Required Mortgage Documents in Canada

What you Should Know

- There are five categories of documents you need when applying for a mortgage in Canada.

- First, you will need to prove your identification.

- Second, you will need to verify your source of income.

- Third, you will need to provide basic financial information such as your credit score, net worth, and banking statements.

- Fourth, you must demonstrate your down payment source. It could be your savings, the sale of your prior home, RRSP account, or a gift.

- Finally, you must provide details of the property you are buying.

The Ultimate Mortgage Application Checklist: Documents Required in Canada (2026)

Buying a new property or refinancing your mortgage in Canada can involve extensive documentation. Sorting your mortgage before hiring a real estate agent will ensure that you don’t waste each other's time. To get a mortgage, you will typically need five types of documents:

- Identification - Government-Issued ID etc.

- Proof of income - Pay Stubs, Tax Forms, etc.

- Basic financial information - Bank Statements, Proof of Investments, etc.

- Down payment confirmation - Sale Agreement of Existing Property, Documents Related to Savings and Investments, etc.

- Property details - Purchase and Sale Agreement, MLS Listing, etc.

If someone cosigns your mortgage, they must also provide their identification and financial information. This article will simplify the process by helping you understand the documents that can be included in each category. You can also use the document checklist at the end of this article to help you in the process.

Personal Identification Documents for Mortgage Applicants

Before you can begin applying for a mortgage, your lender would want to verify your identity. Quite simply, you'll need to show:

- A government-issued ID (with current address)

- Your SIN number

Income Verification: Documents Needed to Prove Your Earnings

This category of documents provides proof of your monthly income and ability to meet debt servicing ratios to the mortgage lenders. In particular, lenders will calculate your monthly mortgage payments to ensure your monthly housing costs don't exceed 39% of your gross monthly income. Additionally, your income has a direct effect on your maximum mortgage affordability.

Recent pay stubs

Your recent pay stubs serve as immediate proof of your current earnings and year-to-date (YTD) income. Many Canadian lenders ask for your two or three most recent, consecutive pay stubs to verify that your income is stable and active.

T1 General Tax Forms: 2-Year Income History

This form provides a comprehensive breakdown of your income for the tax year. To verify income consistency, many lenders ask for your T1 General forms for the two most recent tax years, especially for self-employed applicants or borrowers with variable income.

Notice of assessment (NOA)

A Notice of Assessment (NOA) is the official document issued by the Canada Revenue Agency (CRA) after your tax return has been processed. Lenders review your NOAs from the two most recent tax years to verify your 'Line 15000' (Total Income) and to ensure you have no outstanding income tax debt, which is a common requirement for final mortgage approval.

T4 or T4A tax forms

Your T4 slip summarizes the employment income and deductions for the year as an employee. The T4A slip covers "other income," including pensions, commissions, or self-employed commissions.

Note for the Self-Employed: While some independent contractors receive a T4A for specific services, most self-employed individuals do not receive a standard tax slip for their primary earnings. Instead, they report income through their T1 General and Form T2125 (Statement of Business or Professional Activities). If you are an employee, you will receive these slips from your employer annually; if you are retired or a contractor, they are issued by the relevant payer or financial institution.

Mortgage Employment Letter: Requirements and Sample Info

This letter provides lenders with a sense of your job stability. Make sure the letter includes:

- How long you have worked for the current company

- Employment status (permanent, temporary, or probationary employee)

- Whether you are full-time, part-time, or seasonal

- Hourly or annual salary rate

- Guaranteed hours (for part-time or hourly employees)

- Current role and title

Additionally, make sure the letter is on a company letterhead, signed by HR or a manager, and no older than 30 days. You can learn more on our guide to getting a letter of employment for a mortgage.

Documents for Self-Employed Applicants & Rental Income

- Self-employed: Business owners and contract workers are considered riskier to lenders. This is because they have less income stability than full-time employees. To make up for this, self-employed individuals applying for a mortgage will need to submit income documents for a more extended period - usually from the past three years. Additionally, they may be required to show articles of incorporation or a business license.

