GIC vs. Mutual Funds: Which One to Choose?

What You Should Know

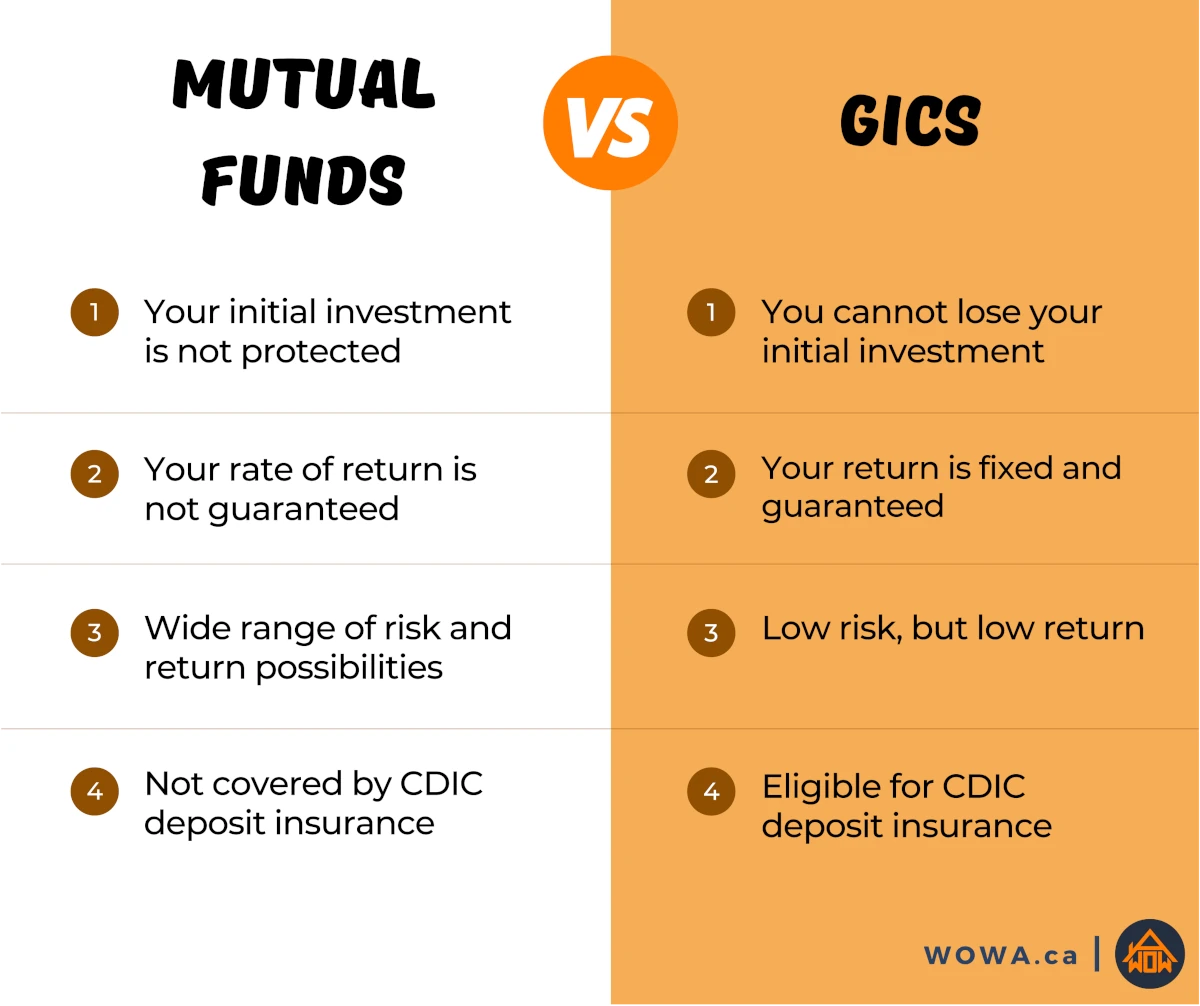

- GICs are a low-risk way to earn a guaranteed return for a set time period.

- Mutual funds offer a wide range of risk and return possibilities, but your principal and return are not guaranteed.

- The choice between GICs and mutual funds depends on your investment goals and how much risk you are willing to take.

