What are Open and Closed Mortgages?

What You Should Know

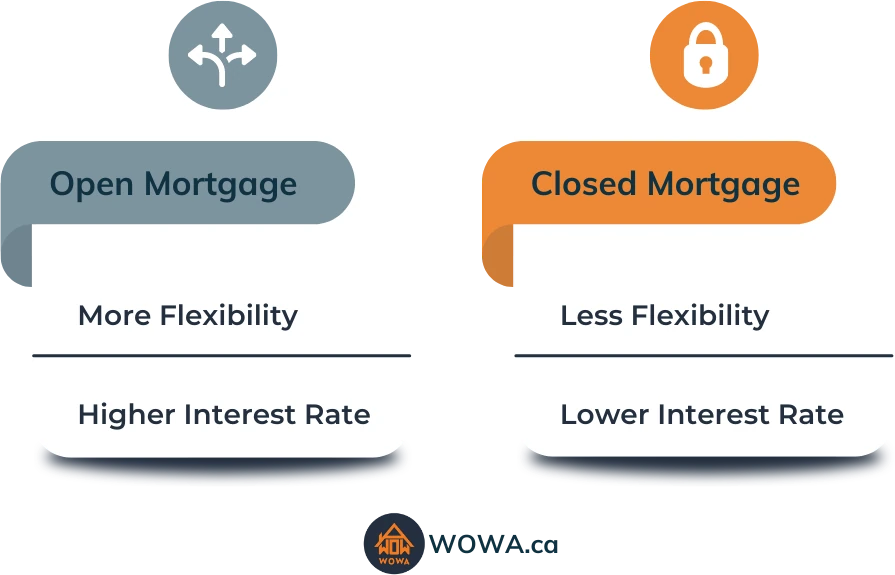

- Open mortgages provide you with more flexibility to prepay your mortgage. A closed mortgage limits your prepayments and will penalize you.

- In exchange for the prepayment flexibility, open mortgages have a higher interest rate than closed mortgages.

- A closed mortgage will penalize you for refinancing, switching lenders, or selling your home before the end of your term.

- Fixed-rate closed mortgages will have higher penalties than variable-rate closed mortgages.

When you’re getting a new mortgage or it’s time for you to renew your mortgage, you’ll be able to choose the type of mortgage that you want for the next number of years of your new mortgage term. The two main types of mortgages in Canada are open and closed mortgages, but there are also convertible mortgages and hybrid mortgages.

These different mortgage types all differ in how the mortgage is structured, particularly the ability or inability to make mortgage prepayments. Your selected mortgage type will also affect your mortgage interest rate.

What is a Closed Mortgage?

A closed mortgage is more restrictive than an open mortgage as it limits your ability to make mortgage prepayments during your term. On the other hand, open mortgages have no limits when it comes to prepayments. With a closed mortgage, you will still be able to make lump-sum mortgage prepayments during your term, but you will be limited in how much prepayments you can make per calendar year.

You can still prepay as much as you would like at the time of renewal at the end of your term with a closed mortgage. This means that if you’re looking to make large prepayments or to pay off your mortgage, you might have to wait if you want to avoid paying interest penalties.

Your annual prepayment limit is a percentage of your original principal balance, which would be the principal amount when you first started having the mortgage with your mortgage lender. For example, if you’ve switched lenders, your annual prepayment limit will be based on the principal amount that was present when the new lender was assigned your mortgage, not based on the original principal balance at your previous lender.

Most lenders also give other prepayment options besides lump-sum prepayments, such as increasing your monthly mortgage payments. Increasing your mortgage payments would allow more money to be used to pay down your principal balance. That pays off your mortgage faster and also saves you money from lower mortgage interest charges.

How Much Can You Increase Your Regular Mortgage Payments?

| Bank | Increase Limit |

RBC | Up to 100% |

TD | Up to 100% |

Scotiabank | Up to 100% |

CIBC | Up to 100% |

BMO | Up to 20% |

Canada’s major banks all allow you to make mortgage prepayments under a certain limit without any mortgage penalties. This can be as low as 10% per calendar year at RBC or as high as 20% with BMO. You can make multiple prepayments as long as the combined amount per calendar year stays under your lender’s prepayment allowance.

If you exceed your prepayment limit, you will be charged a prepayment penalty. If you refinance your mortgage, switch lenders, or renegotiate your interest rate before your mortgage term is over, you’ll also be charged mortgage penalties. Mortgage penalties can be significant, particularly for closed fixed-rate mortgages.

Closed Mortgage Prepayment Limits at Canada’s Major Banks

| Bank | Prepayment Limit (% of principal per year) |

|---|---|

| RBC | 10% |

| TD | 15% |

| Scotiabank | 15% |

| CIBC | 10% - 20% |

| BMO | 20% |

| National Bank | 10% |

What is an Open Mortgage?

