Condo Insurance in Canada

What You Should Know

- Proof of home insurance is one of the required documents to receive a mortgage in Canada.

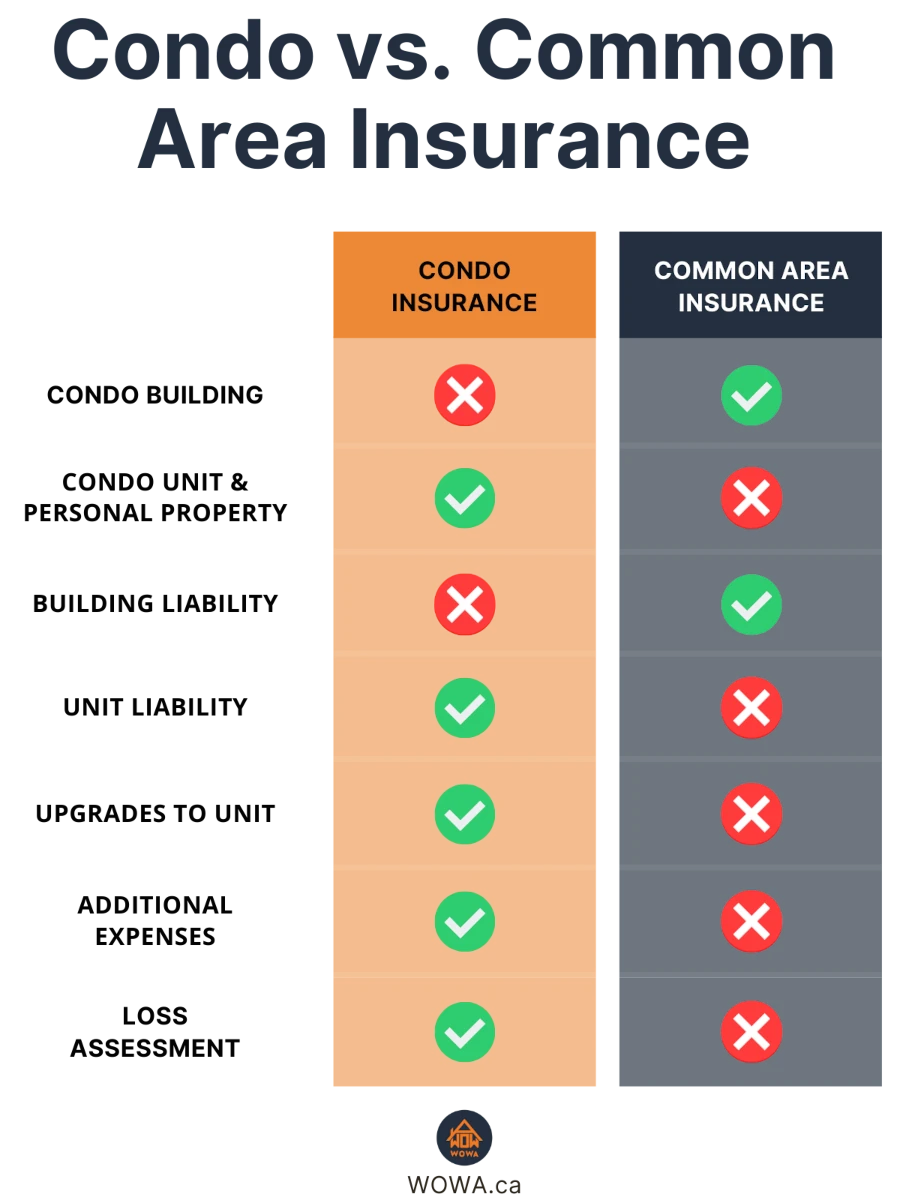

- Condo insurance is designed to fill the coverage gap left by common area insurance.

- You contribute to the building’s insurance through condo fees, which protects shared amenities.

- However, common area insurance typically doesn’t protect the inside of your unit.

- A good condo insurance policy will protect you from unit/property damage, liability, and deductibles needed for damages to the building.

Condo Insurance in Canada

When buying a condo in Canada, you become responsible for your unit but share amenities with other residents. You already pay for common area insurance that protects the building outside of your unit through your condo fees.