- When comparing GICs vs. mutual funds, consider your risk tolerance, how soon you need to access the money, liquidity, and fees.

When it comes to investing and saving, Canadians have a lot of options available to them. From stocks and bonds, to mutual funds and savings accounts, and even acronyms like GICs and ETFs, it can be difficult to figure out which one is right for you. Two popular options are GICs and mutual funds, but which one should you choose?

What is a GIC?

GIC stands for Guaranteed Investment Certificate. It's a low-risk investment that provides a guaranteed and fixed GIC interest rate for a certain term length. You cannot lose your initial investment with a GIC, and your initial investment is also protected (up to $100,000 per bank) through CDIC deposit insurance.

Once your term is over, you’ll get back your initial investment plus the interest earned. Some GICs might also make monthly or annual interest payments. Your money is locked-in with a non-redeemable GIC, but it’s not locked-in with a redeemable or cashable GIC.

What is a Mutual Fund?

A mutual fund is managed by professional investors who invest the pooled money in the fund towards certain goals or assets. For example, a mutual fund might invest in a mix of stocks, bonds, or other assets. Or, it might invest exclusively in stocks, or exclusively in certain bonds. Mutual funds might even have special fund objectives, such as being a socially responsible mutual fund or being a target-date fund for retirement. The wide variety of mutual funds available mean that you can choose from low-risk funds, with lower returns, to high-risk funds with the possibility of high returns.

To invest in a mutual fund, you’ll buy into the fund by purchasing shares. You can then sell your mutual fund shares at any time, however, some mutual funds may have certain restrictions. Your initial investment is not protected with a mutual fund. This means that you could lose some (or all) of your principal. Your rate of return is also not guaranteed. This means that you might earn zero return, or even a negative return, from a mutual fund. Money that you have invested in a mutual fund is not covered by CDIC deposit insurance.

Comparing GIC vs. Mutual Fund Returns

GICs typically offer lower returns than mutual funds, but they also carry less risk. That's because over the long term, mutual funds have historically outperformed GICs. However, what if you compare GICs and mutual funds with similar risk levels: which one would perform better?

Money markets are a type of mutual fund that invests in short-term debt securities, like government bonds and commercial paper. In other words, money market funds also aim to preserve your capital, similar to what a GIC does.

For this example, we’ll take a look at historical 1-year GIC rates over the past five years and how a hypothetical investment would have performed when compared to a money market mutual fund. In these GIC vs. mutual fund comparison scenarios, we have used prevailing 1-year GIC rates compounded at each GIC rate change date. For the performance of mutual funds, they have been tracked assuming that distributions have been reinvested.

Return of GICs vs. Money Market Mutual Funds

When comparing 1-year GIC rates offered by Tangerine GICs with the historical return of the TD Canadian Money Market Fund, it’s clear that 1-year GICs have outperformed the returns from money market investments. From August 2018 to August 2023, a $10,000 investment in 1-year GICs would have resulted in a final balance of approximately $11,171. This assumes that the GIC and accrued interest are re-invested continuously. Meanwhile, the money market mutual fund would have ended at $10,639 after five years. This means the GIC had an annualized ROI of 2.24% vs. the money market mutual fund annualized ROI of 1.25%, or almost double.

GICs vs. Money Market Mutual Funds

(5-Year Performance)

| 1-Year GICs | Money Market Mutual Fund | |

|---|---|---|

| Beginning Investment | $10,000 | $10,000 |

| Ending Investment | $11,171 | $10,639 |

| Total ROI | 11.71% | 6.39% |

| Annualized ROI | 2.24% | 1.25% |

The TD High Yield Bond Fund is a bond mutual fund that invests in high yield fixed income assets, and is classified as having a low-medium risk. Over the past five years, investing in a GIC would have returned more than you would have earned from TD’s bond mutual fund. The high-yield bond mutual fund had an annualized return of 1.10% compared to the GIC’s annualized return of 2.24%. The poor performance of bonds meant that the TD high-yield bond fund had a even lower return than the TD money market mutual fund!

