Rental Property Mortgage

All You Need to Know

What You Should Know

- There are three variations to rental property mortgages: commercial, residential, and CMHC insured.

- Rental property mortgage rates are typically higher than regular mortgage rates.

- You can use up to 50% of the future rental income to help you qualify for the mortgage.

Special Rental Property Mortgage Rates

| Mortgage Term | Lender | Rate |

|---|---|---|

1-YEAR FIXED | CIBC More From CIBC | 4.89% |

2-YEAR FIXED | Frank Mortgage | 4.59% |

3-YEAR FIXED | Frank Mortgage | 4.64% |

4-YEAR FIXED | Frank Mortgage | 4.79% |

5-YEAR FIXED | Frank Mortgage | 4.84% |

7-YEAR FIXED | CIBC More From CIBC | 5.11% |

10-YEAR FIXED | CIBC More From CIBC | 6.79% |

3-YEAR VARIABLE | CIBC More From CIBC | 4.05% |

5-YEAR VARIABLE | CIBC More From CIBC | 4.10% |

Understanding mortgages in Canada can be overwhelming. An investment property mortgage has unique features that make them different from mortgages for owner-occupied residential properties. For example, owner-occupied properties can be high-ratio, meaning that downpayment can be as low as 5%-10%. In contrast, a non-owner occupied property requires a minimum of 20% downpayment even with CMHC insurance.

If you're thinking of buying an investment property, this article will simply explain rental property mortgage characteristics, interest rates, income tax claims, and qualification criteria. Continue reading to become an expert in 5-10 minutes.

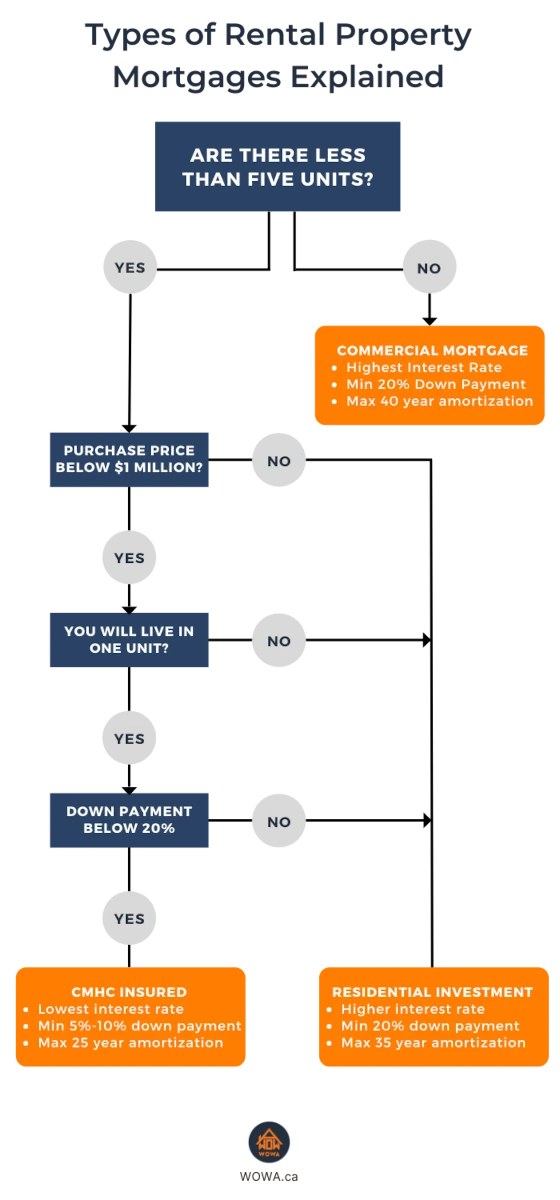

Investment Property Mortgages

Initially, your mortgage characteristics will depend on the purchase price and number of units your investment property has. To qualify for a down payment of less than 20%, your property must meet the following criteria:

- Less than five residential units

- The purchase price is less than $1 million

- Intend to live in one of the units

For first-time real estate investors, we recommend meeting all criteria. You can still receive a small rental loan (mortgage) if you don't meet these criteria. However, you will need a minimum 20% down payment. This process is known as "house hacking" because the other 1-3 units will contribute to your monthly mortgage payments and ideally leave you with some rental property income. It’s a similar concept to the BRRRR method, where your tenant’s rent payments are used to pay your mortgage.

