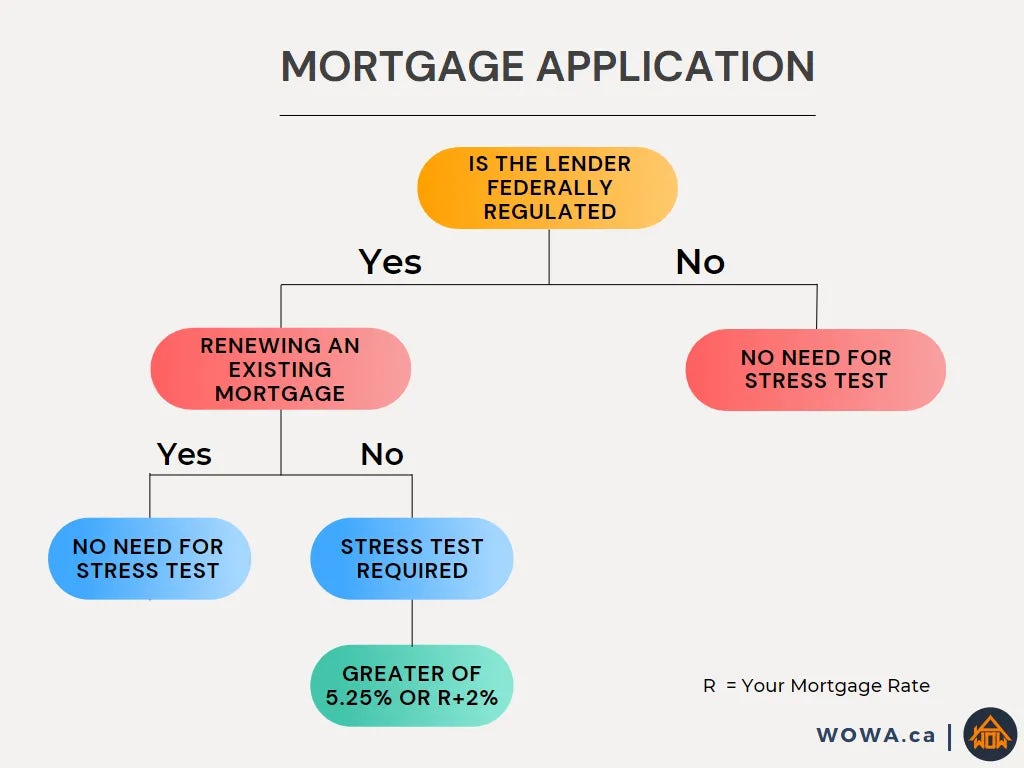

- The stress test only applies to new mortgages and refinancing. Mortgage renewals are exempt.

- Credit unions, B-lenders and private lenders are exempt from the mortgage stress test. However, many credit unions voluntarily conduct their own version of a stress test.

What is a mortgage stress test?

A mortgage stress test is conducted by your mortgage lender to assess whether you could continue to make your mortgage payments if interest rates were to rise. This test helps ensure that you can handle potential increases in borrowing costs.

All federally regulated lenders in Canada—such as banks—are required to perform this test when you:

- Apply for a new mortgage

- Refinance an existing mortgage

How the Stress Test Affects You

The stress test can reduce the amount you qualify to borrow compared to the amount you would be eligible for based on current interest rates. In some cases, it may even disqualify you from getting a mortgage with a federally regulated lender.

Rather than assessing your ability to afford payments at the actual interest rate offered, lenders use a higher qualifying rate—either the floor rate or your contract rate plus 2%, whichever is higher. This ensures a financial cushion in case rates increase in the future.

How is the stress test calculated?

A stress test is calculated by finding out what your mortgage payments would be if interest rates rise to a value called the qualifying rate. This qualifying rate might differ depending on whether your mortgage is insured or uninsured.

If your mortgage is uninsured, then the stress test will be calculated at a qualifying rate which is the higher of

- a floor rate of 5.25%, and

- your current interest rate plus 2%.

If your mortgage is insured, then the qualifying rate is the higher of

- a floor rate of 5.25, and

- your current interest rate plus 2%.

When is a mortgage stress test done?

A mortgage stress test is done when you apply for a new mortgage with a federally-regulated lender. It is also done anytime you refinance your mortgage. A mortgage stress test is not done when you are renewing your mortgage without increasing your mortgage balance or extending your amortization.

How To Avoid The Mortgage Stress Test

Failing a mortgage stress test means that you will be ineligible for a mortgage at any federally-regulated lender. This includes all of the Big Banks in Canada, including RBC and TD.

If you have failed the mortgage stress test, or you are looking to avoid it, you may consider un-regulated lenders, such as private mortgage lenders. Private lenders are not required to conduct a stress test and they are generally more flexible in their lending requirements, such as if you have a bad credit score or if you are self-employed. However, private mortgages come with much higher mortgage rates, even in excess of 10%.

