Terms and conditions apply; rates are per annum and subject to change without notice. Eligible for CDIC deposit insurance. Non-Registered rates are tiered and based on your balance. 3.00% applies to deposits of $25,000 or more. See WealthONE website for current rates and applicable balance tiers. Highest rate in Canada for non-promotional HISA accounts, as confirmed by WOWA.ca as of June 25, 2026.

Cashable and Redeemable GICs in Canada

Best Cashable GIC Rates Canada

| Provider | Registered Redeemable | Non-Registered Redeemable | Cashable |

|---|---|---|---|

1-Year | 1-Year | 1-Year | |

WealthONE HISA Saving Account (more flexible than a GIC) | 3% | 3% | - |

0.2% | 0.2% | 2.25%** | |

WFCU | - | - | 2.10% |

2.35% | 2.35% | 1.95%* | |

- | - | 1.90% | |

- | - | 1.75% | |

2.2% | 2.2% | 1.25%** | |

- | - | 0.30% | *Available only for non-registered accounts ** The rate is for the first year of a 3-year escalating rate GIC |

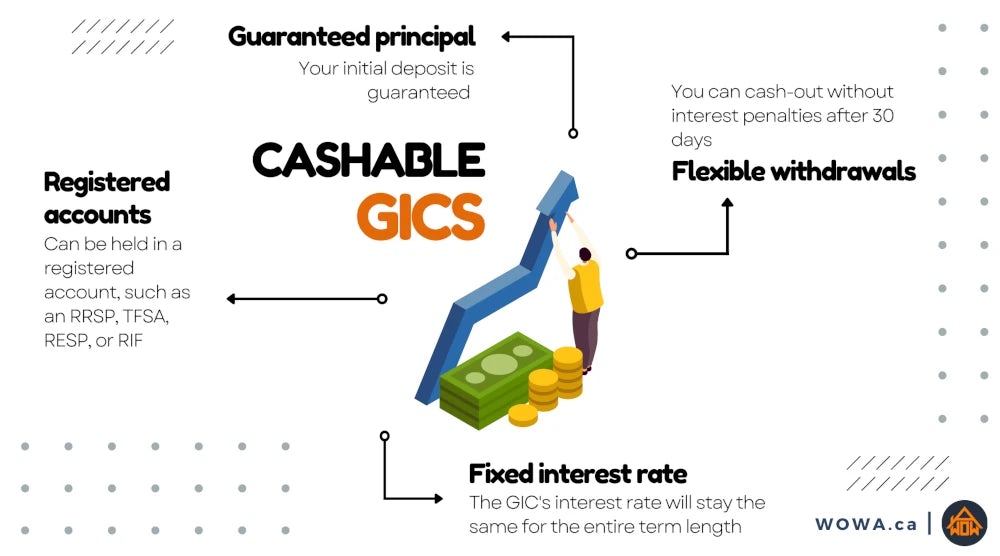

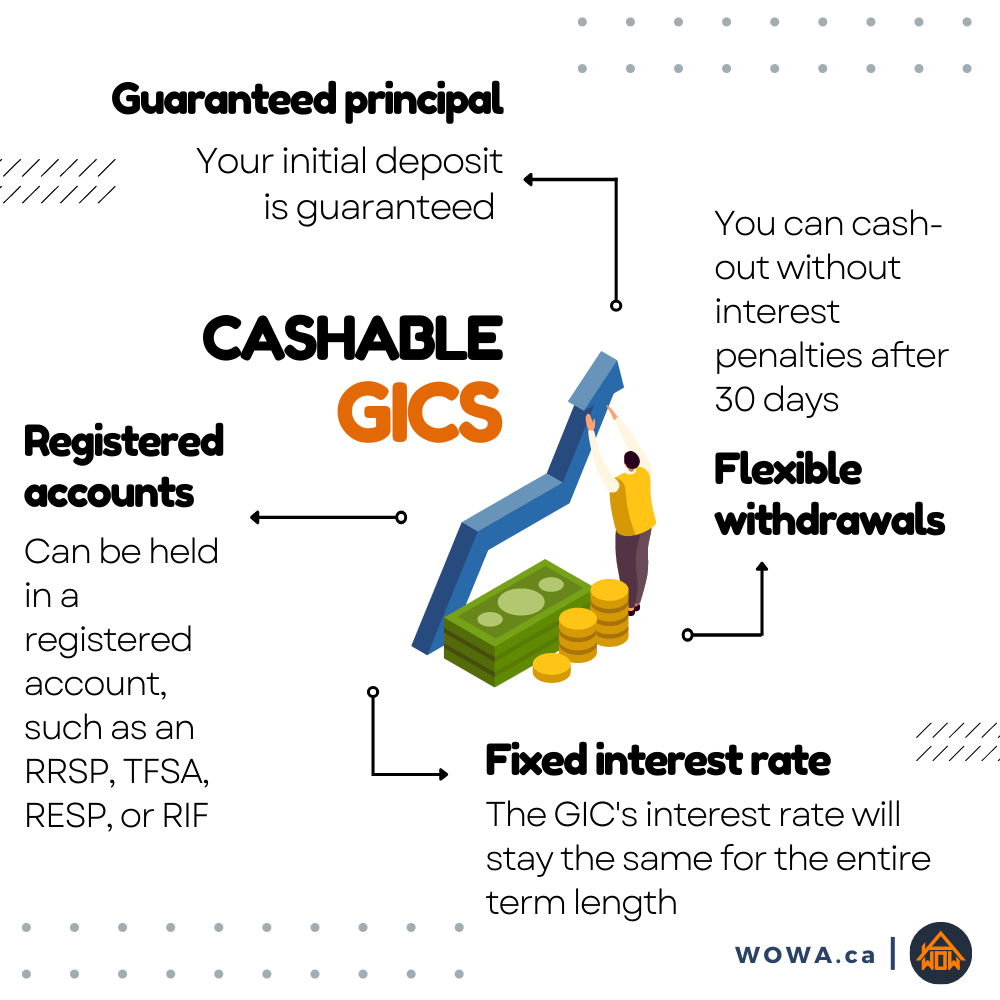

What Is a Cashable GIC?

The content below, excluding GIC rates, was last updated on: September 18th, 2023

A GIC, or Guaranteed Investment Certificate, is a type of investment that guarantees to pay you a fixed rate of interest over a set period of time. GICs are one of the safest investments available, since your principal investment is guaranteed not to decline in value and you will always know exactly how much interest you will earn.

Cashable GICs are a type of GIC that allows you to access your money before the end of the term. This means that you are not locked into your investment for a set period of time and can access your money whenever you need it. In exchange for this flexibility, cashable GICs offer lower interest rates compared to non-redeemable GICs.

However, most cashable GICs still charge an interest penalty if you cash out your GIC before 30 days. This is known as the “waiting period” or the “closed period”, and it usually results in a prior redemption rate of 0%. In other words, withdrawing from your cashable GIC before 30 days is over will mean that you will earn no interest. At some GIC providers, this lock-in period can be as long as 90 days.

