ROI Calculator for Canadian Investments

Enter your Amount Invested and Amount Returned.

Important: If your investment had multiple deposits, withdrawals, dividends, or rental payments, this calculator will treat everything as if it happened at the end. For multi-cash-flow cases, use the IRR Calculator.

About This ROI Calculator

This ROI calculator is designed to calculate the return on investment (ROI) for any Canadian investment. To use the ROI calculator, enter your initial investment amount and the final value of the investment. This gives you your ROI. To calculate your annualized ROI, also known as cumulative annual growth rate (CAGR), simply enter the length of the investment in addition to the initial and final investment amounts. This then calculates the annualized return of the investment.

This page will take a look at ROI, or return on investment. We'll explore what ROI is, how it is calculated, and some of the ways it can be measured. Then, we'll go over some alternatives to ROI that might be a better fit for certain situations.

Simple ROI does not account for timing.

This calculator assumes one initial investment and one final value. If your investment had multiple cash flows (rent, dividends, contributions, withdrawals), ROI will combine them into a single ending amount and ignore timing.

For timed cash-flow accuracy, use the IRR Calculator instead.

ROI Formula

The formula for return on investment (ROI) is:

Alternatively, the formula for annualized ROI is:

Where n = Number of years

In both ROI formulas, multiplying the result by 100 gives you the ROI in percentage form. Otherwise, you will get your ROI in decimal form.

Annualized ROI is a good measure of profitability for simple situations when you purchase an investment and sell it on a future date. For more complicated situations where there can be many cash inflows and outflows relating to an investment, one should use the internal rate of return as a measure of profitability.

Related tools:

- CAGR Calculator (for annual growth rate)

- IRR Calculator (for multiple cash flows)

- Investment Return Calculator (for contributions over time)

What is ROI?

ROI stands for return on investment, and it measures the amount that an investment returns or the final value of an investment relative to the investment's cost. It is usually expressed as a percentage or a ratio. A positive value means that the investment has generated a return greater than its cost, while a negative value indicates that the investment incurred loss.

ROI can be used to evaluate a wide variety of investments, including stocks, bonds, real estate, and businesses. ROI is also a popular metric for evaluating the performance of marketing campaigns and other initiatives. In digital advertising, another term for ROI is return on ad spend (ROAS).

For calculating ROI, you would have to add all the cash outflows to derive the Amount Invested and all the cash inflows to derive the Amount Returned. Thus, ROI does not take into account the time value of money. Another limitation of ROI is that it only considers financial measures and does not take into account other factors that may be important, such as the riskiness of the investment. In order to consider risk, you'll want to use a risk-adjusted return ratio.

How to Calculate ROI

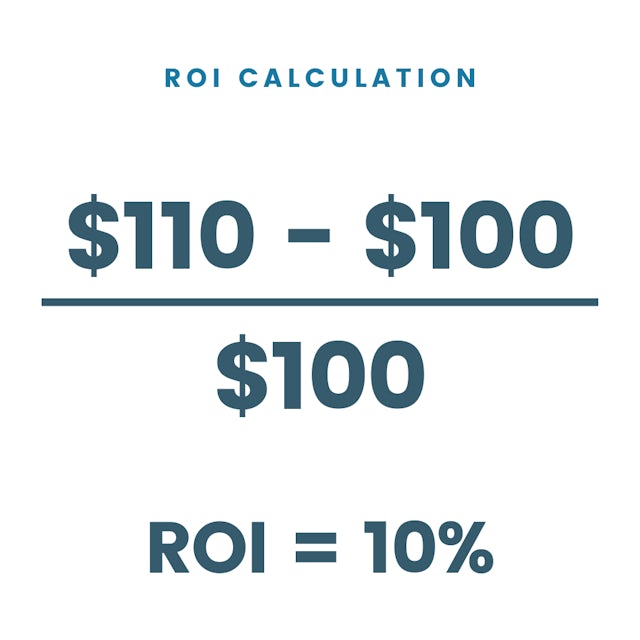

The most common way to calculate return on investment is to take the difference between the initial investment and the final value of the investment, and then divide that by the initial investment.

For example, if you invested $100 in a stock and it went up to $110, your ROI would be (110-100)/100, or 10%.

ROI can also be used to calculate how much money you made from an investment in relation to how much you spent. For example, if you spent $100 on a new marketing campaign and it generated $300 in profit, your ROI would be 200%.