When considering CMHC-insured mortgages, buying a property with more than four units requires a commercial mortgage, while properties with less than five units use a residential mortgage. When considering uninsured mortgages, buying a property with more than six units requires a commercial mortgage, while properties with less than seven units use a residential mortgage.

A commercial mortgage has higher interest rates and a stricter qualification process. A commercial mortgage also may have net-worth requirements. For example, a lender might require your net worth to exceed 25% of the loan value.

A commercial mortgage is often more complicated and costly than a residential mortgage. For example, a commercial mortgage requires an environmental site assessment (ESA) and might require a building condition report. The ESA aims to determine whether contaminants are affecting the property. ESA should be performed according to provincial environmental regulations. A building condition report is a more involved and costly version of the building inspection which is also common for residential purchases.

Owner-Occupied vs. Non-Owner-Occupied

Owner-occupied means you will live in one unit. You will be expected to start living in the property before a year passes from the closing. You are also expected to continue living there for at least a year. As a result, the investment property will be considered your primary residence. For example, a duplex has a single owner that owns both units. The owner might live in one unit and rent out the other unit.

You will be eligible for a lower down payment and better interest rates for your primary residence. Your minimum down payment can range between 5%-10%, meaning an LTV of 90%-95%. However, if the property has more than four units or a purchase price above $1,000,000, a minimum down payment of 20% is required. Depending on your lender, you may be able to move out and rent your previous unit after one year.

Insured Residential Mortgage

| Homeowner Loans | Small Rental Loans | |

|---|---|---|

| Minimum Down Payment | 1-2 units If price is less than $500,000, 5% of the price, otherwise $25,000 + (Price - $500,000)/10. 3-4 units Price/10 | 20% |

| Maximum Amortization | 25 years with CMHC, otherwise 35 years | 25 years |

Down Payment

If you don't live in one unit for at least a year, you'll need a 20% down payment. However, if you live in one unit, the purchase price is less than $1 million, and there are less than five units in the property, you're eligible for a minimum 5% to 10% down payment. The lower down payment is due to mortgage default insurance, so you'll need to meet all CMHC mortgage rules. A benefit of mortgage default insurance is that you'll likely receive better mortgage rates in Canada.

You can pay a minimum 5% down payment on the first $500,000 in value of your property. However, any value between $500,000 - $1,000,000 must have a 10% minimum down payment. For example, a $700,000 property would need a down payment of at least $45,000 (500,000*5% + 200,000*10%).

According to CMHC, Canada’s national housing agency, when you intend to reside in a property with 1 to 4 units, its mortgage would be a homeowners loan. A homeowner loan for a 1-2 unit property can have a loan-to-value (LTV) ratio as high as 95%, which means a down payment as low as 5%. A homeowner loan for a 3-4 unit property can have an LTV as high as 90%, which means a down payment as low as 10%. A single-unit property where the purchaser does not intend to reside is not eligible for CMHC mortgage default insurance.

CMHC also offers mortgage default insurance for small rental loans. A small rental loan is a residential mortgage for a property containing 2-4 units where the purchaser intends to rent all the units. Small rental units have a maximum LTV of 80%, which is equivalent to a 20% down payment.

Amortization Period

Your mortgage amortization is the number of years it will take to pay off your mortgage fully. Generally, real estate investors prefer more extended amortization periods because it reduces their monthly mortgage payments. As a result, a longer amortization will provide you with better cash flow each month.

Depending on the type of property you purchase, you can qualify for a maximum amortization of 25 or 35 years for residential property. If you have CMHC mortgage default insurance (which is compulsory with a down payment of less than 20%), then you'll have a maximum amortization of 25 years.

If your down payment exceeds 20%, you can extend your amortization. Some Canadian Lenders offer 30-year mortgages and 35-year mortgages. You will not need to live in a unit to do this. However, there is an amortization extension fee, and you will have higher interest rates than a 25-year mortgage. Ideally, your monthly mortgage payments will be smaller, but given the variables, it's helpful to use a mortgage payment calculator to compare.

Mortgage Default Insurance

By Canadian law, you must have mortgage default insurance if you have a high-ratio mortgage meaning a down payment of less than 20%. The insurance protects your mortgage lender if you default on your loan. Homeowner purchase program is the most common mortgage default insurance program. To participate in this program, you must purchase a property with four or fewer units valued below $1 million and live in a unit for a year.

Otherwise, if your down payment is 20% of the property price or more, you will not need mortgage default insurance. Although CMHC insurance may provide you with lower mortgage rates, there are additional minor fees.

