Home Appraisals 2026

What You Should Know

- Home appraisals are conducted to find the value of a home

- Knowing the value of a home is important when you're looking to buy or sell it

- Mortgage lenders will only lend money based on the appraised value of the home

- For sellers, an appraisal can give a starting point for your listing price

- For buyers, having an appraised value lower than your purchase price will mean that the lender won’t be letting you borrow as much as you will need

- Buyers will need to make up the difference in cash, or the buyer can walk away if there was an appraisal contingency clause in the purchase agreement contract

- Home appraisals usually cost $300 to $600 and are paid by the buyer or borrower

- Home appraisals are also needed when refinancing your mortgage

What Is a Home Appraisal?

An appraisal is a process of determining the value of the home by a professional who is unbiased and impartial in their judgment. Appraisals are used in home purchase transactions & mortgage refinancing as they are useful for all parties involved in a real estate transaction from the home buyer & seller to the lender. In home purchases, an appraisal is helpful to ensure the home selling price is an accurate representation of the home’s condition, surrounding location, and neighbourhood. Whereas, in a refinance, an appraisal is essential for the lender to determine the amount of funds that can be borrowed.

In each case, the appraisal helps the lender ensure that the homeowner is not borrowing more than what the home is worth. The home acts as the collateral in the transaction, such that if the borrower were ever to default, the lender can seize and foreclose on the home or conduct a power of sale on the home. If the value of the home is less than the amount borrowed, then the lender is taking on a large amount of risk and can lose money on the transaction.

How does the appraisal process work?

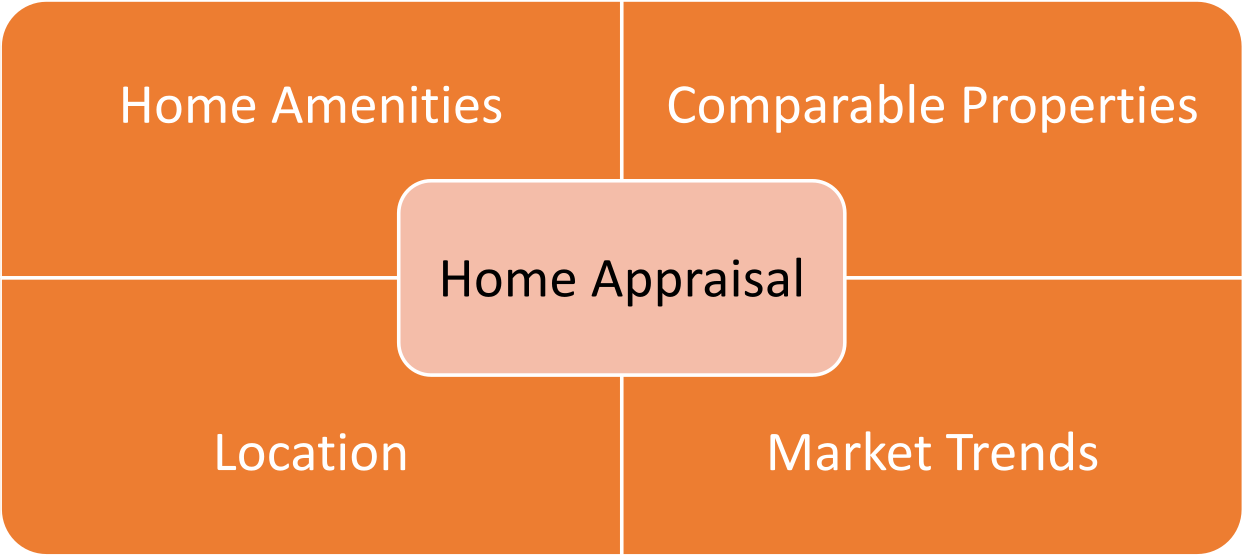

An appraisal can cost anywhere between $300 - $600 and is usually part of the closing costs of the transaction. There are several factors that can impact the value of your home:

- Home Amenities – Number of bedrooms, bathrooms, square footage, quality of fixtures, utilities, and appliances are all analysed. Apart from interiors, the exterior such as structure, construction type, parking, and gutters are also included in the appraisal.

