Mortgage Pre-Approval in Canada

A mortgage pre-approval tells you how much a lender may be willing to lend you and locks in an interest rate for a set period while you shop for a home. It's a strong signal to sellers and real estate agents that you're a serious, ready buyer. Getting pre-approved is one of the first steps most Canadians take before house-hunting: it sets your budget and protects you from rising rates during your search.

Just remember one thing as you read on: a pre-approval is an estimate, not a guarantee. Final approval still depends on the specific home you buy and a full review of your finances.

What You Should Know

- A pre-approval is an estimate of how much you may be able to borrow, plus a rate hold that protects you from rate increases while you shop.

- Rate holds typically last 90 to 130 days, depending on the lender.

- A pre-approval is not final approval: the lender still verifies your documents and appraises the home before funding.

- You'll need proof of income, proof of down payment, ID, and consent to a credit check.

- Getting pre-approved is free, and there's no obligation to take the mortgage.

- Avoid taking on new debt, changing jobs, or making large unexplained deposits between pre-approval and closing.

What is a mortgage pre-approval?

A mortgage pre-approval is a lender's written estimate of the mortgage amount and interest rate you may qualify for, based on a review of your finances. It's more detailed than a pre-qualification because it involves a credit check and a closer look at your income, debts, and down payment.

A pre-approval usually gives you two things:

- The maximum mortgage amount you may be able to borrow.

- A rate hold: a guarantee that your quoted mortgage rate won't rise for a set period, even if market rates do.

It does not guarantee that you'll receive the full amount or the final mortgage. That decision comes later, once you've made an offer and the lender reviews the specific property and your verified documents.

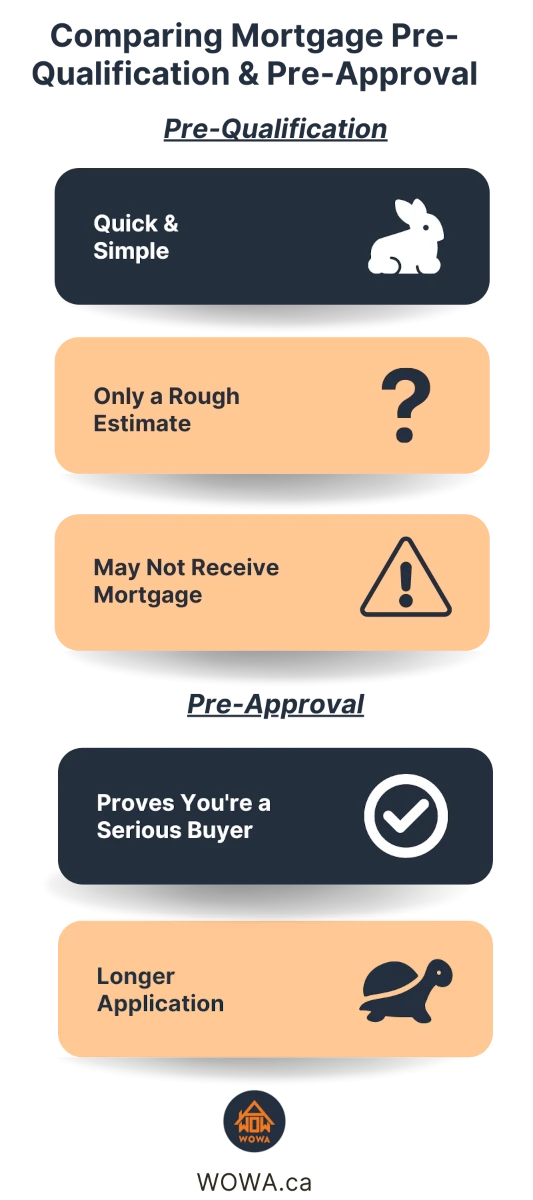

Pre-qualification vs. pre-approval

These two terms are often confused, but they're different steps:

| Pre-qualification | Pre-approval | |

|---|---|---|

| How long it takes | Minutes | A bit longer, involves a full application |

| Detail | A rough estimate based on numbers you provide | A closer review of your finances |

| Credit check | Often a soft check (no score impact) | Typically a hard check (may affect your score) |

| Rate hold | None | Yes, commonly 90 to 130 days |

| What it proves to sellers | Little | That you're a serious, ready buyer |

In short: pre-qualification is a quick check early in your journey, while a pre-approval carries weight when you're ready to buy.