Refinancing your mortgage also means that you will have to undergo another mortgage stress test.

Is a Mortgage Stress Test Needed?

| Mortgage Refinance | Yes |

| Mortgage Renewal | No |

| Not Federally Regulated like Private Lenders | No |

Mortgage Stress Test Breakdown

Debt Service Ratios (GDS/TDS) and Mortgage Affordability

Your mortgage affordability depends on three key factors:

- The size of your down payment

- Your Gross Debt Service (GDS) Ratio

- Your Total Debt Service (TDS) Ratio

What are GDS and TDS Ratios?

- GDS Ratio: This is the percentage of your monthly income that goes toward housing costs—typically your mortgage payment, property taxes, and (half of) condo fees (if applicable).

- TDS Ratio: This includes all your housing costs plus other monthly debt obligations, such as credit card payments, car loans, and student loans—expressed as a percentage of your monthly income.

CMHC Mortgage Insurance Changes (Effective July 5, 2021)

The Canada Mortgage and Housing Corporation (CMHC) updated its policy to ease restrictions imposed in mid-2020 for new insured mortgages. Here are the current qualifying criteria:

- ✅ Minimum credit score of 600

- ✅ Maximum GDS ratio of 39%

- ✅ Maximum TDS ratio of 44%

Note: CMHC does not accept down payments funded through additional debt, such as personal loans. Only traditional sources like savings or gifts are eligible.

Can You Pass the Stress Test?

Use a mortgage stress test calculator to:

- Estimate your GDS and TDS ratios

- Confirm whether your down payment meets minimum requirements

- Determine if you qualify for a CMHC-insured mortgage

CMHC Insurance Requirements

| Minimum Credit Score | 600 |

| GDS Ratio | 39% |

| TDS Ratio | 44% |

| Minimum Down Payment | 5% |

Mortgage Stress Test History

Canada’s Mortgage Stress Test: A Timeline of Evolution (2016–Present)

Over the past eight years, Canada’s mortgage stress test has undergone several key changes aimed at strengthening financial stability and protecting borrowers from rising interest rates. Here's how it evolved:

2016: Introduction for Insured Mortgages

- The federal government introduced the stress test for insured mortgages (those with less than 20% down).

- Borrowers had to qualify at the Bank of Canada’s 5-year benchmark rate, not their actual contract rate.

- Goal: Ensure borrowers could afford payments if rates rose.

2018: Expansion to Uninsured Mortgages

- OSFI (Office of the Superintendent of Financial Institutions) expanded the stress test to uninsured mortgages (20%+ down).

- Borrowers had to qualify at the greater of:

- The benchmark rate (then ~5.34%)

- Their contract rate + 2%

- This move significantly reduced borrowing power and cooled overheated markets.

2020: Proposed Benchmark Rate Reform

- The federal government proposed using a median 5-year fixed insured mortgage rate + 2% instead of the posted rate.

- Intended to make the stress test more responsive to market conditions.

- Implementation was delayed due to the COVID-19 pandemic.

2021: Tougher Rules Implemented

- OSFI raised the minimum qualifying rate to 5.25% for uninsured mortgages.

- This change reduced buying power by ~4–5% for many borrowers.

- The Department of Finance matched the rule for insured mortgages.

2022–2023: No Change Despite Rising Rates

- Despite interest rates climbing above 6%, OSFI kept the stress test unchanged at 5.25% or contract rate + 2%.

- Borrowers were qualifying at rates above 8%, leading to affordability concerns.

- OSFI launched consultations to review the framework.

2024: Major Reform for Renewals

- OSFI removed the stress test requirement for borrowers switching lenders at renewal, provided the loan amount and amortization remain unchanged.

- This addressed long-standing concerns about reduced competition and borrower flexibility.

- The Canadian Mortgage Charter reinforced this change for insured mortgages.

2025 and Beyond: Potential Overhaul

- OSFI is evaluating a Loan-to-Income (LTI) cap as a possible replacement or complement to the stress test.

- Proposal: Limit lenders to issuing no more than 15% of mortgages with debt exceeding 450% of borrower income.

- Decision expected after a full year of testing (OSFI’s ongoing monitoring and evaluation).

Stress Test Mortgage Rate Changes

| Date | Interest Rate | Change |

|---|---|---|

| October 25, 2017 | 4.99% | - |

| January 17, 2018 | 5.14% | +0.15% |

| May 9, 2018 | 5.34% | +0.20% |

| July 10, 2019 | 5.19% | -0.15% |

| March 18, 2020 | 5.04% | -0.15% |

| May 20, 2020 | 4.94% | -0.10% |

| August 12, 2020 | 4.79% | -0.15% |

| June 1, 2021 | 5.25% | +0.46% |

Source: Bank of Canada

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.