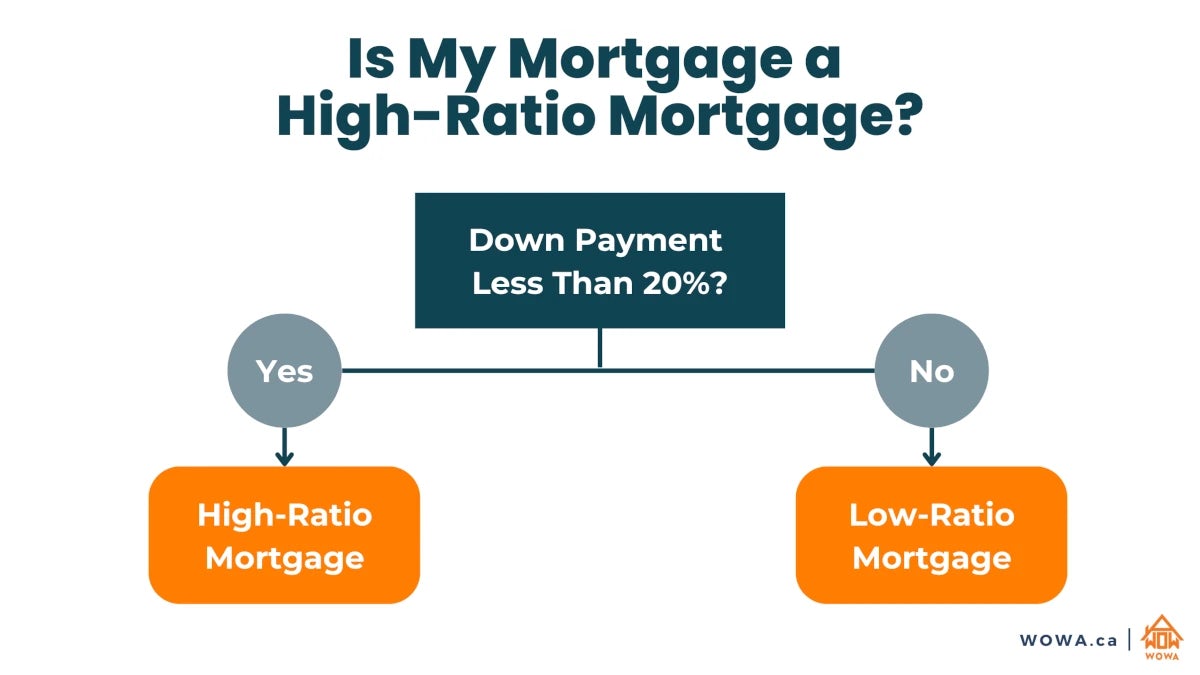

What is a High-Ratio Mortgage?

What You Should Know

- A high-ratio mortgage is when you make a down payment of less than 20%.

- High-ratio mortgages require mortgage default insurance, which is only possible for homes with a price of $1.5 million or less.

- Since they are insured, high-ratio mortgage rates are often lower than conventional low-ratio ones.

What is a High-Ratio Mortgage?

A high-ratio mortgage allows you to purchase a home with a down payment as low as 5%. It refers to a mortgage where your loan-to-value (LTV) ratio is greater than 80%, meaning your down payment is less than 20%.

In contrast, a low-ratio mortgage—also known as a conventional mortgage—has an LTV ratio of 80% or less, which corresponds to a down payment of at least 20%.

Because high-ratio mortgages involve borrowing a larger portion of the home's value, they carry more risk for lenders. To offset this risk, mortgage default insurance is required for high-ratio mortgages by most lenders, including banks and credit unions.

High-Ratio Mortgages and Loan-to-Value Ratios

Your mortgage’s loan-to-value ratio (LTV) is the amount that you are borrowing compared to the purchase price or appraised value of the home. For example, if you make a 10% down payment on a home, your mortgage’s LTV ratio will be 90%. Likewise, if you make a 20% down payment, your LTV ratio is 80%.

LTV Ratio Calculation

If your mortgage’s loan-to-value (LTV) ratio is greater than 80%, it is considered a high-ratio mortgage. In Canada, the minimum required down payment is 5% for homes priced up to $500,000, and 10% on the portion of the price above $500,000. However, if the purchase price is above $1.5 million, a minimum down payment of 20% is required on the entire price, making the mortgage ineligible for insurance. A 5% down payment results in a maximum LTV ratio of 95%.

See how your down payment affects affordability with our mortgage affordability calculator.