Important: a pre-approval is not final approval

A pre-approval is a helpful estimate and a rate hold; it is not a commitment to lend. Final approval still depends on:

- Verifying your income, down payment, and documents.

- A home appraisal of the specific home confirming it's worth what you're paying.

- No major change to your finances, employment, or credit between now and closing.

Treat your pre-approved amount as a ceiling to shop under, not a promise.

Benefits of getting pre-approved

Getting pre-approved is optional, but it offers real advantages:

- Know your budget. You'll know how much you can spend and avoid homes outside your range.

- Lock in your rate. A rate hold protects you if rates climb while you search. If rates drop, many lenders will let you take the lower rate.

- Shop with confidence. Sellers and agents take pre-approved buyers more seriously, which can strengthen your offer.

- Plan your finances. You'll have a clearer picture of your monthly mortgage payment and down payment needs.

- It's free. Pre-approvals cost nothing, and you're not obligated to proceed.

How long does a mortgage pre-approval last?

Most lenders hold your rate for 90 to 130 days. If you don't buy a home within that window, the rate hold expires, but you can usually reapply for a new one, which may involve an updated credit check.

Among Canada's Big Five banks, rate holds currently run up to 120 days, with BMO offering up to 130 days. If interest rates fall during your hold, most lenders let you request the lower rate (which may restart the clock).

Tip: Apply for your pre-approval when you're seriously ready to shop, roughly 90 to 120 days out. Applying too early can mean the hold expires before you find a home.

Documents you need for a mortgage pre-approval

Required mortgage documents vary by lender, but most ask for some combination of the following. Having these ready speeds things up and makes your pre-approval more reliable, since it's based on verified information rather than estimates.

- Government-issued photo ID: driver's licence or passport.

- Proof of income: recent pay stubs and/or an employment letter. If you're self-employed, your last two years' Notices of Assessment and tax returns (T1).

- Proof of down payment: recent bank or investment statements (often 90 days of history). If any funds are a gift, a signed gift letter.

- Assets: bank accounts, investments, and any other property you own.

- Debts and liabilities: credit cards, car loans, lines of credit, student loans, and other obligations.

- Employment history: current employer details, plus previous employer if you've been at your current job under two to three years.

- Consent to a credit check: some banks' online tools use a soft check first and pull a hard inquiry later, at full application.

How to get a mortgage pre-approval?

You can get pre-approved through a mortgage broker or directly from most lenders. The process is similar to applying for a mortgage:

- Gather your documents (see the checklist above).

- Compare lenders and rates. Because your rate affects how much you can afford, it pays to shop around. A broker can compare many lenders at once.

- Complete the application with your income, down payment, assets, and debts.

- Consent to a credit check. Online tools at several banks use a soft check at this stage.

- Receive your pre-approval, a letter or certificate stating your maximum amount and your held rate.

What lenders look at when you apply

A pre-approval isn't just a yes-or-no, the lender also estimates how much you can borrow and at what rate. Here's what they weigh.

Your credit score

In Canada, credit scores range from 300 to 900. There's no single national cut-off as each lender and mortgage insurer sets its own bar:

- Insured mortgage (down payment under 20%): At least one borrower generally needs a score of about 600, per CMHC and other insurer guidelines.

- Uninsured mortgage (20% or more down): Many major banks look for roughly 680 or higher for their best rates, though minimums vary by lender.

- Alternative (B) lenders: Some may consider scores in the low 500s, usually with a larger down payment and a higher rate.

A short credit history can affect your application even with a good score. To improve your score, pay bills on time, keep credit card balances low, and avoid applying for new credit right before a mortgage. There are several free services in Canada to check your score.

Your income and employment

Lenders want to see stable, verifiable income. Generally:

- Steady employment income (salary from a full-time permanent job) is weighted fully.

- Variable income: bonuses, commission, self-employment, or investment income is often averaged, discounted, or requires a two-year track record.

How each type is treated varies by lender, so it's worth asking how your specific income will be assessed.

Your debt service ratios

Lenders check two debt service ratios to make sure your debt load is manageable, both measured at the stress-test rate:

- Gross Debt Service (GDS): housing costs (mortgage, property tax, heat, and 50% of condo fees) as a share of gross income. For insured mortgages, the limit is up to 39%.

- Total Debt Service (TDS): GDS plus all other debt payments. For insured mortgages, the limit is up to 44%.