Return of GICs vs. High-Yield Bond Mutual Funds

GICs vs. High-Yield Bond Mutual Funds

(5-Year Performance)

| 1-Year GICs | High-Yield Bond Mutual Fund | |

|---|---|---|

| Beginning Investment | $10,000 | $10,000 |

| Ending Investment | $11,171 | $10,563 |

| Total ROI | 11.71% | 5.63% |

| Annualized ROI | 2.24% | 1.10% |

The TD Balanced Growth Fund invests 35% in bonds and 65% in equities. This mix gives it a low-to-medium risk classification. This mutual fund has significantly outperformed the returns of GICs over the past five years. If you had invested in this balanced mutual fund, you would have gotten an annualized ROI of 5.48%, well over double of the GIC’s annualized ROI of 2.24%.

Return of GICs vs. Balanced Growth Mutual Funds

Return of GICs vs. Balanced Growth Mutual Funds

(5-Year Performance)

| 1-Year GICs | Balanced Growth Mutual Fund | |

|---|---|---|

| Beginning Investment | $10,000 | $10,000 |

| Ending Investment | $11,171 | $12,508 |

| Total ROI | 11.71% | 25.08% |

| Annualized ROI | 2.24% | 4.58% |

Equities have the potential for high growth, but they are also very volatile. The TD Canadian Equity Fund has a medium risk rating, and has an annualized ROI of 6.23% over the past five years. That’s almost three times the return of a GIC for the same time period!

Return of GICs vs. Canadian Equity Mutual Funds

Return of GICs vs. Canadian Equity Mutual Funds

(5-Year Performance)

| 1-Year GICs | Canadian Equity Mutual Fund | |

|---|---|---|

| Beginning Investment | $10,000 | $10,000 |

| Ending Investment | $11,171 | $13,531 |

| Total ROI | 11.71% | 35.31% |

| Annualized ROI | 2.24% | 6.23% |

When looking at the performance of GICs vs. mutual funds over the past five years, GICs have outperformed money market funds and some bond mutual funds. However, equities continue to offer larger returns for investors willing to take on more risk. This risk can be clearly seen during the drop in the market in early 2020, where the returns of bonds and equities fell below those of GICs and money market securities.

The higher returns offered from bonds and equities do result in them catching up and surpassing GICs and money markets. While GICs offer stability and security, they may not be the best investment for those looking to grow their money over the long term.

Return of GICs vs. Mutual Funds

Summary of GICs vs. All Mutual Funds

(5-Year Performance)

| 1-Year GICs | Money Market Mutual Fund | High-Yield Bond Mutual Fund | Balanced Growth Mutual Fund | Canadian Equity Mutual Fund | |

|---|---|---|---|---|---|

| Beginning Investment | $10,000 | $10,000 | $10,000 | $10,000 | $10,000 |

| Ending Investment | $11,171 | $10,639 | $10,563 | $12,508 | $13,531 |

| Total ROI | 11.71% | 6.39% | 5.63% | 25.08% | 35.31% |

| Annualized ROI | 2.24% | 1.25% | 1.10% | 4.58% | 6.23% |

Comparing GICs and Mutual Funds

When comparing GICs vs. mutual funds, which one should you choose? The answer depends on your investment goals and how much risk you are willing to take. If you are looking for a low-risk investment with a guaranteed return, then a GIC might be right for you. But if you are willing to take on more risk in exchange for the chance of higher returns, then a mutual fund might be a better option. There are other things to consider as well, such as liquidity, time horizon, and fees. This section will take a look at each of these factors to help you decide which investment is right for you.

GICs vs. Mutual Funds: Factors to Consider

| GICs | Mutual Funds | |

|---|---|---|

| Principal is Protected | ||

| Liquidity | Varies | |

| Guaranteed Return | ||

| Higher Returns | ||

| Low Risk | Varies | |

| Low Fees |

Principal is Protected

The main feature of GICs is that your principal is protected. You cannot lose any money by investing in a GIC. Your bank or GIC provider promises that you will get back your principal plus interest at the end of your GIC term. Even if your bank fails and goes bankrupt, the federal government covers up to $100,000 in eligible GIC deposits at participating financial institutions. This means that GICs are a very low risk investment, and if your investment is covered by CDIC or other deposit insurance, then you may even consider GICs to be risk-free.

With a mutual fund, your principal is not protected. It is possible to have negative returns that cause you to lose some of your initial investment. In extreme cases, you may even lose all of the money that you have invested. This might happen if the value of the investments in the mutual fund goes to zero. While this is extremely unlikely to happen, there is still a chance of that happening. Your mutual fund provider, as well as the government, do not guarantee that your principal is protected.