However, you're the only owner of your unit, so the common area insurance you pay for does not protect it. This is the purpose of condo insurance - to fill the coverage gap of your unit.

Condo insurance will protect you from damages, injuries, and more that happen inside your unit. For example, if someone hurts themselves in the elevator, the building is responsible. However, if there is an injury within your unit, you are the only owner of your unit, so you are responsible. It is different from home insurance in Canada because your building is already protected, whereas nothing is covered initially with a standalone home.

Continue reading to understand condo insurance in Canada, the coverage options available to you, and the average cost of condo insurance in your city.

Canada's major condo insurance providers

The major condo insurance providers typically offer similar policies. However, there are many home insurance providers in Canada. The "Standard condo insurance coverage" section below provides more detail about the typical coverages. This section will explain some differences between the major insurance providers and their policies.

TD condo insurance

TD Bank is one of the big five banks in Canada. They provide a comprehensive condo insurance package. According to TD, 40% of their home insurance claims are water damage. As a result, they recommend including extended water damage in your policy. It is easy to receive a condo insurance quote from TD, you can use their online to receive one in minutes. You can also learn more about TD bank reviews and mortgage rates here.

RBC condo insurance

RBC is another big five bank in Canada. Their condo insurance policy is similar to TD. In addition, they provide personal property insurance for items inside your car while it's parked on or off your property. A standard deductible for RBC condo insurance is $1000. Along with insurance, everyday banking, and investing services, RBC provides mortgages. RBCs online condo insurance quote tool begins with entering your postal code. You can visit our article on RBC Royal Bank mortgage rates & reviews to learn more.

Co-operators condo insurance

Co-operators provide two tiers of condo insurance packages - Prestige and Classic. Classic has all the standard coverages, whereas prestige has additional protections such as paint spilling on a carpet. To see the cost of Co-operators' condo insurance, you can get a quote on their website in minutes.

Intact condo insurance

Intact is Canada's largest home, auto and business insurance company. Their policy shines through their additional living expenses term. If there's an event that prevents you from living in your unit, they'll pay for a health club membership, storage unit fees, and more. However, it's not specified if their policy includes damages to your unit and liability protection.

BCAA condo insurance

BCAA is a large insurance provider for British Columbia homeowners. With a BCAA membership, you can save up to 20% on your policy. They also provide short-term rental coverage as an addition for AirBnB owners. If you are interested in learning more about BCAA condo insurance, you can visit their webpage explaining their coverage.

Understanding your common area insurance

As mentioned previously, you pay for common area insurance of your building through your condo fees. Before selecting a policy for your unit, it's essential to understand what is already covered through your common area insurance. In Canada, there are generally two types of common area coverages that apply to your unit:

- Fixture coverage: This covers objects physically attached to your unit through bolts, screws, nails, cement, glue, or other means. Typically this includes appliances, plumbing, wiring, and carpets. However, this doesn't cover your personal belongings.

- Restrictive coverage: This doesn't protect anything contained in the walls of your unit. Additionally, it may or may not cover the electrical systems or plumbing associated with your unit. Residents with restrictive coverage need to obtain a better policy to protect their property.

You can find your common area coverage within your condo corporation policy. You'll better understand the coverage options needed to fill the gap with this information. Continue reading below to understand the most common condo insurance coverages.

Typical common area coverage

You partially contribute to the building's insurance through your monthly condo fees. This is known as common area coverage or condo association insurance. The following two policies are generally what is covered through these fees:

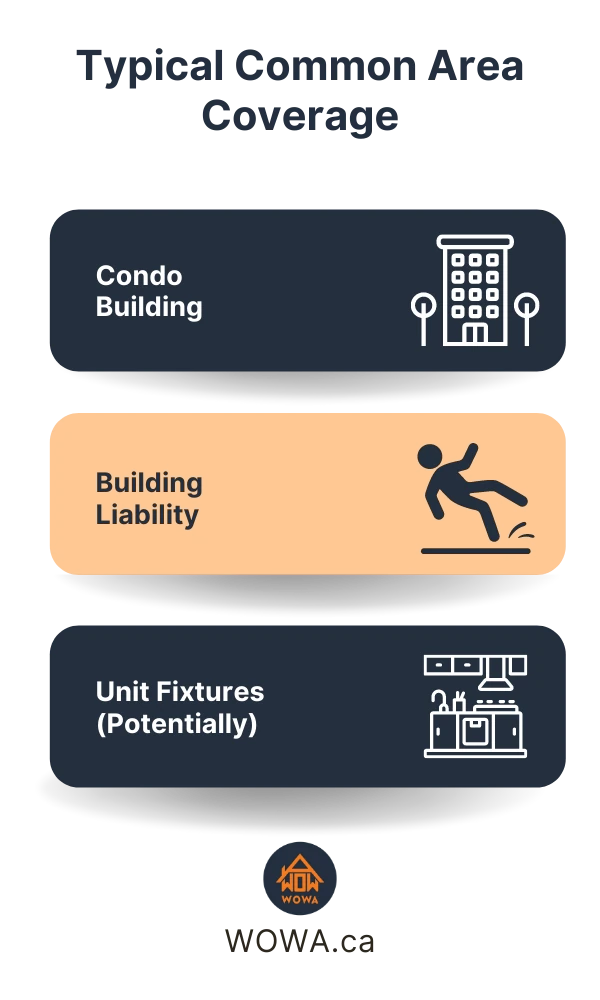

Condo building

This policy insures the shared spaces of your building from damages. Each condo resident partially pays for it as they all share the areas. Shared spaces include the elevator, hallways, gardens, stairs, swimming pool, and more.

Building liability

All building residents are protected through this coverage if a guest is injured in a shared space. However, this only applies to the common areas and not within your unit.

Condo unit (if fixture coverage)

As mentioned above, some common area coverage will protect the original materials and fixtures used to construct your unit. This can include flooring, walls, and the appliances that come with your unit. However, this type of policy varies by condo, so double-check with the policies of your condo association.

Standard condo insurance coverage

When buying insurance for your condo, it's essential to understand the typical coverages available to you and potential additions that may interest you. This section will help you understand the coverages that generally apply to condo insurance policies in Canada. Of course, it's always wise to double-check your policy and ensure these terms are included with your coverage.

Condo unit

This protects your unit from damages. As mentioned above, your common area coverage paid through your condo fees may already include this.

Personal property

Otherwise known as contents insurance, this policy protects your items within your unit if they are damaged for a specified reason. Specified reasons typically include fire, theft, explosions and more. For example, if a fire destroys your clothing, this insurance will provide you with money to buy more.

Typically this covers between $30,000 - $200,000 worth of your clothes, jewelry, etc. However, if you have expensive items such as paintings or fine wine, you should consider enhancing your coverage.

- Storage lockers: Your personal property insurance may or may not cover items stored in a private locker outside your unit. Always double-check with your insurance provider to make sure.

Unit upgrades & improvements

If your condo fees include coverage for your unit, it is likely only for the value at the time of construction. This means that if you move into a renovated unit, you should check with your insurance provider to ensure the value increase is covered.

Additionally, enhancements such as expensive kitchen appliances or fixtures may not be included in the coverage unless otherwise noted. Likewise, changes to your building, including addition or renovation, could impact your coverage (be sure to check). This term typically provides you with a $100,000 cushion of improvement coverage as standard coverage. However, you can always obtain more if need be.

Personal liability

Another term that's generally included with condo insurance is personal liability insurance. This term protects you if you accidentally injure someone within your unit.

For example, imagine you accidentally spilled coffee on your neighbour while handing it over within your unit, and they fall and injure themselves. Generally speaking, you receive $100,000 - $5,000,000 of coverage. This coverage will help pay for any medical bills or legal fees associated with the incident.

Additional living expenses

Coverage for your living expenses is another part of the package. If you cannot live within your unit due to unforeseen circumstances, this will cover the costs of residing elsewhere while damage is fixed.

For example, if a fire or flood ruins your unit and you must stay in a hotel until it's renovated, this coverage would cover the expenses.

Loss assessment coverage

If there is damage to common property that exceeds the common area coverage of your building, then you may need to pay part of the deductible. Loss assessment will pay your portion. Those living in older condos that are breaking down should consider this addition. It typically provides up to $10,000 in coverage.

Popular condo insurance additions

Although the section above includes terms typically included with a condo insurance policy, some additional options will provide you with more coverage. These options cost more money and are explained in detail below.

