Mortgage Life Insurance in Canada

What You Should Know

- Mortgage life insurance pays off some or all of your remaining mortgage balance if you pass away.

- Your premiums depend on factors such as your mortgage amount, age, and lender.

- Mortgage life insurance is not mandatory in Canada, and lenders cannot require you to purchase it as a condition for mortgage approval.

- Mortgage life insurance is often more expensive than comparable term life insurance, while providing less coverage over time as your mortgage balance declines.

- Mortgage life insurance is usually tied to your lender and is not portable. If you switch lenders, you will typically need to reapply for coverage, often at a higher cost.

- Mortgage life insurance is often underwritten at the time of a claim rather than at application, which can create a risk of denied claims if information was incomplete or inaccurate.

Protect Your Mortgage. Protect Your Family.

Your mortgage may be one of your biggest financial commitments.

Sun Life can help you explore life insurance options designed to help protect it.

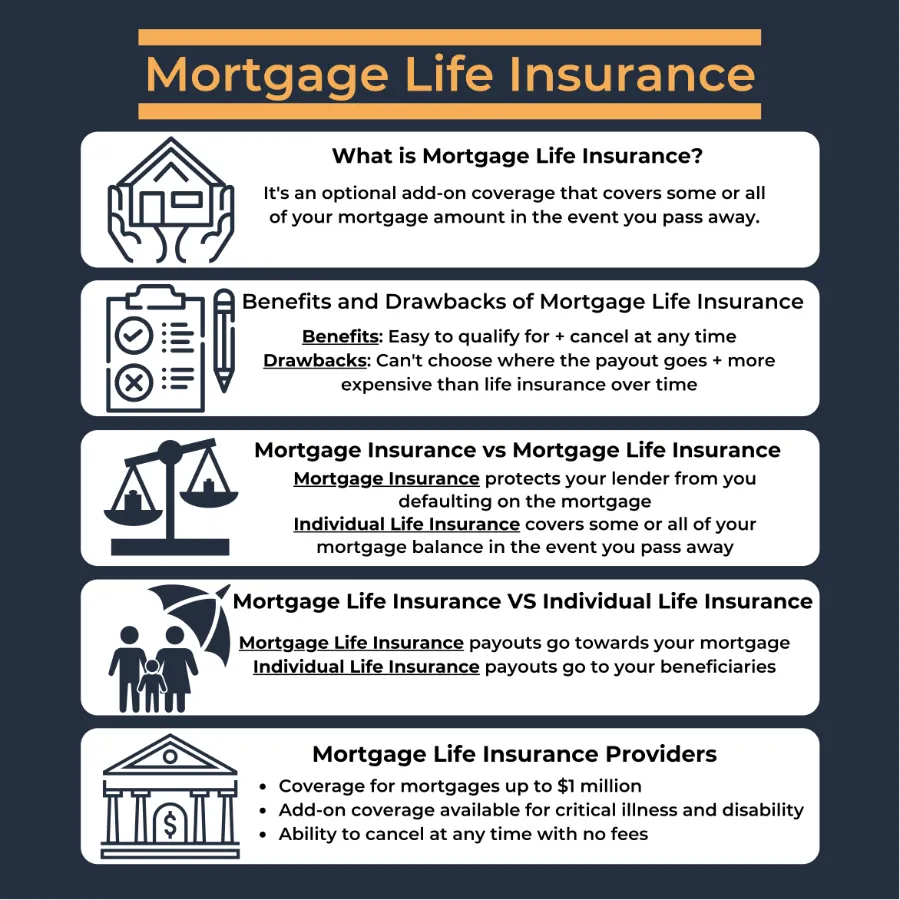

What is Mortgage Life Insurance?

Mortgage life insurance shouldn’t be confused with home insurance in Canada. Mortgage life insurance is an insurance policy that will cover all or part of your mortgage amount in the event of your passing away. Mortgages are loans secured by your home, meaning the bank can take your property if you stop making payments. Especially if you are a first time home buyer with a large mortgage, mortgage life insurance may provide you the peace of mind you need to sleep better at night, knowing that your family will be able to stay in your home in the event of a tragedy.

Coverage is offered either directly through your mortgage lender or an affiliated life insurance company when you purchase a home and get a mortgage. You will usually get your first 30 days of coverage risk-free, meaning during this period you can cancel your policy and receive your money back. Some financial institutions even offer home buyers the ability to put more than 1 person on their mortgage life insurance policy, meaning you might be able to add a co-borrower, mortgage guarantor, or mortgage endorser to your policy.