Table of Loan-to-Value Ratios for High-Ratio Mortgages

| Down Payment | Loan-to-Value (LTV) Ratio |

|---|---|

| 5% | 95% |

| 10% | 90% |

| 15% | 85% |

| 19.9% | 80.1% |

High-Ratio Mortgages vs. Conventional Mortgages

Mortgage loan insurance is required for high-ratio mortgages, but they are not required for conventional mortgages in Canada. Mortgage insurance is offered by the Canada Mortgage Housing Corporation (CMHC) as well as other private insurers. CMHC mortgage insurance is not free. You will need to pay CMHC mortgage insurance premiums based on your mortgage’s loan-to-value ratio.

Note: Not all conventional mortgages are treated the same. Some low-ratio mortgages that meet insurer criteria (such as limited amortization and no refinancing) are considered "insurable" by lenders and may receive rates closer to insured mortgages. Others, such as refinanced mortgages, are "uninsurable" and often have higher rates.

High-Ratio and Conventional Mortgage Comparison

| High-Ratio Mortgage | Conventional Mortgage | |

|---|---|---|

| CMHC Insurance | Required | Not Required |

| Maximum Amortization Period | Usually 25 years for insured mortgages; 30 years available for eligible first-time buyers and eligible new-build purchases | Commonly 30 Years, some lenders may go to 35 years |

| Mortgage Rates | Typically Lower | Typically Higher |

| Maximum Home Price | $1,500,000 | No Limit |

Insurance Premiums

High-ratio mortgages require mortgage default insurance, provided by CMHC or private insurers. This insurance comes with a premium, calculated as a percentage of your mortgage amount and typically added to your loan balance.

As of December 15, 2024, mortgage insurance is generally available for properties valued up to $1.5 million, following an increase from the previous $1 million cap that had been in place since 2012. Homes priced above $1.5 million are not eligible for mortgage insurance, meaning a minimum down payment of 20% is required on the full purchase price, resulting in a conventional (uninsured) mortgage.

Use our CMHC insurance calculator to estimate your premium.

Mortgage default insurance protects the lender—not the borrower—in the event of a default. While borrowers pay the insurance premium, they are still responsible for repaying the mortgage and any shortfall if the property is sold after default.

Mortgage insurance in Canada did not have a strict maximum home price limit until 2012, when a $1 million cap was introduced. This cap remained in place until it was increased to $1.5 million in December 2024.

Amortization Period

The maximum amortization period allowed for high-ratio mortgages is 25 years. Eligible first-time buyers and eligible buyers of newly built homes can extend this to 30 years. If you would like a longer amortization period, then you would need to use a conventional mortgage. A longer amortization period allows for your mortgage payments to be spread out over a longer time period, resulting in smaller monthly mortgage payments. While the amount of your mortgage payments will be smaller, you will need to pay a larger down payment upfront in order to qualify for a conventional mortgage. A longer amortization period also means that you will be paying more interest over the lifetime of your loan.

Mortgage Rates

High-ratio mortgages are insured mortgages. Insured mortgages usually have lower mortgage rates than uninsured conventional mortgages. While you may get lower mortgage rates with a high-ratio mortgage, you still have to pay for mortgage default insurance. However, your mortgage interest savings may even outweigh the cost of mortgage insurance.

Note: If you refinance your mortgage (for example, to access equity or increase your loan amount), the new mortgage is typically no longer insured, even if your original mortgage was. As a result, you may lose access to insured mortgage rates going forward. However, if you switch lenders at renewal or port your mortgage to a new property without increasing the loan, the insured status is generally preserved.

CMHC High-Ratio Mortgage

CMHC insurance premiums are paid by you, not your mortgage lender. You can add CMHC premiums onto your mortgage amount or you can pay it upfront.

CMHC premiums are calculated as a percentage of the total amount of your mortgage. The premium will vary depending on the LTV ratio of your mortgage, with the premium increasing for higher LTV ratios. You can use a CMHC insurance premium calculator to estimate the premium payable for your mortgage.

High-Ratio Mortgage Calculation

You can use our mortgage payment calculator to compare what you'll actually pay under different down payment scenarios. The example below walks through a $500,000 home purchase using illustrative rates of 4.64% for an insured (high-ratio) 5-year fixed mortgage and 5.14% for an insurable (low-ratio) 5-year fixed mortgage, both amortized over 25 years (these were CIBC rates in August 2024).