Extended water damage

This term protects you from sudden water damage that affects your condo unit. Your policy may include one or both of the following terms, so it's best to double-check.

- Overland water: This protects you from damages caused by water flowing across the land from lakes or rivers due to heavy rainfall. If you live close to a body of water, then you should consider including this term. Especially if you have a unit on a lower floor or store belongings in a basement locker. Generally, this will cover up to $50,000 worth of damages.

- Sewer backup: This covers you if the main city sewer drain overflows and backs up into your unit. It will also cover up to $50,000 worth of water damage.

Identity theft

This term covers legal fees and expenses if someone steals your identity and engages in fraudulent activity under it. It typically protects $5,000 worth of financial losses due to the crime.

Loss of rental income (for landlords)

This term guarantees landlords rental income if their tenant is formed to move out due to unlivable conditions.

Occupant damages (for landlords)

This term protects landlords from damages to their property caused by tenants.

Condo insurance Toronto

Condos in the Toronto housing market are expensive. As a result, this city has the highest condo insurance rates on this list. Using the following inputs, the insurance rate below was calculated.

- Unit Description: Two-bedroom condo in a high-rise building

- Size: Under 1,000 sq. feet

- Location: Downtown Toronto (Intersection of King St. W & John St.)

Estimated condo insurance rate: $32 per month or $384 per year.

Condo insurance Vancouver

According to the Vancouver housing market report, Condo apartments in the city had an average selling price of $752,800 in November 2021. Given the high replacement cost of these condos, the insurance rates are also higher than other cities on this list. The rate below was calculated with the following inputs representing an average Vancouver condo.

- Unit Description: Two-bedroom condo

- Size: Under 1,000 sq. feet

- Location: Downtown Vancouver (Intersection of Homer st. and Nelson St.)

Estimated condo insurance rate: $27 per month or $312 per year.

Condo insurance Calgary

Condo apartments in the Calgary housing market saw a 22% average price increase between November 2020/21. As a result, you can expect the condo insurance rates to increase over time. The average Calgary condo insurance rate was calculated below with the following inputs.

- Unit Description: Two-bedroom condo

- Size: 850 sq. feet

- Location: Downtown Calgary (Next to Central Memorial Park)

Estimated condo insurance rate: $23 per month or $276 per year.

Condo insurance Edmonton

Condo apartments in the Edmonton housing market have the lowest average sales price on this list. As a result, condo owners can expect to pay the lowest condo insurance rates. The average Edmonton condo insurance rate was determined with the following information.

- Unit Description: Two-bedroom condo

- Size: Under 1,000 sq. feet

- Location: Downtown Edmonton (Next to Canadian Western Bank Place)

Estimated condo insurance rate: $22 per month or $264 per year.

Nine factors that affect your condo insurance cost

In general, your condo insurance premiums will increase if you are more likely to make a claim. Insurance providers will calculate the probability of you needing to make a claim with variables such as condo age, construction materials, the replacement cost of your insured contents, and more.

With these details, they can determine the risk, probabilities, and cost of insuring you. Therefore, the best way to lower your condo insurance costs is to decrease the likelihood of making a claim. The main factors they look at to determine this are:

- Location

As mentioned in the previous section, the city you live in will significantly affect your insurance costs. Additionally, neighbourhoods known for crime have higher premiums due to the increased chance of theft, vandalism, and break-ins. Those living near areas prone to flooding will also see their premiums increase.

- Replacement cost

The more expensive it is to replace your items and rebuild your unit, the more insurance you will pay. This is because the increased replacement cost is riskier for your insurance provider. Your insurer may need to conduct a home appraisal to estimate your condo replacement cost. Also, make sure to keep your insurance provider updated on any renovations. If your unit is more valuable than they believe, they might not provide you with the total amount of replacement money.

- Property type

Living in a condo townhouse, gated community, or penthouse is evaluated differently because different risks affect them. For example, a condo townhouse will typically have higher insurance costs than a unit in a large building. The insurer will also need to protect the townhouse from exposure to the outside walls. However, the common area insurance already protects the exterior walls in a large condo building.

- Special use

Using your condo for commercial reasons may increase your premiums. This is especially true if your condo is an investment property or Airbnb. Additionally, it's wise to check with your condo board's Airbnb policy.