Monthly premiums are directly influenced by how much you choose to be covered for. For example, if you have a mortgage of $300,000, your monthly premium to insure the full $300,000 mortgage will likely be twice the cost of insuring your mortgage for only $150,000.

Protect Your Mortgage. Protect Your Family.

Your mortgage may be one of your biggest financial commitments.

Sun Life can help you explore life insurance options designed to help protect it.

Benefits and Drawbacks of Mortgage Life Insurance

| ✔ Pros | ✖ Cons |

|---|---|

|

|

|

|

|

|

Depending on your situation, mortgage life insurance may be something that fits your needs or may be an extra cost not worth the price. Mortgage life insurance is much easier to qualify for than individual life insurance, and usually your mortgage lender will ask a few questions before you qualify. This makes it much easier for people with poor health to get some form of life insurance coverage, which can be important to help give you peace of mind especially when getting a large mortgage amount.

A common question many home buyers have is: “Can I cancel my mortgage life insurance at any time?”. The answer is yes! One of the most appealing parts of mortgage life insurance is how you can cancel anytime and how most mortgage lenders will offer your money back after your first 30 days if you do cancel. This is so that you will be covered right away after getting a mortgage and will still have time to think over your mortgage life insurance policy. The other benefit of mortgage life insurance is the simplicity it offers. Instead of having to pay another monthly bill, mortgage lenders will add the cost directly to your monthly mortgage payment, making it an easier and simpler way to buy life insurance.

Generally, premiums can range between 10 cents to $1.65 for every $1000 in coverage you get depending on your age. Mortgage life insurance is often significantly more expensive than comparable term life insurance, while providing less coverage over time because the payout declines as your mortgage is paid down.

| Age | Average Big 5 Rate |

|---|---|

| 18 to 30 | $0.10 |

| 31 to 35 | $0.15 |

| 36 to 40 | $0.22 |

| 41 to 45 | $0.31 |

| 46 to 50 | $0.44 |

| 51 to 55 | $0.57 |

| 56 to 60 | $0.75 |

| 61 to 65 | $1.04 |

| 66 to 69 | $1.47 |

For example: you have just purchased an $800,000 house with a 20% ($160,000) down payment. Your mortgage amount is $640,000. You pay monthly mortgage life insurance premiums to cover your entire $640,000 mortgage in the event of a tragedy. 10 years later your amount owing is $440,000 as you have paid off some of your principal mortgage balance. You are now continuing to pay the same rate for mortgage life insurance, but the amount of coverage has dropped from being $640,000 initially, to now being only $440,000 as your mortgage amount has also dropped.

The biggest drawback of mortgage life insurance is post-claim underwriting. Unlike traditional life insurance, mortgage life insurance is often underwritten after a claim is made. This means your application may not be fully reviewed until a claim occurs, which can lead to denied claims if information is incomplete or inaccurate.

Another drawback is the lack of flexibility in deciding where the money goes when your policy pays out. The money will automatically go towards your mortgage amount, leaving your beneficiaries without the option to decide where to spend the money. This may be very important, especially if there are other expenses such as tuition, credit card bills, living expenses, or funeral costs to cover.

Mortgage Default Insurance vs Life Insurance

Mortgage loan insurance and mortgage life insurance differ in what they cover, when it's required, when its paid, and who offers it:

| Mortgage Loan Insurance | Mortgage Life Insurance | |

|---|---|---|

| What is it for? | Protects your lender from you defaulting | Protects your family if you pass away by covering your mortgage |

| Is it Mandatory? | Yes, for mortgages with a down payment of less than 20% | No |

| When are Premiums Paid? | Lump-sum or added to your mortgage payments. | Weekly, semi-monthly, or monthly, or added to your mortgage payments |

| Who Offers It? | CMHC or other private mortgage insurers | Your mortgage lender or affiliated life insurance company |

How is Mortgage Life Insurance Different from Individual Life Insurance?

The biggest difference between mortgage life insurance and individual life insurance is flexibility. An Individual life insurance policy will provide your loved ones with a lump sum payout that they can choose how they spend, while mortgage life insurance payouts will automatically go towards the home's mortgage amount.

The other main difference is the policy length and coverage. Mortgage life insurance only will cover you for the time that you have your mortgage, meaning that once you pay off your mortgage, you won't receive any form of coverage in the event of death. This differs from term-life insurance and whole-life insurance, where you will be covered for as long as you have your policy.