Calculating Annualized ROI

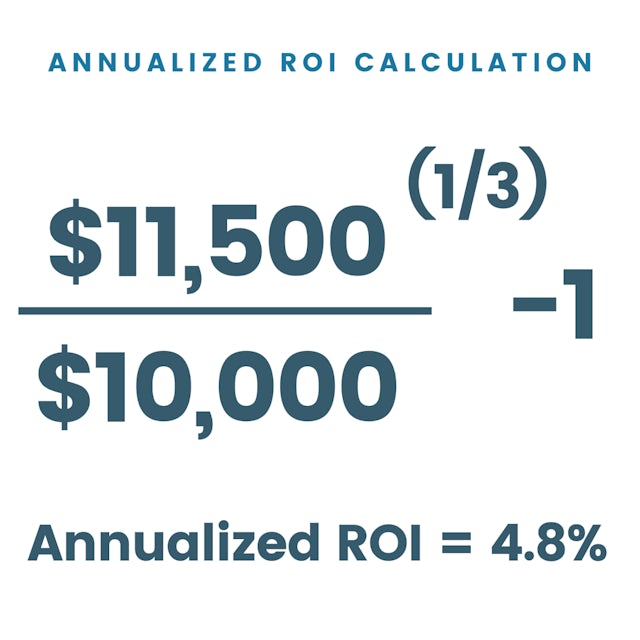

Calculating annualized ROI is slightly different, as it involves the number of years the investment was held for. Annualized ROI gives you the annual return for the investment, which makes it a better metric to compare between different investments, especially those held for different lengths of time. That's because investments might be held for different periods of time.

Annualized ROI can be calculated using the simple formula,

where P is the initial investment, F is the final value of the investment, and n is the number of years the investment is held.

For example, let's say you have a stock that you purchased for $10,000. After three years, it's worth $11,000, and you receive $500 in dividends. Then, based on the annualized ROI calculation, your annualized ROI would be [($11,500/$10,000)^(1/3)] - 1] = 4.8%. Meanwhile, the simple ROI will be 15%. The table below shows how the annual ROI can differ based on the length of investment, even when the ROI is the same.

| Initial Investment | $10,000 | $10,000 |

| Capital Gains | $1,000 | $1,000 |

| Dividends | $500 | $500 |

| Final Investment Value | $11,500 | $11,500 |

| Years | 1 Year | 3 Years |

| Basic ROI | 15% | 15% |

| Annualized ROI | 15% | 4.8% |

ROI and Canadian Taxes

The return you calculate using this tool is your gross ROI — it does not account for income taxes, which can significantly reduce your actual take-home return.

How your investment returns are taxed in Canada depends on the account type and the nature of the return:

Capital gains are only 50% taxable (the inclusion rate), meaning only half of your gain is added to your income and taxed at your marginal rate.

Dividends from Canadian corporations benefit from the dividend tax credit, which reduces the effective tax rate compared to regular income.

Interest income (e.g., from GICs or bonds) is fully taxable as regular income.

TFSA: Returns earned inside a TFSA are completely tax-free, so your gross ROI equals your after-tax ROI.

RRSP: Returns grow tax-deferred. You'll pay income tax on withdrawals, so your realized after-tax ROI depends on your marginal rate at the time of withdrawal.

Return on Ad Spend

Return on Ad Spend (ROAS) is a key metric that ecommerce businesses use to measure the success of their digital marketing campaigns. Both ROAS and ROI are measures of profitability, but they differ in how they are calculated.

ROAS is a measure of how much revenue is generated for every dollar spent on advertising. ROI, on the other hand, looks at the overall profitability of a campaign, taking into account both ad spend and other associated costs.

To calculate ROAS, simply divide total revenue associated with the campaign by the total ad spend:

For example, if an ecommerce business spends $100 on Google Ads and generates $5,000 in revenue from those ads, their ROAS would be 5:1, or $5 of revenue for every $1 spent.

On the other hand, ROI will also take into account other costs for a business. For example, a business will need to subtract the cost of their product, and not consider just the cost of the ad campaign.

What Is a Good Return on Ad Spend?

A good return on ad spend is anything above 4:1, or 400%. However, it's common for most advertisers to see a ROAS that hovers around 200% to 300%. According to Neilsen, the average ROAS for online display ads is 263%, while magazines have a ROAS as high as 394%!