Banks often apply tighter internal caps on uninsured mortgages. You can estimate your own numbers with our Mortgage Affordability Calculator.

Your down payment

Your down payment size shapes what you qualify for and whether you need mortgage default insurance. Current insured-mortgage rules in Canada:

- Minimum down payment: 5% on the first $500,000 of the price, plus 10% on the portion between $500,000 and $1.5 million.

- Insured price cap: $1.5 million (raised from $1 million on December 15, 2024). Homes priced at or above $1.5M require at least 20% down and can't be insured.

- 30-year amortization: available on insured mortgages for first-time buyers and buyers of newly built homes; otherwise the insured maximum is 25 years.

A down payment under 20% requires mortgage default insurance (from CMHC, Sagen, or Canada Guaranty). Your down payment must come from acceptable sources, such as your own savings, an RRSP or FHSA withdrawal, or a non-repayable gift with a signed gift letter.

The mortgage stress test

Federally regulated lenders must confirm you could still afford your payments if rates rose. To pass the stress test, you must qualify at the higher of your contract rate + 2% or a 5.25% floor.

The stress test applies to new mortgages and refinances. However, it generally does not apply when renewing with your existing lender. It may also not apply when switching lenders at renewal through a straight switch, which means the loan amount and amortization do not increase.

One recent change: as of November 21, 2024, borrowers with uninsured mortgages can switch lenders at renewal without re-qualifying under the stress test, provided the loan amount and amortization stay the same. Try our Stress Test Calculator to see how you'd fare.

Big 5 bank mortgage pre-approvals compared

All five major banks offer a rate hold with pre-approval.

| Bank | Application Process | Rate Hold |

|---|---|---|

RBC | Online application | Up to 120 days |

Scotiabank | Online application | Up to 120 days |

TD | Online, through phone, or in-person meeting | Up to 120 days |

CIBC | In-person meeting | Up to 120 days |

BMO | Online, through phone, or in-person meeting | Up to 130 days |

RBC Royal Bank Mortgage Pre-Approval

RBC offers both pre-qualification and pre-approval. If you apply online, RBC uses a soft credit check first and pulls your full credit report later, at the mortgage application stage. A pre-approval comes with a rate guarantee of up to 120 days.

Scotiabank Mortgage Pre-Approval

Scotiabank's eHOME platform lets you get pre-approved for a Scotiabank mortgage, search for a home, and apply for your mortgage entirely online, with a rate hold of up to 120 days. You can also work with a Scotiabank advisor if you prefer.

TD Bank Mortgage Pre-Approval

You can apply for a TD mortgage pre-approval online, by phone, or in person, with a rate hold of up to 120 days. Applying online has no impact on your credit score, and if rates drop during your hold, you can ask to have your rate adjusted.

CIBC Mortgage Pre-Approval

CIBC provides a pre-approval certificate with a rate guarantee of up to 120 days. You can start online or by phone, and a CIBC mortgage advisor typically follows up to complete the process.

BMO Bank of Montreal Mortgage Pre-Approval

BMO offers a rate hold of up to 130 days, the longest among the Big Five, and you can apply online, by phone, or in person. Its digital pre-approval can return a decision quickly.

What not to do after getting pre-approved

Your lender re-checks your finances before final approval. Until your mortgage closes, avoid anything that changes the picture they pre-approved:

- Don't take on new debt. A new car loan, financing furniture, or a new credit card can raise your debt ratios and shrink what you qualify for.

- Don't make large or unexplained deposits. Lenders need to trace your down payment; undocumented lump sums can hold up approval.

- Don't change jobs or income sources if you can help it. A new job, probation, or a switch to self-employment can affect how your income is assessed.

- Don't miss payments. A single late payment can lower your credit score and put your rate or approval at risk.

- Don't apply for other credit. Extra hard inquiries and new accounts can lower your score at the worst time.

- Don't spend your down payment or closing-cost savings. Keep those funds intact and where the lender expects them.

If a major financial change is unavoidable, tell your mortgage professional first so it can be planned around.

Should you keep a financing condition?

When you make an offer on a home, a financing condition (or "financing clause") gives you a set number of days to secure your mortgage after your offer is accepted. It lets you walk away and recover your deposit if financing falls through. In competitive markets, some buyers waive it to make an offer more attractive.