High-Ratio Mortgage (5% Down)

With a 5% down payment of $25,000, your mortgage amount is $475,000 — a high-ratio mortgage. CMHC charges a 4.00% premium at this loan-to-value ratio, adding $19,000 to the mortgage balance for a total financed amount of $494,000.

At 4.64% over 25 years, your monthly payment is $2,773. Over the life of the mortgage, you'll pay $337,821 in interest — this figure includes interest on the CMHC premium, since the premium sits on top of your principal and accrues interest just like the rest of the loan.

Low-Ratio Mortgage (20% Down)

With a 20% down payment of $100,000 on the same home, your mortgage is $400,000 with no CMHC premium required. At 5.14% over 25 years, your monthly payment is $2,358, and you'll pay $307,520 in interest over the life of the loan.

Is a High-Ratio Mortgage Cheaper than a Low-Ratio Mortgage?

The high-ratio mortgage has a lower interest rate, but a larger loan and a $19,000 insurance premium. The low-ratio mortgage has a higher rate, but a smaller loan and no insurance. Which one actually costs more depends on how you measure it:

- In absolute dollars, the high-ratio mortgage pays more total interest — $337,821 vs $307,520, a difference of $30,301 — because the loan is larger.

- As a share of principal, the high-ratio mortgage pays less interest — about 71% of its $475,000 principal, vs 77% for the low-ratio's $400,000 — reflecting the lower interest rate.

The table below extends the comparison to 10% and 15% down payments. The bottom row, "Total Cost," is the apples-to-apples figure: what you actually spend over 25 years, including the down payment, all mortgage payments, and the CMHC premium.

Interest Costs — High-Ratio vs Low-Ratio

| High-Ratio (5%) | High-Ratio (10%) | High-Ratio (15%) | Low-Ratio (20%) | |

|---|---|---|---|---|

| 5-Year Fixed Rate | 4.64% | 4.64% | 4.64% | 5.14% |

| Down Payment | $25,000 | $50,000 | $75,000 | $100,000 |

| Mortgage Principal | $475,000 | $450,000 | $425,000 | $400,000 |

| CMHC Premium | $19,000 | $13,950 | $11,900 | $0 |

| Monthly Payment | $2,773 | $2,604 | $2,452 | $2,358 |

| Total Interest | $337,821 | $317,271 | $298,773 | $307,520 |

| Interest as % of Principal | 71% | 70.5% | 70.3% | 77% |

| Total Cost (Down + Principal + Interest + CMHC) | $856,821 | $831,221 | $810,673 | $807,520 |

In this example, the 20%-down low-ratio mortgage produces the lowest Total Cost — but only by $49,301 vs the 5%-down scenario, despite requiring an additional $75,000 of cash upfront. That trade-off is what the next section explores.

One caveat: the comparison assumes a constant mortgage rate for the entire 25 years. In practice, you'll renew every 5 years (or less) at whatever rate prevails, so the lifetime interest figures should be treated as illustrative rather than predictive.

What If You Invested the Difference Instead?

The 20%-down option is the cheapest in the table above, but it ties up $75,000 more cash upfront than the 5%-down option. What if you put less down on the same home and invested the rest?

Frame the question this way: assume you have $100,000 of cash available, and you can allocate it however you want between the down payment and an investment at a 2% annual return compounded monthly held for 25 years. Putting more down reduces the mortgage cost; putting more in the investment grows the cash on the side. The table below shows the trade-off at each down payment level:

- Total Cost is the cost of the mortgage on its own — Down Payment + Principal + Interest + CMHC, as in the first table.

- Net Cost is Total Cost minus the investment gain earned on whatever cash you didn't put down (i.e. $100K − down payment, grown at 2% for 25 years).

The two anchor scenarios are labelled in the first column: Path B at the top is "5% down + invest $75K"; Path A at the bottom is "20% down + invest nothing."

Down Payment vs Investment Trade-Off

| Down Payment | Total Cost | Net Cost | |

|---|---|---|---|

| Path B: 5% Down + Invest | $25,000 (5% down) | $856,821 | $808,219 |

| 10% Down | $50,000 (10% down) | $831,221 | $798,819 |

| 15% Down | $75,000 (15% down) | $810,673 | $794,472 |

| Path A: Put It All Down | $100,000 (20% down) | $807,520 | $807,520 |

At a 2% investment return, the cheapest option isn't either extreme — it's 15% down + investing the remaining $25K, at $794,472. That beats Path A (20% down, no investment, $807,520) by about $13,000 and Path B (5% down, invest $75K, $808,219) by about $14,000.