Mortgage life insurance is usually tied to your lender and is not portable. If you switch lenders or refinance with a new provider, you will typically need to reapply for coverage, often at a higher cost due to your increased age.

Unlike term life insurance, which is fully approved upfront, mortgage life insurance is often only fully reviewed at claim time—creating a risk that claims could be denied.

| Mortgage Life Insurance | Individual Term-Life Insurance | |

|---|---|---|

| How is it Paid Out? | Directly to your lender to cover your mortgage. | Directly to your beneficiaries to use how they see fit. |

| Policy Length | For the length of your mortgage or until you cancel your policy. | 5 to 40 years, depending on your term length and age. |

| Where Can You Purchase? | Through your mortgage lender or an affiliated life insurance company. | Through any life insurance company or insurance broker. |

| When Underwriting Occurs | Often at claim time (post-claim underwriting) | Before approval (upfront underwriting) |

Is Term Life Insurance Cheaper Than Mortgage Life Insurance?

Term life insurance and even whole life insurance is usually cheaper than mortgage life insurance over time. For example, according to PolicyMe, an average 40-year-old looking to purchase $500,000 in coverage for 10 years would have a monthly life insurance rate of $26.44. In comparison, TD Mortgage Protection costs $0.24 per $1,000 of coverage for someone aged 40, where $500,000 in coverage would cost $120 per month. That means that in this example, mortgage life insurance for the same coverage would cost over four times that of a term life insurance plan!

Since you’ll be paying down your mortgage over time, your coverage with a mortgage life insurance plan will also decrease over time. On the other hand, term life insurance has a set coverage amount.

Some lenders also offer bundled mortgage insurance products that combine mortgage life insurance with disability insurance or critical illness insurance. These products are designed to cover your mortgage payments if you become disabled or seriously ill, in addition to paying off your mortgage in the event of death.

Like mortgage life insurance, these bundled products are typically tied to your lender and also use post-claim underwriting, which can limit flexibility and may affect claim outcomes.

Key takeaway:

Mortgage life insurance may seem convenient, but it often costs more than general life insurance, provides decreasing coverage, and may only be fully reviewed at claim time.

Mortgage Life Insurance Providers in Canada

Mortgage life insurance providers include banks and insurance companies. Your lender might offer their own mortgage life insurance, however, you can always purchase insurance from a third-party provider.

Mortgage life insurance providers have different policies. Be sure to read them carefully and compare things such as the maximum coverage you can apply for, the add-on types of coverage offered, conditions, and your monthly premiums.

Mortgage life insurance at Royal Bank of Canada (RBC) covers up to $750,000 in mortgage amounts for borrowers. Monthly premiums will be locked-in based on how much coverage you want and your age when you apply. RBC offers you the ability to get a quote through their website in minutes for how much it will cost you to get mortgage loan insurance. RBC also offers the ability to add-on additional coverages, which include critical illness insurance and disability insurance.

Mortgage life insurance at TD offers coverage for up to $1,000,000 on your mortgage amount. Monthly premiums range from 10 cents per month per $1000 in coverage for people aged 18-30, while progressively rising based on your age, all the way up to $1.66 per month for every $1000 in coverage for those aged 66 to 69. Your monthly insurance premiums are locked-in for the full term of your mortgage, but you can still cancel coverage anytime. TD also offers add-on coverage for critical illnesses, which can cover you for up to $1,000,000.

CIBC offers up to $750,000 in mortgage life insurance coverage to reduce or pay off in full your mortgage principal. Monthly premiums per $1000 in coverage are between 8 cents, and all the way up to $1.62 depending on your age and number of borrowers being covered. Monthly premiums at CIBC will be added directly to your mortgage payments, and will be adjusted if you change how frequently you pay your mortgage.

Scotiabank offers up to $1,000,000 in coverage on your mortgage. Monthly premiums start at 14 cents per month for every $1000 in coverage for people aged 18-30 and progressively rise depending on your age, all the way up to $1.57 per month for every $1000 in coverage for people aged 66-69. Scotiabank also allows you to add other types of mortgage life insurance coverages to your policy, such as critical illness and disability insurance.

BMO offers up to $750,000 in mortgage life insurance coverage, and you can choose to cover between 50% and 100% of your mortgage balance up to this amount. You can get a quote on the BMO website for how much it will cost you in minutes. BMO allows either the main borrower on the mortgage or a co-borrower to get mortgage life insurance coverage.