How to Choose: If getting back your principal is very important to you, then you should go with a GIC. For example, this might be the case if you’re saving up for a down payment for a home, and you absolutely need the money back in a certain amount of time. With a GIC, you know exactly how much money you’ll get back, and when you’ll get it. There’s no risk of losing any of your principal investment.

If you’re willing to take on more risk, then a mutual fund can open up more investing opportunities for you. This will usually be a better choice if you don’t need the money soon and you have a longer investing time horizon. Even if you do lose some of your principal in the short-term, the possibly higher returns might mean you’ll make the money back in the future.

Liquidity

The term “liquidity” simply refers to how quickly and easily you can access your money without penalty. Mutual funds are more liquid than GICs, but that doesn’t mean that all GICs are illiquid — redeemable GICs are more liquid than non-redeemable GICs.

Most GIC rates that you’ll see advertised are for non-redeemable GICs. These are GICs where your money is locked-in for the entire term length, and you absolutely cannot withdraw your money early for any reason. In exchange for that, their offered interest rate is higher, and is commonly the advertised “rate” that people see.

Redeemable and cashable GICs are different — as the name implies, you can cash them in early if you need to, but the interest rate is lower to compensate. Redeemable GICs can be cashed-out early at any time, at a certain redemption rate, while cashable GICs can be cashed-out after 30 days and still earn their usual interest rate up to the date of withdrawal.

Mutual funds are liquid in the sense that you can sell your mutual fund shares at any time. However, mutual fund trades are executed once per day after market close, typically at 4 pm. So if you sell your mutual fund shares at 10 am, your trade will not be executed until 4 pm that same day. This means that you may have to wait a bit to get your money from a mutual fund sale, but it is still much easier than selling GICs.

Some mutual funds charge a fee if you sell your shares before a certain waiting period. For example, RBC mutual funds charge a 2% short-term trading fee if you sell within 7 days of buying them. This could eat into your initial principal if you sell your mutual fund shares within 7 days.

How to Choose: If you need liquidity, such as if you want to get in and out of investments, then a mutual fund might be a better choice. You can buy and sell mutual fund shares easily. While you might be charged a trading fee if you sell within 7 days, it’s still shorter than cashable GICs and their minimum waiting period of 30 days in order to earn interest.

If you don’t need to access the money, then a GIC allows you to lock-in your money for a set period of time. This can act as a “forced savings”, where you are less likely to spend the money if it’s not readily available. Cashable and redeemable GICs are also a more liquid alternative for those that might need to access their money before the end of their term.

Guaranteed Return

GICs have a set interest rate that is fixed for your GIC term. This is the rate you’ll earn, with interest usually being paid annually or at maturity. You can even choose to receive your interest payments monthly, or to automatically reinvest it into the GIC. This means that GICs can provide a steady cash-flow for those looking for a source of fixed income, and it gives certainty to those looking for a set return over a period of time. Even variable-rate GICs, such as market-linked GICs, have a minimum guaranteed return.

Mutual funds have no guarantees about return. The value of your investment can go up or down depending on the market, and mutual fund distributions can also vary significantly. It’s possible to have negative mutual fund returns and to never make your initial principal back. The return from a mutual fund can be very different from one year to the next, which makes them a more volatile investment.

How to Choose: If you're looking for a safe investment with a guaranteed return, GICs are a good option. But if you're willing to take on more risk in exchange for the potential for higher returns, mutual funds may be a better choice.

Higher Returns

In general, mutual funds offer the possibility to earn much higher returns than GICs. That’s because equities have historically outperformed cash and fixed-income investments over the long term. However, it’s important to remember that mutual funds also come with higher risks. Equity markets can be volatile, and there’s always the potential for loss.

You can invest in lower-risk mutual funds, such as balanced or conservative mutual funds with a larger investment mix in bonds and fixed-income, but you’ll be giving up potential returns. On the other hand, you could choose to invest in higher-risk mutual funds, such as growth or equity mutual funds with a greater focus on stocks. But again, this comes with the potential for greater losses.

GICs offer a comparatively low rate of return compared to buying stocks, ETFs, or mutual funds. However, you can still enhance your GIC yield with certain GIC products. One example are variable-rate GICs that are linked to the prime rate. If prime rates increase, often through Bank of Canada rate hikes, then your GIC interest rate will increase too.