Why does 15% win? Two effects work together:

- Putting more down within the insured range (any down payment from 5% up to just under 20%) reduces both your mortgage principal and your CMHC premium, while keeping you at the lower insured mortgage rate of 4.64%. Each dollar of additional down payment in this range pays back through lower interest and lower CMHC.

- But the moment you reach 20% down (LTV of 80%), the mortgage stops being insured, and the rate jumps to the uninsured 5.14% in this example. Avoiding the CMHC premium entirely saves you $11,900, but the higher rate on the (still substantial) $400K balance costs you an extra $8,747 in lifetime interest, eating most of the gain. Net effect: going from 15% down to 20% down only saves $3,153 on the mortgage side — far less than the $16,200 investment gain you forfeit by tying that $25,000 into the down payment instead of investing it.

The implication is that the "optimal" down payment in this example is actually just under 20% — say 19.9%, putting you at LTV 80.1% and still in the insured tier. That preserves the lower rate while extracting maximum savings on principal and CMHC.

This conclusion is sensitive to the assumptions baked into the table:

- The rate spread between insured (4.64%) and uninsured (5.14%) mortgages. A narrower spread would shrink the penalty for crossing 20% down. A wider spread would make it worse.

- The 2% investment return. Returns meaningfully above 2% reward putting less down (more invested); returns below 2% reward putting more down. The crossover where Path B (5% down) ties Path A (20% down) is at about a 2.02% investment return.

Other factors that matter and that the table doesn't capture:

- Tax treatment. Investment income in a non-registered account is taxable, which lowers the effective return and pushes the optimum toward putting more down. A TFSA or RRSP preserves more of the gain.

- Renewal risk. Your rate at renewal could be higher or lower than the one you start with. A rate increase hurts the larger mortgage more.

- Liquidity. A smaller down payment preserves cash for emergencies or other goals — that flexibility has value even when it doesn't show up in the total-cost math.

The practical takeaway: the cheapest down payment is often the largest one that still keeps your mortgage insured — typically just under 20%. Putting exactly 20% down trades a small avoided CMHC premium for a much larger increase in interest, and putting only 5% down requires the investment side to do all the heavy lifting. The sweet spot lives in between.

FAQ: High-Ratio Mortgages in Canada

High-ratio (insured) mortgages often have lower interest rates because the insurance reduces risk for lenders. However, whether they are actually cheaper overall depends on how long you keep the mortgage. Since you must pay an upfront insurance premium, shorter holding periods (such as selling or refinancing within a few years) may make insured mortgages more expensive, while longer holding periods can allow the lower interest rate to offset the cost of insurance.

A high-ratio mortgage is a mortgage with a loan-to-value (LTV) ratio above 80%, meaning the borrower makes a down payment of less than 20%. These mortgages by law require mortgage default insurance, which protects the lender in case of default.

Yes. In Canada, mortgage default insurance is mandatory for all home purchases with a down payment below 20%. This requirement applies as long as the property and borrower meet the insurer's eligibility criteria.

The minimum down payment depends on the home price:

- 5% on the first $500,000

- 10% on the portion above $500,000

- 20% on the full price if the home costs more than $1.5 million

This tiered structure means that the effective down payment percentage increases as the home price rises.

Yes. As of December 2024, mortgage insurance is available for homes priced up to $1.5 million. This allows buyers to make a down payment below 20% on homes between $1 million and $1.5 million, provided they meet income and qualification requirements.

A 20% down payment gives you an LTV of 80%, which is the cutoff for a standard low-ratio mortgage. At that point, mortgage default insurance is not required, and the mortgage is typically treated and priced as uninsured.

Not necessarily. Avoiding mortgage insurance requires a larger down payment, which has an opportunity cost. In some cases, using a smaller down payment with an insured mortgage can allow buyers to enter the market sooner or preserve liquidity, even after accounting for the insurance premium.

No. Mortgage default insurance cannot be removed from your mortgage after purchase, even if your equity increases over time. However, since the insurance premium is typically paid upfront and added to your mortgage balance, there is no ongoing premium to eliminate. This means there is generally no financial benefit to "removing" the insurance later.

If you refinance your mortgage, the new loan is usually not insured, even if the original mortgage was. This means you may no longer qualify for insured mortgage rates after refinancing, except for specific insured-refinance programs, such as eligible secondary-suite refinancing. However, if you simply renew your mortgage without changing the amount or terms significantly, the insured status is typically preserved.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.