- Credit score

A better credit score can help you save up to 25% on condo insurance. However, a poor credit score will not increase your condo insurance premiums. You can always use a free credit score checking tool to see how good yours is. It is always recommended to share your credit score when applying for insurance in Canada.

- Renovations & betterment

As mentioned with replacement cost, the more expensive it is to rebuild your unit, the more your insurance will cost. However, most condo insurance policies include a renovation and upgrades term covering up to $100,000 in value increases. It is best to contact your insurance provider before renovations to understand your current assessed replacement value and if the changes will put you over the threshold.

Although renovating a high-end kitchen with marble countertops will increase your condo value, your insurance costs will likely follow. However, renovations that improve the safety of your home may reduce your insurance costs. For example, installing an alarm system will reduce your chances of making a theft claim. As a result, your insurance provider may lower your costs.

- Past claims history

Insurance providers look at your claims history from the past ten years when assessing you. If you make claims more frequently, you are riskier to the insurance company, so you will need to pay more. A rule of thumb is to avoid making claims for minor issues that you can fix yourself.

- Construction materials

The different materials used to build your unit all come with various risks.

- Plumbing: In the 90s, many pipes were built with Kitec. This is a cheaper variant of Pex piping that is more likely to burst. Today, Kitec has cost condo owners thousands of dollars in water damage, and copper piping has become the standard.

- Electricity: Old circuit breakers and electrical wiring increase the chance of fire. As a result, it will cost you more in insurance costs.

- Heating: Today, most condos are heated with a central air furnace and ductwork. However, some older units may use radiators or electric baseboards. Each method of heating has different risks and will affect your insurance costs.

- Pets

Owning aggressive pet species may increase your insurance cost. This is due to personal liability insurance that protects you from the medical expenses associated with any injuries to guests on your property. If you have a dog breed known to be aggressive, then there is a higher probability of needing to make a claim.

Eight ways to get cheap condo insurance in Canada

Use a broker: Brokers shop around for you and find the best insurance policy to meet your needs at a lower price. The savings will be passed on to you.

Group discounts: You can get insurance through your employer or another group that has already organized a deal with an insurer. This may be a professional association or union.

Compare quotes: You can compare condo insurance quotes online to get the best price for your insurance policy. This may require you to share information about your unit, square footage, common areas and more. Just be sure to read the fine print to know how this will affect you when you renew.

Special offer: Your insurer may have a special offer based on your previous claims history, credit score and other factors. Before accepting an insurance policy, be sure to inquire about any deals you could qualify for.

Senior discount: If you are over 55, some insurers may allow you to get discounted condo insurance in Canada.

Raise your deductible: If you are willing to assume more risk in the event of a claim, then it could pay off in lower premiums. You can raise your deductible (the amount you are responsible for paying before insurance kicks in) to reduce your monthly condo insurance payments.

Reduce coverage: If you have savings, you can self-insure against loss or damage by increasing your deductible and reducing your coverage limits on certain items. For example, if you have an expensive TV, then it may be worthwhile to lower your condo insurance policy on this item.

Bundle policies: Sometimes, you can cut the cost of your multiple insurance policies by bundling them together under one company. However, be sure to compare each quote, so you don't lose any savings to commissions and other fees.

How to apply for condo insurance

First, you need to decide on an insurer. Then, you will need to provide basic information about yourself, such as; your name, age, and gender. You can ask your current insurance broker or agent for recommendations based on their previous clients.

You'll also need to provide information about the condo, including:

- The year of construction

- Age of roof

- Type of heating

- Construction materials

- If there's a fire alarm system

- The total value of your belongings

When shopping around for condo insurance in Canada, remember to compare quotes on a like-for-like basis. Make sure you're not overpaying on your premiums because you don't know how to shop for insurance or that you were given advice by an agent who might be getting more commission from one company over the other.

Although you are not legally required to have condo insurance, Canadian mortgage lenders require it. Condo insurance premiums are highly variable from one insurer to another, and you must shop around to get the best value for your money.

The bottom line

Condo insurance is mandatory to get a mortgage in Canada when buying a condominium unit, and it's important that you find the best possible price. This will require shopping around and comparing quotes from different insurers so you can be sure to get the most out of your money. Condo insurance premiums are highly variable, so make sure you read all fine print before agreeing on a policy with an insurer.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.