Another example are market-linked GICs. These GICs follow the return of a certain index, for example the S&P 500 for equities, or the return of Canadian financial companies and utilities. This gives you indirect exposure to equity markets while still protecting your initial investment. In exchange for the low-risk, the maximum return of market-linked GICs are capped. You’re still guaranteed a minimum return, however, this minimum can be significantly lower than normal GIC rates for a comparable term.

How to Choose: Your investing time horizon is key when deciding based on higher returns. There is the possibility of losing money with a mutual fund, but the higher possible return over time can make up for it if you invest long enough. In other words, mutual funds have the potential to outperform GICs in the long-run even when considering the potential for losses.

Market-linked GICs can give you exposure to equity markets, but even then their returns are limited with maximum return caps. For short-term investments, the lower return of GICs might make up for their low risk.

Low Risk

GICs are a low-risk investment, and can even be risk-free if you stay within CDIC coverage limits. On the other hand, the risk of mutual funds can vary. For instance, some mutual funds might only invest in government bonds. Others might invest in money market securities, such as T-Bills, that have an even lower risk level.

One example of a low-risk mutual fund is the RBC Canadian Government Bond Index Fund (RBF563). This can have an equally low-risk comparable to GICs, but it also has an equally low return. In the case of the RBC Canadian Government Bond mutual fund, the annualized return over 23 years since inception has been 3%. There’s also still no guarantee of returns. Over the past year, the return of this fund was -3%. Meanwhile, the TD Canadian Money Market Fund has had an annualized return of 3.1% since inception 35 years ago, with a 1-year return of 4% as of August 2023.

How to Choose: If you want to invest in stocks and have the potential for capital appreciation, mutual funds may be the way to go. For more risk-averse investors that don’t mind a lower return, GICs provide a guaranteed return with almost zero risk to your principal.

Low Fees

Some investors choose investments based on fees. Others choose investments based on performance. If you’re looking for the absolute lowest fees, then a mutual fund might not be a good option.

Mutual funds are well known for having high ongoing fees, called MERs (management expense ratios). These fees are charged by the fund company to pay for the costs associated with running and managing the mutual fund. For actively managed mutual funds, it's not uncommon to see MERs of 2% or more. For example, the TD Balanced Growth Fund (TDB970) has a MER of 2.22%. That can really eat away at your returns!

On the other hand, there are usually no fees associated with purchasing or holding a GIC. This means that GICs are a way to invest without paying any fees directly. You can even use online trading platforms, such as bank brokerages, to buy GICs from a variety of Canadian financial institutions without having to pay any trading commissions. Instead, fees are usually baked into the quoted rate.

How to Choose: Between the two, GICs have no fees while mutual funds can have significant annual fees. However, you shouldn’t base your decision on fees. Instead, performance of the investment is a better factor to consider. Mutual funds can offer higher returns even when factoring in their fees. If you’re still looking for a low-fee way to invest, then ETFs are a great alternative to mutual funds. Some of the best index ETFs can have a MER as low as 0.07%.

What About Taxes?

Since GICs pay out interest, the money that you make from a GIC is considered to be interest income. In Canada, interest income is taxed as regular income, which means that GIC interest income is taxed at your highest marginal tax rate. For example, if your employment income was $80,000, then $1,000 in GIC interest income would be taxed at your $80,000-$81,000 tax bracket. You’ll face the same tax situation for other interest income, such as interest earned in a high-interest savings account or interest-paying bonds.

Earnings from mutual funds are usually in the form of capital gains and dividends. These are treated differently, with dividends benefiting from dividend tax credits and only 50% of capital gains being considered when calculating capital gains tax. In short, you’ll usually have to pay more tax on GIC interest income than you would on the same amount in mutual fund earnings.

One way to get around this is to use registered accounts, such as an RRSP, TFSA, RESP, or other retirement savings account. Registered accounts give certain tax benefits, such as deferring tax to a later year in the case of RRSPs, or having your investments grow entirely tax-free with a TFSA. Both GICs and mutual funds can be purchased and held in registered accounts. There are some restrictions to keep in mind, such as foreign currency GICs and USD GICs not being allowed in registered accounts.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.