- Rental properties: Canada's real estate investors may be eligible to include rental income in their mortgage applications. For example, this allows those using the BRRRR method to use their rental income to qualify for a mortgage. However, if pursuing this route, make sure to have rent or lease agreements handy.

Financial Records: Credit, Assets, and Debt Documentation

This category is designed to provide lenders with a snapshot of your overall financial situation. In particular, they will want to know your credit score and credit history.

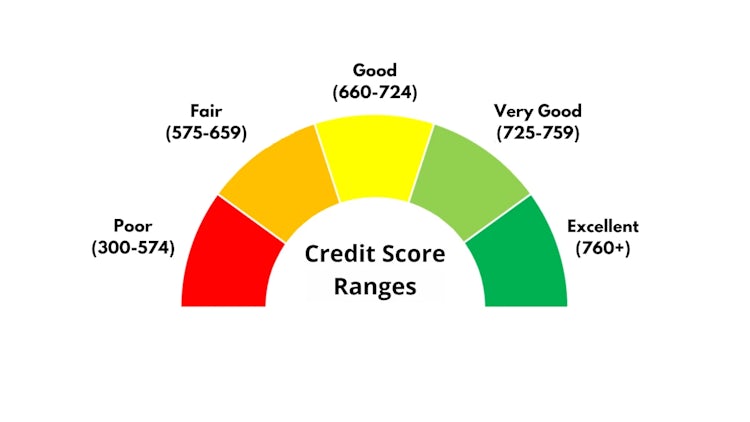

Credit score

Your credit score is a three-digit number that lenders use to measure your creditworthiness. In Canada, while 680 is often preferred for the best rates at ‘A’ lenders, the actual minimum credit score for an insured mortgage is currently 600 for at least one borrower. There are many ways to check your credit score for free.

Mortgage pre-approval letter

A mortgage pre-approval letter demonstrates that you have enough income and credit to meet the lending criteria.

Bank statements

Your bank statements provide a snapshot of your liquid assets and help lenders verify your monthly cash flow and existing debt obligations. Many lenders ask for the most recent 90 days of bank statements to verify the source of funds and recent account activity. They primarily look for consistent balances and a lack of non-sufficient funds (NSF) alerts. Lenders review your bank statements to confirm you have the funds for closing costs and to check for undisclosed liabilities. Ensure these are official PDF downloads from your online banking that clearly show your name, account number, and the bank’s logo.

List of assets and investments

Your list of assets will show the value of your investments and property. This may include cars, boats, real estate, RRSPs, and stocks. Lenders will use this to calculate your net worth.

Down Payment Verification: How to Prove Your Source of Funds

This category is pretty straightforward - lenders want to make sure you have the funds to cover your down payment. There are multiple methods to prove your source of funds, whether through your investments, the sale of your previous home, or a gift. You do not need all of the documents listed below, just enough to prove you can afford the down payment. It also helps to understand if you will have an insured or uninsured mortgage.

Insured vs. uninsured mortgage

An insured mortgage has a down payment of less than 20% of the property value. An uninsured or conventional mortgage has a down payment of 20% or more of the value. You can use a loan-to-value calculator to understand the type of mortgage you will need.

Statement of savings or investments

This document proves that the funds you use for your down payment are liquid (meaning they can be easily accessed). The statement must be less than 90 days old and list the account holder, account number, type of account, and current balance. If you are selling stocks in a taxable account, keep in mind the capital gains tax you will need to pay at the end of the tax year.

Sale agreement of existing property

Existing homeowners can use the proceeds from selling their previous house as the downpayment for their next house. If you are using the sale of your last home for this, then you will need to include a copy of the offer.

However, if you can’t sell your home fast enough, then don't worry - you can use a HELOC or a bridge loan to finance your down payment. Just be aware of how these loans affect your debt servicing ratios, as mentioned in category one.