- Comparable Properties – Similar valued properties in the area are used for comparison to determine the value of the properties in the area.

- Location – The neighbourhood, local amenities, public transit, schools, and safety standards can all play a role.

- Market Trends – The economic and social trends in the market can also affect the value of your home. For example, if it’s a buyer’s market where there are excess sellers and fewer buyers which can dampen prices, or a seller’s market, where there are excess buyers and fewer homes which can push up prices.

When does the appraisal take place in the home sale process?

The appraisal takes place right after the buyer and seller have agreed on a price and an agreement has been signed. After all the details regarding the agreement have been finalized, the lender will send an appraiser to determine the value of the home.

However, the seller can also choose to get an appraisal done before the buyers approach them in a pre-listing appraisal. In this case, the appraisal is done before all the negotiations and it removes any unpredictability of a lower appraisal after an agreement has been signed. The pre-listing appraisal home price can stay the same all the way till closing as that is the fair market value of the home. A pre-listing appraisal should be used when:

- Your home is unique or different from other homes making it very hard to find comparable homes in the surrounding area

- The real estate market is facing a lot of volatility making it very difficult to gauge buyer and seller sentiment resulting in unpredictable prices.

Types of Home Appraisals

Appraisals for Home Buyers

An appraisal is an essential part of the home buying process and will be one of the first to take place in the closing process. There are two situations that can take place, the appraised value is greater than the contract price and the transaction can take place as the buyer and lender will be satisfied with the outcome. However, if the appraised value is less than the contract price, the transaction will be delayed till the borrowing amount is sorted out which can delay the transaction.

As a buyer, if the appraised value is less than the listing or contract price, you can use it as a bargaining chip to try to reduce the price. During the negotiations, this can be a useful tool to reduce the price. However, the bank will not lend you an amount greater than the appraised value of the home. A lower appraisal can be a great tool for buyers, however, the seller may not agree to lower the price or might choose to get a second opinion.

Appraisal for Home Sellers

A home appraisal can be useful to determine the list price for sellers. However, if the appraisal is done afterward and the appraised value is less than the list price, sellers might need to reduce the price or get another appraisal. Sellers can also choose to wait for an all-cash deal where an appraisal is not required, but that is difficult and can prolong the selling process. If the location your house is located in has experienced distressed sales resulting in a greater number of homes for sale, it is likely to drive your home price down too.

In order to increase the appraised value of your home you can do some renovation. Note that renovations which relate to taste and their value is subjective are likely to increase your home price by less than their cost. While renovations which are improvements by objective measures are likely to increase the appraised value by more than their cost. You can use the greener homes initiative to subsidize your improvements while increasing the appraised value of your home.

Appraisals for Mortgage Refinancing

If you are getting your mortgage refinanced, an appraisal lower than the outstanding mortgage amount can prevent you from getting the new mortgage. The reason is that lenders use the home as collateral If the home is valued at less than the outstanding balance, the risk for the lender is too high. You may also need a home appraisal if you are receiving a reverse mortgage in Canada.