Calculating Rental Property ROI

Your rental property ROI is a measure of your return on investment. There are a few ways to calculate it, but Cash-on-Cash Return on Investment (CoC ROI) is the best method. It is calculated as follows:

ROI = Net Operating Income / Purchasing Costs

You may also include property appreciation to get the true ROI. However, the easiest way to determine this is using a rental property ROI calculator.

Claiming Mortgage Payments on Rental Property

You can deduct mortgage interest payments to lower your taxable income in Canada. However, you can only do this with investment properties and not primary residences. You must factor out your proportionate square foot percentage from the deduction if you live in a unit. For example, if you own a 5,000 sq ft. rental property and inhabit a 1,250 sq ft. unit, then you can only deduct 75% ((5000-1250)/5000) of the mortgage interest costs.

Should you pay off the rental property mortgage?

If your property generates cash flow - meaning profits, you should keep your mortgage. However, paying off the mortgage could be a good idea if your property is losing money. In general, mortgage debt enhances your return on investment because you only need a small down payment to receive the total property appreciation and rental income. There are also the tax benefits of mortgage debt, such as deductions.

If your property generates profits, your money would be better spent as a down payment for another rental property. Instead of one fully paid off property, you could have two that appreciate in value and still provide you with rental income.

Each year, you will receive a T5013 slip from your mortgage lender showing the amount of interest paid. You must fill out Line 8710 with the appropriate amount to claim the mortgage interest payments. Additionally, you may claim the costs directly associated with receiving the mortgage, such as:

- Legal fees

- Mortgage broker fees

- Application & processing fees

With the deduction, you will lower the total amount of tax you need to pay. Some other popular rental expenses you can deduct in Canada include:

- Rental property insurance

- Repairs and maintenance

- Property taxes

- Utilities

- Travel expenses

- And more

Tools for Landlords

As a landlord, two crucial factors ensure tenants continue to pay while removing bad ones as quickly as possible. Even if your tenant doesn't pay, you're still expected to pay for mortgage payments, property taxes, and more. This means one missed tenant payment can send you into more debt to make up for your obligations.

To prevent this from happening, one tool is rental income insurance. This coverage provides you with guaranteed rental income if your tenant decides not to pay. You should also get familiar with the eviction process in your province. The easiest way to remove a tenant is to buy them out of their lease agreement at the cost of one to two months' rent. This approach is known as "cash for keys" and can save you thousands of dollars worth of legal fees, damages, and missed rent.

Rental Property Mortgage Requirements

It can be easier to qualify for a rental property mortgage in Canada. This is because you can use some of the rental income you are receiving in the future to meet requirements. You will always need the standard required documents to purchase a property in Canada.

However, specific to rental properties, you will also need to establish the amount of rent. This can be done either through existing rental agreements or through an opinion of market rent which can be provided by an appraiser. If current rental agreements are not available, your mortgage broker or mortgage lender would ask for an opinion of market rent when they are ordering a home appraisal for your mortgage.

Your mortgage lender will then use this information to calculate your debt coverage ratios. They will also make sure you meet the minimum credit score requirements.

Rental Income Treatment

Qualification for residential mortgages is often based on gross and total debt service (GDS and TDS) ratios. Both of these ratios have the borrower’s income in their denominator. The numerator in GDS includes housing expenses, mainly mortgage principal repayment, mortgage interest, property taxes and heating costs. The numerator in the TDS ratio includes the numerator in the GDS ratio in addition to any other debt payment obligations.

Rental income can be included in your earnings either as gross rental income or net rental income. In the gross inclusion method, the lender can include as much as 50% of the rent you are expected to receive. In this method, taxes and heat may be excluded from the numerator of debt service ratios.

In the net rental income method, the lender estimates the operating expense of the property.

Net Rent = Gross Rent - Property Operating Expenses.

Net rent is added to the borrower’s income for the purpose of calculating affordability ratios. Gross rental income is often used for smaller properties with a homeowner or small rental mortgage while net rental income method is often used for commercial mortgages.

The Bottom Line

Although your lender can decline your mortgage application, you can take steps to improve your chances of approval. Investment property mortgages can be similar to conventional mortgage loans. However, if your property doesn't meet CMHC mortgage default insurance regulations, the process gets more complex. Although you can still receive a mortgage without meeting the criteria, you’ll have a higher down payment and interest rate.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.