How do Cashable GICs work?

If you choose to withdraw from a cashable GIC, you will keep the interest earned up until the date of withdrawal. For example, if your cashable GIC rate was 2.00% and it has been 180 days, you would receive interest for 180 days at a rate of 2.00%. If you kept the cashable GIC until maturity, you would still earn the same GIC rate of 2.00%. Withdrawing from a cashable GIC before 30 days has passed will result in 0% interest being earned.

In Canada, most cashable GICs have a term length of 1 year which can be renewed upon maturity. Interest earned on the GIC is usually paid once at maturity, though some lenders offer semi-annual or monthly interest payments. More frequent interest payments will result in a lower offered GIC rate, but allows for compound interest to accrue. Just like other types of GICs, cashable and redeemable GICs are eligible for CDIC deposit insurance at participating CDIC member institutions.

Terms and conditions apply. Rates are per annum and subject to change without notice. Eligible for CDIC deposit insurance. See WealthONE's website for current rates and applicable balance tiers. Highest rate in Canada for RRSP HISA accounts, as confirmed by WOWA as of July 24 2026

Best Cashable GICs in Canada

RBC Cashable GIC

RBC Cashable GIC

- Current Interest Rates as ofAugust 07 2026

- 1-Year Cashable GIC: 1.95%

- Minimum Investment: $1,000

- Minimum Withdrawal: $1,000

- Waiting Period: 30 Days

RBC offers two types of cashable GICs, a one-year cashable GIC and a prime-linked cashable GIC. The one-year cashable GIC has a fixed interest rate with a minimum investment of $1,000. RBC’s prime-linked cashable GIC has a variable interest rate that can change during your one-year term based on RBC's prime rate. If the prime rate increases, your GIC rate will increase too! However, the opposite will also occur if the prime rate decreases. RBC's prime-linked GIC also requires a minimum investment of $5,000.