Tips to Get A Higher Appraised Value

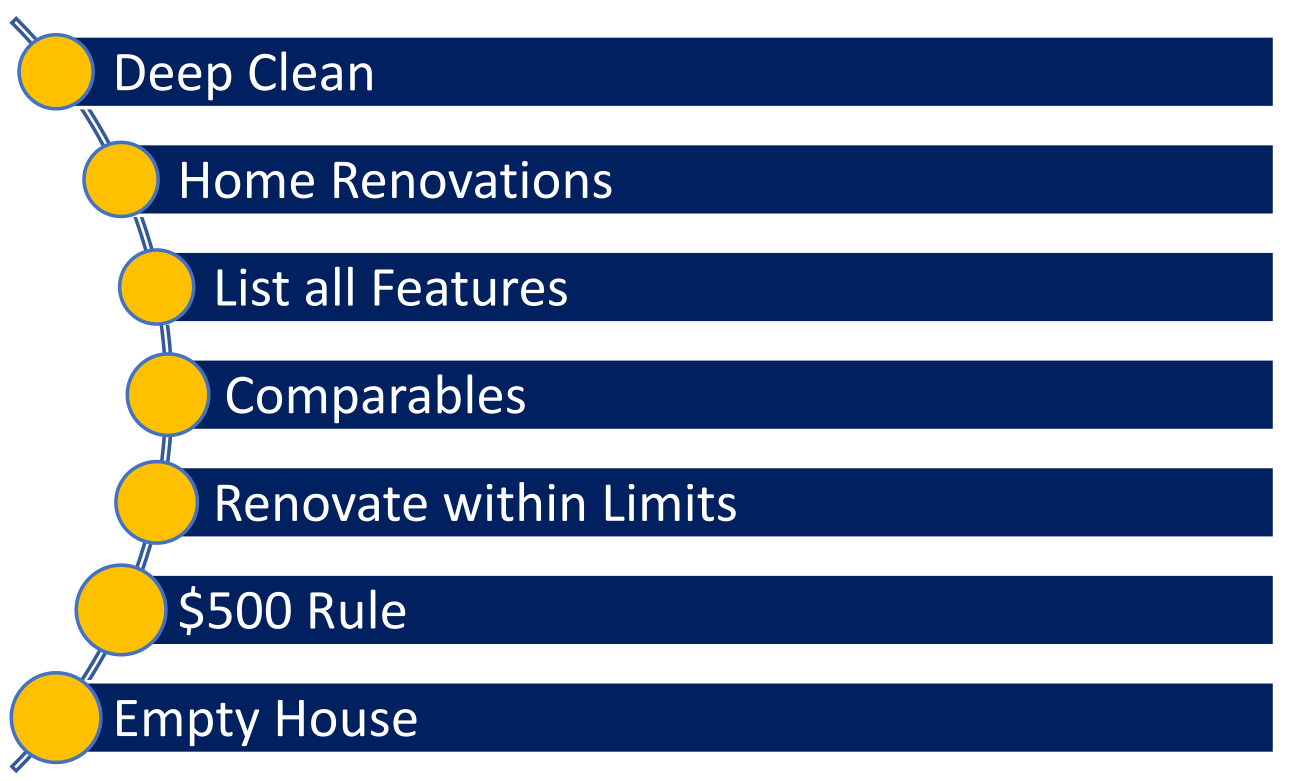

There are several ways in which you can get a higher and accurate appraisal for your home:

- Deep Clean: Although this sounds rudimentary, it needs to be mentioned. If you have carpets get them deep cleaned, marble floors should be polished, and the garage should be clean. The exterior of the home such as the front yard, porch, and back yard should all be cut and mowed. Apart from basic cleaning, if you have an additional project like a new pool getting built, you should cover it to make it look presentable.

- Home Renovations: If you have had major renovations in the past such as a new kitchen or finishing the basement, you should point those out to the appraiser. All relevant information such as when the upgrades were done, by who, and how much they cost should be provided.

- List all Features: Although the appraiser will take note of all the features in the home, you can make a list of all the amenities and surrounding benefits of your home.

- Comparables: Comparables or comps are values of surrounding homes that are used to value your home. The appraiser will get their own comparables, however, as comps are vast and can be for any homes in the surrounding area, you can track MLS listings in your neighbourhood and provide them to the appraiser.

- Renovate within Limits: If you are planning to sell the home then renovating an entire kitchen or washroom might not be worth the money or effort. However, small changes such as getting the carpets cleaned/changed, improving the lighting, or painting the walls can have a positive effect on your appraisal and do not require a lot of funds.

- $500 Rule: Appraisers often value homes in increments of $500, such that if they see a leaky faucet or cracked door, your home value could reduce by $500 even though it might only cost you $300 to fix. Therefore, any small changes or fixes that you can make should definitely be made as they can make a huge difference to the final value.

- Empty House: When the appraiser comes to value the home, make sure you don’t have a full family gathering or a get together of any sort, as this can make it very hard for the appraiser to do his or her job. If you can, you should take pets out during the appraisal process too.

Appraisal Problems and Q&A

Why would the appraised value be less than the contract price?