Be cautious here. Because a pre-approval is not final approval, waiving the financing condition carries real risk. Final approval still depends on the home appraising at or above your purchase price, income and document verification, and your finances staying stable. If financing then falls through, you can lose your deposit, and you may be liable for the seller's losses if they resell for less.

A pre-approval can strengthen your position, but the decision to keep or waive a financing condition should be made with your mortgage professional and real estate lawyer, based on your situation, not automatically because you hold a pre-approval.

Can you be denied a mortgage after pre-approval?

Yes. A pre-approval doesn't guarantee final approval. Common reasons a mortgage falls through after pre-approval include:

- Your finances changed: new debt, a drop in income, or a job change.

- The appraisal came in low: the home is worth less than your offer price.

- Missing or unsatisfactory documents during verification.

- A credit issue: a missed payment or new hard inquiries, lowering your score.

If you're denied, options may include a larger down payment, a co-signer, or exploring alternative lenders with more flexible requirements.

What a mortgage pre-approval letter looks like

Once pre-approved, you'll receive a pre-approval letter or certificate. You can share it with sellers as proof that you can afford the purchase. It typically includes:

- Your pre-approved mortgage amount: the maximum the lender may lend you.

- Home price: the maximum price you can support based on your down payment.

- Mortgage interest rate: the rate held for you, guaranteed for the rate-hold period if you're approved within it.

- Expiry date: when the rate hold ends (commonly 90 to 130 days out).

- Mortgage type and terms: such as amortization, term, and loan-to-value (LTV) ratio.

Sample pre-approval terms (illustrative only):

Based on the information provided, you may be pre-approved for a mortgage with the following terms:

- Sale price: $1,000,000

- Loan amount: up to $800,000

- Interest rate: your held rate

- Amortization: 25 years

- Mortgage term: 5 years

- LTV: 80%

- Rate hold: 120 days from issue

This is an example of what a pre-approval letter might contain. Actual figures depend on your finances and lender.

Frequently asked questions

Does the interest rate depend on the length of the pre-approval?

The length of your rate hold is one factor, but it's not the main one. A longer hold can carry a slightly higher rate because the lender is guaranteeing it for longer. Your credit score, complete documentation, and overall financial situation matter more. In general, the lower-risk you appear, the better your rate.

What should I do after getting pre-approved?

Review your conditions and note when your rate hold expires. Keep your finances stable, and once you find a home, apply for the full mortgage and provide the documents your lender requests. If your situation has changed since pre-approval, your rate or terms may change.

Should I negotiate the final mortgage rate?

Yes, you can often negotiate. A strong application (good credit, a larger down payment, low debt) gives you more leverage. Mortgage brokers may also buy down the rate from their lenders. It's worth shopping around, and remember that rate isn't everything. Other terms matter too.

Do I need a pre-approval for a pre-construction condo?

Often, yes. Builders commonly require a mortgage pre-approval as a condition of purchase, and may ask for one at any time. Keep in mind that for a condo completing years away, the rate in your pre-approval may differ from your actual rate at closing.

Do mortgage pre-approvals affect your credit score?

It depends on the check used. Online pre-qualifications and several banks' online pre-approval tools use a soft check with no impact. A full pre-approval usually involves one hard inquiry, which can lower your score slightly. If you're shopping with multiple lenders, inquiries made within about 45 days are typically treated as a single inquiry.

Do mortgage pre-approvals cost money?

No. Pre-approvals are free, and you're not obligated to take the mortgage.

Do I need to pass the stress test for a pre-approval?

If your lender is federally regulated (like a bank), yes, you'll need to pass the stress test to be pre-approved. You can use a stress test calculator as a rough guide. Other lenders, such as some credit unions, may not be required to use the federal stress test, but they may still apply their own qualification rules to assess your income, debts, credit, and ability to make payments.

Should I tell my real estate agent how much I'm pre-approved for?

You can share your maximum comfortable price range so your agent can tailor the search, but you don't have to disclose your income or how much you have saved. And remember: being pre-approved for a large amount doesn't mean you should spend it all.

Can I offer more than my pre-approval amount?

You can, but you'll need a way to finance the difference, often a larger down payment. If the gap is small, you might qualify for a larger mortgage when you apply. If it's large, you may need to increase your down payment.

Do mortgage pre-approvals expire?

Yes. Because a pre-approval is based on your finances at a point in time, the rate hold expires after the set period (commonly 90 to 130 days). If it expires before you buy, you can apply for a new one.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.