Both of RBC's cashable GICs allow you to choose between monthly, semi-annually, or annual interest payment options. The minimum investment in order to be able to receive monthly interest payments is $5,000.

There are three ways to purchase a GIC with RBC: online using online banking, with an advisor at a branch or by phone, or with RBC Direct Investing. RBC’s online trading platform, RBC Direct Investing, also gives you access to GICs from the other major Canadian banks.

TD Cashable GIC

TD Cashable GIC

- Current Interest Rates as ofAugust 07 2026

- 1-Year Cashable GIC: 1.75%

- Minimum Investment: $1,000

- Minimum Withdrawal: $1,000

- Waiting Period: 30 Days

TD has a wide range of cashable GICs. This includes:

- TD 1-Year US Dollar Cashable GIC

- TD 5-Year Stepper GIC

- TD Short Term Cashable GIC

- TD International Student GIC

- TD 1-Year Cashable GIC

- TD 3-Year Premium Rate Cashable GIC

- TD 100-Day Special Offer GIC

The only interest payment option offered by TD for their cashable GICs is interest paid at maturity or redemption. For TD’s 100-day, 1-year, 3-year, and 5-year cashable GICs, the minimum investment is $1,000 for non-registered accounts and $500 for registered accounts. The minimum withdrawal for registered accounts is also lower, at $500.

TD's 3-year cashable GIC has a minimum waiting period of 90 days. Redemptions before then will pay no interest. TD's 5-year cashable GIC can only be withdrawn on each anniversary date. TD's short term cashable GIC has a term ranging from 1 to 29 days, with a minimum investment of $100,000. TD's international student GIC has a minimum investment of $10,000.

TD’s 1-year and 3-year cashable GICs can be purchased through TD Direct Investing. You can also purchase them through online banking, by phone, or at a TD branch.

Scotiabank Cashable GIC

Scotiabank Cashable GIC

- Current Interest Rates as ofAugust 07 2026

- 1-Year Cashable GIC: 1.90%

- Minimum Investment: $500

- Minimum Withdrawal: $500

- Waiting Period: 30 Days

The only cashable GIC offered by Scotiabank is for a one-year term. It has a lower minimum investment of just $500, and you can choose between monthly interest payments or payment at maturity. Monthly interest payments are only available for non-registered accounts, and it requires a minimum investment of $5,000. Scotiabank’s cashable GIC can be in either CAD or USD, with USD GICs now being eligible for CDIC coverage.

BMO Cashable GIC

BMO Cashable GIC

- Current Interest Rates as ofAugust 07 2026

- 1-Year Cashable GIC: 1.25%

- Minimum Investment: $500

- Minimum Withdrawal: $500

- Waiting Period: 30 Days

BMO’s GIC list includes six fully cashable and redeemable GICs:

- BMO Term Deposit Receipt

- BMO US$ Term Deposit Receipt

- BMO US$ Redeemable Short-Term Investment

- BMO Variable Rate GIC

- BMO AIR MILES GIC

- BMO Redeemable Short-Term Investment Certificate

All of BMO’s cashable GICs have a term of 364 days, except for BMO’s Term Deposit Receipt (1 day to 5 years) and BMO’s US$ Term Deposit Receipt (30 days to 5 years).

BMO’s Variable Rate GIC is linked to the BMO prime rate. It requires a minimum investment of $5,000.

The BMO AIR MILES GIC offers one AIR MILES reward mile for every $1,000 invested, rounded down to the nearest $1,000, and is paid every month. It requires a minimum investment of $5,000. For example, a $5,000 BMO AIR MILES GIC will earn you 5 AIR MILES reward miles every month. In exchange, the interest rate offered is slightly lower compared to other BMO GICs.

BMO's Term Deposit Receipt can have a term as little as 1 day, which requires a minimum investment of $100,000. Terms from 30 days to 364 days have a minimum investment of $5,000, while 1 to 5 years requires at least $1,000.