National Bank offers up to $1,000,000 in mortgage life insurance coverage for people aged 18 to 64. This coverage is offered for borrowers, co-borrowers, mortgage guarantors, and mortgage endorsers.

Manulife offers up to $1 million coverage per borrower or guarantor for their mortgage life insurance plan. There's no waiting period, and you can make weekly, semi-monthly, or monthly premium payments. Manulife also offers mortgage disability insurance, and you can top-up your existing mortgage life insurance coverage. To purchase, you’ll need to go through your lender or mortgage broker.

Sun Life sells their mortgage life insurance policy as “mortgage protection insurance” for borrowers. It has a set term length, but you won't lose coverage if you switch mortgage lenders during your insurance term.

Laurentian Bank's mortgage life insurance is insured by iA Financial Group. You're covered for a balance of up to $750,000, but you'll need to complete a health questionnaire if your coverage amount is for $200,000 or more. If you purchase Laurentian Bank's mortgage life insurance, you'll also receive their Mortgage and Line of Credit Insurance Assistance Program for free. This provides financial coaching as well as legal advice and psychological support.

Mortgage Life Insurance - Maximum Coverage

| Lender | Insurer | Maximum Coverage |

|---|---|---|

| TD | Canada Life Assurance Company | $1,000,000 |

| Scotiabank | Canada Life Assurance Company | $1,000,000 |

| RBC | Canada Life Assurance Company | $750,000 |

| CIBC | Canada Life Assurance Company | $750,000 |

| BMO | Sun Life Assurance Company of Canada | $750,000 |

| MCAP | Sun Life Assurance Company of Canada | $750,000 |

| First National | The Manufacturers Life Insurance Company (Manulife) | $1,000,000 |

| National Bank | National Bank Life Insurance Company | $1,000,000 |

For mortgage life insurance policies, you need to be under an age limit to be eligible to apply. This limit is often between 65 and 70 years. Your mortgage life insurance will be active until you refinance or sell your home, at which point your insurance coverage will end. If you're over the age limit and your insurance coverage ends, you may be eligible to re-apply if your new mortgage has a similar balance under recognition of prior coverage (ROPC).

Your mortgage life insurance premium will depend on your age and mortgage balance at the time of application. Your monthly premium rate is calculated as a premium rate for every $1,000 of mortgage balance that you want to insure. If applicable, you will also have to pay provincial sales tax on your monthly insurance premiums.

Generally, you must pay mortgage life insurance premiums for each borrower on the mortgage you want to insure. Some banks offer lower joint-borrower premiums or offer a multi-insured discount. For example, TD offers a 25% premium discount if there is more than one borrower who gets insurance for the same mortgage. However, you’ll need to pay for two individual premiums.

Some lenders also offer a discount for larger mortgage balances. TD provides a 25% discount for insured mortgage balances between $300,000 and $500,000 and a 35% discount for insured mortgage balances between $500,000 and $1,000,000.

Your cost of mortgage life insurance is based on the insured mortgage balance. For example, if your premium rate is $0.32 per $1,000 of mortgage balance, and your mortgage balance is $500,000, then your cost of mortgage life insurance will be $160 per month.

Monthly Mortgage life insurance premium rates per $1,000 of single coverage

| Age | TD | CIBC | Scotiabank | RBC | BMO |

|---|---|---|---|---|---|

| 18 to 30 | $0.10 | $0.08† | $0.14 | $0.09 | $0.10 |

| 31 to 35 | $0.14 | $0.14† | $0.18 | $0.13** | $0.14* |

| 36 to 40 | $0.21 | $0.21 | $0.25 | $0.20** | $0.21* |

| 41 to 45 | $0.30 | $0.31 | $0.36 | $0.29 | $0.30* |

| 46 to 50 | $0.44 | $0.46 | $0.47 | $0.40 | $0.43 |

| 51 to 55 | $0.54 | $0.59 | $0.58 | $0.52 | $0.60 |

| 56 to 60 | $0.77 | $0.76 | $0.77 | $0.70 | $0.77 |

| 61 to 65 | $1.04 | $1.03† | $1.12 | $0.95** | $1.08 |

| 66 to 69 | $1.64 | $1.03† | $1.57 | $1.63 | - |

Premiums last updated in March 2026

*BMO has different age brackets of 18-29, 30-35 and 61-64

**RBC has different age brackets of 31-36, 37-41, and 42-45

†CIBC has different age brackets of 18-29, 30-35, 61-64 and 65-69

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.