ROI for Common Investments

Did you know that the average annual net total rate of return for Canadian equities over the past 10 years (as of March 30, 2026) was 11.5%? That's for the S&P/TSX Composite Index (TSX). However, this figure can change based on the time frame chosen. For example, the annual rate of net total return for the TSX from January 2000 to March 2026 was 8.0%. The returns of Canadian equities have historically outperformed other Canadian asset classes, such as bonds.

Renaissance Investments (CIBC) – 2026 Projections predicts the average return for Canadian equities to be 6.2%, and fixed-income to be 3.8%, over the next 10 years. The bar chart below shows their rate of return predictions over the next 10 years.

Expected Rate of Return for Canadian Investments (Next 10 Years)

| Asset Class | Expected Annual Rate of Return |

|---|---|

| FTSE Canada All Corporate Bond Index | 4.5% |

| Canada FTSE Universe Index | 3.8% |

| JP Morgan GBI Global Ex-Canada Unhedged | 3.9% |

| JP Morgan GBI-EM LC Unhedged | 7.2% |

| Canada S&P/TSX Composite Index | 6.2% |

| US S&P 500 Index | 5.2% |

| MSCI All Country World Index | 5.8% |

| Gold | 6.7% |

Source: Renaissance Investments (CIBC) – 2026 Long-Term Expected Returns. All figures are in CAD.

Calculating ROI for Rental Properties

Calculating ROI on Canadian rental properties is slightly different from a regular ROI calculation. That's because you'll need to account for ongoing costs, such as rental mortgage payments, repairs, and maintenance. Your rental income might vary as well based on vacancy rates. You can follow the steps below to calculate your ROI on a rental property.

Step 1: Start by adding up all your costs associated with the property, including purchase price, closing costs, and any renovations or repairs.

Step 2: Next, calculate your expenses for the next year, such as monthly mortgage payments and ongoing costs like insurance, property taxes, and utilities.

Step 3: Subtract your total annual expenses calculated above from your annual rental income. This will give you your net rental income.

Step 4: To get your ROI, you'll then divide your net rental income by your total cost of investment.

Another way to calculate the profitability of a rental property is to calculate the cap rate. The cap rate excludes the costs of buying, selling, or financing the rental property.

Example of a Rental Property ROI Calculation with Financing

Using a mortgage loan as financing reduces your initial investment cost. That's because you don't need to use as much cash to own the property as you would if you purchased it in full with cash.

For example, let's say you buy a rental property for $500,000 with a 20% down payment of $100,000. Closing costs added up to $10,000, and you make $20,000 worth of repairs. This totals $130,000 as your initial investment cost.

You spend $1,500 per month on mortgage payments, insurance, taxes, and utilities, which adds up to $18,000 per year. You collected $2,500 per month in rent, or $30,000 per year. Your annual net rental income is $12,000 per year.

Your ROI will then be 9.2%, based on this calculation:

Example of a Rental Property ROI Calculation without Financing

If you purchase the property in full using cash, you will need to account for that as part of your initial investment cost. For example, let's say you buy a rental property for $500,000. Closing costs added up to $10,000, and you make $20,000 worth of repairs. This totals $530,000 as your initial investment cost.

You spend $500 per month on insurance, taxes, and utilities, which adds up to $6,000 per year. You collected $2,500 per month in rent, or $30,000 per year. Your annual net rental income is $24,000 per year.

Your ROI will then be 4.5%, based on this calculation:

Equity When Calculating Property ROI

If you financed your rental property purchase, you'll need to make mortgage payments. Since a portion of your mortgage payments goes towards your principal, you'll be building up your home equity with each payment. You can consider the equity that you gain when calculating your rental property's ROI.

To do this, calculate the principal paid down for the time period that you are looking for. In the previous example, let's say that of the $1,500 monthly expenses, $750 went towards the mortgage principal and rest went towards interest, insurance, taxes, and utilities. This means you are building $750 per month in equity, or $9,000 per year. This increases your rental property's ROI to 16.1%. You will receive this built-up equity back once you sell the home.

These examples do not account for capital appreciation or depreciation — the change in the property's market value over time. Property values can rise or fall depending on the market and time period, and this can significantly impact your overall rental property ROI. To factor in any change in property value, add or subtract the estimated gain or loss to your Amount Returned when using the calculator above.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.