An open mortgage is open to mortgage prepayments of any amount and at any time. If you have extra money saved up, you can use that money to make a prepayment. Prepayments are a one-time lump-sum that is applied towards your mortgage principal, while your regular mortgage payments have to cover both your interest and principal. As mortgage prepayments are fully used to pay down your principal balance, you'll be saving interest while paying off your mortgage faster.

Open mortgages allow you to make mortgage prepayments without any prepayment penalties. You can make extra prepayments every month, or you can pay off your entire mortgage all at once without any extra charges.

Being completely open means that you can freely refinance your mortgage or renegotiate your mortgage at any time, and it will cost less since there won’t be any prepayment penalties. For example, if open mortgage rates have fallen, you can renegotiate to the lower mortgage rate without any penalties.

In exchange for the flexibility that open mortgages provide, open mortgages usually have a higher interest rate when compared to closed mortgages.

Open vs Closed Mortgages

| Pros | Cons | |

|---|---|---|

| Open Mortgages |

|

|

| Closed Mortgages |

|

|

Interest Rate

To make up for the numerous limits placed on closed mortgages, such as not being able to refinance or switch lenders midway through your term without penalties, closed mortgages have lower interest rates than open mortgages.

The lower interest rate for closed mortgages is the main reason why closed mortgages are the most common option in Canada. Most mortgage rate ads that you see will also be for closed mortgages, since they are able to show more attractive rates when compared to higher open-mortgage rates.

Flexibility

Open mortgages are easily the most flexible choice. You won’t have to worry if changing lenders will cost you thousands of dollars in mortgage penalties, and you can have peace of mind in knowing that you can renegotiate your mortgage rate at any time. The ability to make mortgage prepayments without having to fuss over your lender’s prepayment limits is also a great feature for homeowners that have the potential and means to pay off their mortgage early.

Closed mortgages lock you into your lender for the term length of your mortgage, and you won’t be able to switch or renegotiate without significant penalties. If interest rates drop significantly, you won’t be able to take advantage of the lower rates without paying any penalties to your lender if you have a closed fixed-rate mortgage. Mortgage prepayment penalties can more than offset any potential interest savings. You won’t have to worry about this with an open mortgage.

What is a variable closed mortgage?

Closed variable-rate mortgages have an interest rate that follows your bank’s prime rate, which is based on market rates. On the other hand, closed fixed-rate mortgages have an interest rate that stays the same for your term length.

If interest rates fall, your mortgage rate for a variable closed mortgage will also fall, allowing you to benefit through interest savings. Variable closed mortgages are still closed mortgages, which means that the same prepayment limits as fixed closed mortgages apply.

However, variable-rate closed mortgages can have lower prepayment penalties, as their penalties are calculated based on three months’ worth of interest. Fixed closed mortgages have penalties based on the higher of three months’ worth of interest or an “interest rate differential”, which is the difference between your contract mortgage rate and current Canada mortgage rates. To find out how much penalties you will need to pay, visit our mortgage penalty calculator.

Are you likely to sell soon?

When you sell your home, you’ll be paying back the entire mortgage using the money you received from the buyer. If you sell before your mortgage is up for renewal, you’ll be charged prepayment penalties. If you’re buying another home, you could avoid penalties by porting your mortgage over to the new home.

If you expect that you’ll be selling your home within the next couple of years, an open mortgage can allow you to avoid prepayment penalties.

Convertible Mortgages

If you’re undecided between an open mortgage or a closed mortgage, many banks and lenders offer convertible mortgages. Convertible mortgages are a fixed-rate closed mortgage for a very short term, with most being 6 months.

This short term period allows you to switch lenders or make larger prepayments at renewal without any penalties, since your term renewal will be much earlier than a 5-year term. You can also choose to convert your 6-month convertible mortgage into a longer-term mortgage without penalties. You may have to pay an additional fee for the ability to convert into a longer term.

Convertible mortgages are useful if you’re looking to sell your home soon or you’re close to having enough money to fully pay off your mortgage early. They can also be used if you feel like interest rates will fall in the next 6 months, allowing you to lock-in a lower mortgage rate at the end of your 6-month term.

6-month open mortgages are also an option if you’re still undecided. However, mortgages with short terms, such as a 6-month open mortgage or a 6-month convertible mortgage, all have very high interest rates.

The choice between an open mortgage and a closed mortgage comes down to how much you value flexibility over having a lower mortgage rate. To help guide you in this decision, you can use a mortgage interest calculator to find out how much interest would cost for a closed-mortgage term. Compare the total interest that you’ll pay for a closed mortgage with the higher total interest for an open mortgage, and see if the increased cost is worth the convenience of an open mortgage.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.