FHSA Withdrawals (First-Time Buyers)

The First Home Savings Account (FHSA) allows you to withdraw up to your total account balance (including investment growth) tax-free for a down payment. To use these funds, lenders will typically require:

- Account Statements: Showing a 90-day history of the funds to verify the source of the savings.

- Form RC725: A copy of the "Request to Make a Qualifying Withdrawal from your FHSA" form that you submit to your financial institution.

- Proof of Qualification: Confirmation that you are a first-time home buyer as defined by the CRA.

Don’t forget about closing costs

The most common mistake of homebuyers is not budgeting for closing costs. These are one-time fees that must be paid when finalizing your purchase. In general, these cost around 1.5%-4% of the final purchase price. However, you can use a closing cost calculator to get a better estimate.

RRSP Home Buyers' Plan (HBP): Withdrawal Documentation

First-time homebuyers in Canada can withdraw up to $60,000 from their RRSPs for a down payment under the RRSP Home Buyers' Plan (HBP). Qualified individuals receive the funds tax-free, provided the amount is repaid to the RRSP within 15 years, with repayments beginning in the second year after the withdrawal. To use these funds, lenders will typically require:

- Account Statements: Showing a 90-day history of the funds to verify the source of the savings.

- Form T1036: A copy of the "Home Buyers' Plan (HBP) Request to Withdraw Funds from an RRSP" form submitted to your financial institution.

- Proof of Qualification: Confirmation that you are a first-time home buyer as defined by the CRA.

Mortgage Gift Letter: Rules for Down Payment Gifts

A gift letter proves that you will receive funds for your down payment from an outside source, such as friends and family. The letter should include:

- Name of giver

- Amount gifted

- A statement that the funds are a gift and not a loan

Down payment assistance programs (DPAPs)

Given the rising housing market prices in Canada, it's tough for many to afford a down payment. This is why the federal, provincial, and municipal governments across Canada have created down payment assistance programs to help you buy a home.

There are also many incentives for first-time homebuyers, such as tax rebates.

Property-Specific Documents for Your Mortgage Approval

The final category is straightforward - lenders want to see details of the property you are buying. Additionally, if you are selling another home, they ask for information on it too.

Final purchase and sale agreement

This is the signed contract between you and the seller. Lenders want to see this because it provides details such as the date of purchase and final purchase price.

MLS Listing

The listing is helpful to mortgage lenders because it provides them with an estimation of your property taxes, utility costs, and condo fees (if buying a condominium). These are all inputs required to calculate your gross debt service ratio.

Additional ways to save time

Follow the tips below to expedite your mortgage application.

- Triple check all documents: It's not uncommon to make mistakes when completing paperwork. Carefully review everything to make sure it's filled out accurately.

- Have your mortgage lender review: You could be missing something even with multiple reviews. Have a fresh set of eyes to ensure everything is completed correctly to minimize mistakes. If you are using a mortgage broker, they may suggest changes that improve your chances of receiving a mortgage.

- Complete all paperwork: Having a mortgage application held up because you forgot to complete a section is no fun. Make sure everything is completed in full.

- Organize your files: Many files are required to receive a mortgage. Keep a folder to store your documents in.

Legal description of the home

A legal description is a complete legal description of the property that states the full address and postal code. This information can be found on your final purchase and sale agreement and on documents such as tax assessments, title certificates, etc.

Homeowners insurance policy

Most mortgage lenders in Canada will require you to have homeowners insurance. This will protect your home from repair costs due to water damage, fire, and more. You will need to provide a copy of the policy to your lender. If you are buying a condo then you will need to prove you have condo insurance. If you need home insurance, the best way is to apply for quotes online. This will give you a feel for pricing, and understand which policies you need. You can visit our page for a full list of insurance providers in Canada.

Lenders' title insurance

Finally, lenders require you to obtain title insurance in Canada. This will protect your lender if someone else has a claim on your property.

Additional property details (if selling a home)

Those selling their existing home to buy a new one will need to submit a few additional documents to their mortgage lender. In particular, you will need to submit a recent mortgage statement and a legal description of the home you are selling.