CIBC Cashable GIC

CIBC Cashable GIC

- Current Interest Rates as ofAugust 07 2026

- 1-Year Cashable GIC: 2.25%

- Minimum Investment: $1,000

- Minimum Withdrawal: $1,000

- Waiting Period: 30 Days

CIBC offers two types of cashable GIC: the CIBC Flexible GIC and the CIBC Variable Rate GIC. The Flexible GIC has a term of 1 year and a minimum investment of $1,000 for non-registered accounts and $500 for RRSPs and TFSAs. The Variable Rate GIC is linked to the prime rate, with the GIC rate changing one day after CIBC's prime rate changes.

National Bank Cashable GIC

National Bank Cashable GIC

- Current Interest Rates as ofAugust 07 2026

- 1-Year Cashable GIC: 0.30%

- Minimum Investment: $500

- Minimum Withdrawal: $500

- Waiting Period: 30 Days

National Bank’s Redeemable Without Penalty GIC has three term options: 12 months, 14 months, and 24 months. National Bank's cashable GIC can be redeemed after 30 days for their 12-month and 14-month term GICs, and can be redeemed after 6 months for their 24-month term cashable GIC.

National Bank’s Redeemable Plus GIC is also cashable, but can only be cashed without penalties on the GIC's anniversary date. This means you will need to wait at least a year to avoid penalties. National Bank's Redeemable Plus GIC has a term of 36 months.

Cashable vs. Redeemable GICs

Both cashable and redeemable GICs allow you to withdraw before the maturity date. The main difference between cashable and redeemable GICs is the interest rate that you’ll earn for your early GIC withdrawal.

Withdrawing from a redeemable GIC early will cause your GIC to only earn interest at a lower early redemption rate. If you don’t withdraw early and hold the GIC until maturity, you’ll receive a higher interest rate.

Early redemption rates can be very low at some banks. For example, RBC's redemption rate as of August 2023 is 0.75% if you cash-out your redeemable GIC after 30-59 days has passed, with it increasing up to 1.5% before 1 year has passed. If you had held the redeemable GIC for 1 year to 2 years less a day, the redemption rate is 0.05%. That's a paltry amount of interest to earn for keeping your money locked up longer for up to two years!

The benefit of redeemable GICs over cashable GICs is their higher base rate. For example, RBC’s 1-year redeemable GIC rate is 3.00% as of August 2023, while RBC’s 1-year cashable GIC rate is 2.25%. Redeemable GICs allow you the option to withdraw from your GIC, even if you give up a large portion of the interest earned, while still having the ability to earn a reasonable rate if you hold until maturity. On the other hand, cashable GICs offer the most flexibility, but a lower interest rate.

Can Non-Redeemable GICs be Withdrawn Early?

Non-redeemable GICs are locked-in until the end of your term. Your bank or GIC provider may offer exceptions, such as if you are facing financial hardship, but you may have to pay penalties. In some cases, you might not be able to withdraw from a non-redeemable GIC early at all. In exchange, non-redeemable GICs offer higher interest rates than redeemable and cashable GICs.

It is important to check the terms and conditions of your GIC before investing. For example, Scotiabank’s Terms and Conditions for their non-redeemable GICs state that they can only be redeemed early upon the death of the non-redeemable GIC owner. If there is a chance that you might need the money before the end of your GIC term, a redeemable or cashable GIC might be a better choice.

Withdrawing from a Cashable GIC

You don’t have to withdraw the full amount of a cashable GIC. Instead, you can withdraw a portion of your GIC and keep the remaining amount invested if you wish.

To make a partial withdrawal from a cashable GIC, you will usually need to still have a remaining balance that is over your bank's minimum threshold. For most cashable GICs, the remaining balance must be at least $1,000. The minimum amount that you can withdraw is also usually $1,000.

For example, let’s say that you have a $5,000 cashable GIC. If you wish to keep the cashable GIC open, then you can withdraw up to $4,000. This leaves $1,000 remaining in the GIC, which will continue to earn interest at your locked-in GIC rate. You can also choose to withdraw the entire GIC balance. Withdrawing in full will close the GIC account. You’ll receive your principal back plus accrued interest.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.