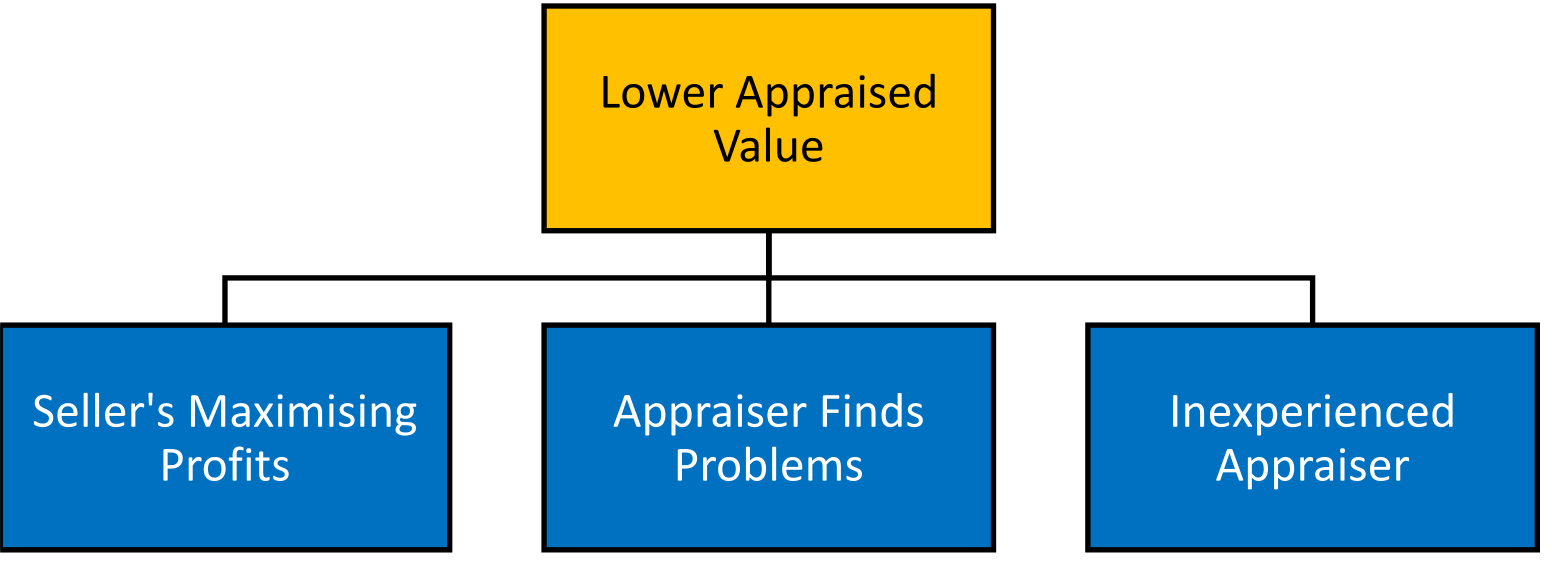

There are three reasons for the appraised value being less than the quoted price:

1. Seller Maximizing Their Profits

In most cases, the seller is trying to maximise their gain from the transaction and increases the price well beyond the fair market value in the hope that a buyer might take up the deal. In a seller’s market where there are excess buyers and fewer homes, sellers take advantage of this scarcity and drive up prices well beyond the fair market value. Seller’s also sometimes overestimate how much their house is worth and this can be problematic, hence, it is best to use an agent who can give an impartial starting price for the house.

2. Appraiser Finds Problems

An appraiser does a deep dive into the home from the exterior roof shingles to the interior piping. Homeowners might not even be aware that there is something wrong with their homes. The appraiser can also find issues that might not have occurred to the seller such as an additional room that does not have the necessary permit. This can result in a ‘cost to cure’ cost which reduces the value of the home. These factors can lead to the appraised value coming well below the contract price.

3. Inexperienced Appraiser

There can also be the rare situation where you get an inexperienced appraiser who does not have the necessary tools or comps to make an accurate judgment. If the appraiser has not dealt with similar homes or if they haven’t worked in that location for a period, then they can make mistakes too. Hence, if the appraiser comes well below the contract price, be sure to ask questions yourself, do research on comparables in the area, and worst case, get another appraiser to value the home.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.