Status Certificate/Estoppel Certificate (If purchasing a Condo)

Lenders often require a current Status Certificate or Estoppel Certificate when financing a condo purchase, and they may request an updated copy if the existing one is no longer recent, to verify the financial health of the condo corporation, reserve fund adequacy, and that the specific unit's maintenance fees are not in arrears.

Maintenance Fee Verification (If purchasing a Condo)

A recent condo fee statement helps the lender confirm your monthly housing costs when calculating your debt service ratios.

The bottom line

Many documents are required if you're trying to get approved for a mortgage in Canada. Mortgage lenders want proof of your identification, income and basic financial information. They also need confirmation on the down payment source. You'll also be asked to provide property details about the house, including legal descriptions and insurance policies. If you already have a mortgage, you can save time when buying a new home by porting your existing mortgage.

Summary: Downloadable Canada Mortgage Document Checklist

Category One: Identification

Government-issued ID (with current address)

SIN number

Category Two: Proof of income

Two to three most recent pay stubs.

T1 general tax form from the last two years

Notice of assessment from the last two years

T4 tax form

Letter of employment from the previous 30 days

Additional Considerations

- Self-employed

T4A tax form

All files from above but for a more extended duration

- Real estate investor

Lease/ rental agreement from tenants

Category Three: Basic financial information

Credit score above 600

Mortgage pre-approval letter

Bank statements from the most recent three months

List of assets and investments

Separation or Divorce Agreement (to verify support obligations or asset distributions, if applicable)

Category Four: Down payment confirmation (Only need your source of funds)

Statement of savings or investments no older than 90 days

Sale agreement of existing property

RRSP withdrawals (first-time buyers)

Gift letter (gifting down payment)

FHSA Statements (90-day history) and a completed Form RC725

Proof of available funds for closing costs, which lenders often expect to be in addition to the down payment

Category Five: Property details

Final purchase and sale agreement

MLS Listing

The legal description of the home you are buying

Homeowners insurance policy

Lenders' title insurance

Status Certificate/Estoppel Certificate (If purchasing a Condo)

Maintenance Fee Verification (If purchasing a Condo)

Additional Considerations (if also selling a home)

Recent mortgage statement

The legal description of the home you are selling

Frequently Asked Questions (FAQ)

How recent must my employment letter be?

Many Canadian lenders prefer a recent letter of employment, often dated within 30 days of the application or closing, although exact requirements vary by lender. If your closing is several months away, your lender may ask for an updated letter and a fresh pay stub closer to the closing date to ensure your employment status hasn't changed.

Can I provide screenshots or CSV exports of my bank statements?

Generally, no. Lenders usually prefer official bank statements or lender-acceptable transaction records that clearly show your name, account number, institution details, and recent transaction history. Screenshots and Excel files are often rejected because they can be easily altered and lack the formal verification required for anti-money laundering (AML) audits.

Are digital signatures (like DocuSign) accepted for these documents?

Yes, most lenders and brokers in Canada now accept electronic signatures for the initial application and document submission. However, keep in mind that when you visit your lawyer to sign the final "Charge/Mortgage" and land transfer documents, a physical "wet" signature in the presence of a legal professional is still often required.

Can I use my First Home Savings Account (FHSA) for the down payment?

Absolutely. To use your FHSA funds, you must provide your lender with a 90-day account history (similar to a standard bank account) and a copy of Form RC725, which is the official request for a qualifying tax-free withdrawal.

What if I've lost my T4 or Notice of Assessment (NOA)?

You can download digital copies of your NOAs and T4 slips directly from the CRA "My Account" portal. These digital copies are commonly accepted by Canadian mortgage lenders. If you haven't registered for an account, you can also call the CRA at 1-800-959-8281 to request paper copies by mail.

Do I need to provide documents for my co-signer?

Yes. If you are using a co-signer to qualify, they are legally considered a co-borrower. They must provide the same full set of documentation as you, including identification, income verification, and a list of their own assets and liabilities.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.