RESP Calculator

1. About the Beneficiary

2. About the Family

3. Investments and Grants

There is a surplus. You have enough saved for higher education from RESP alone!

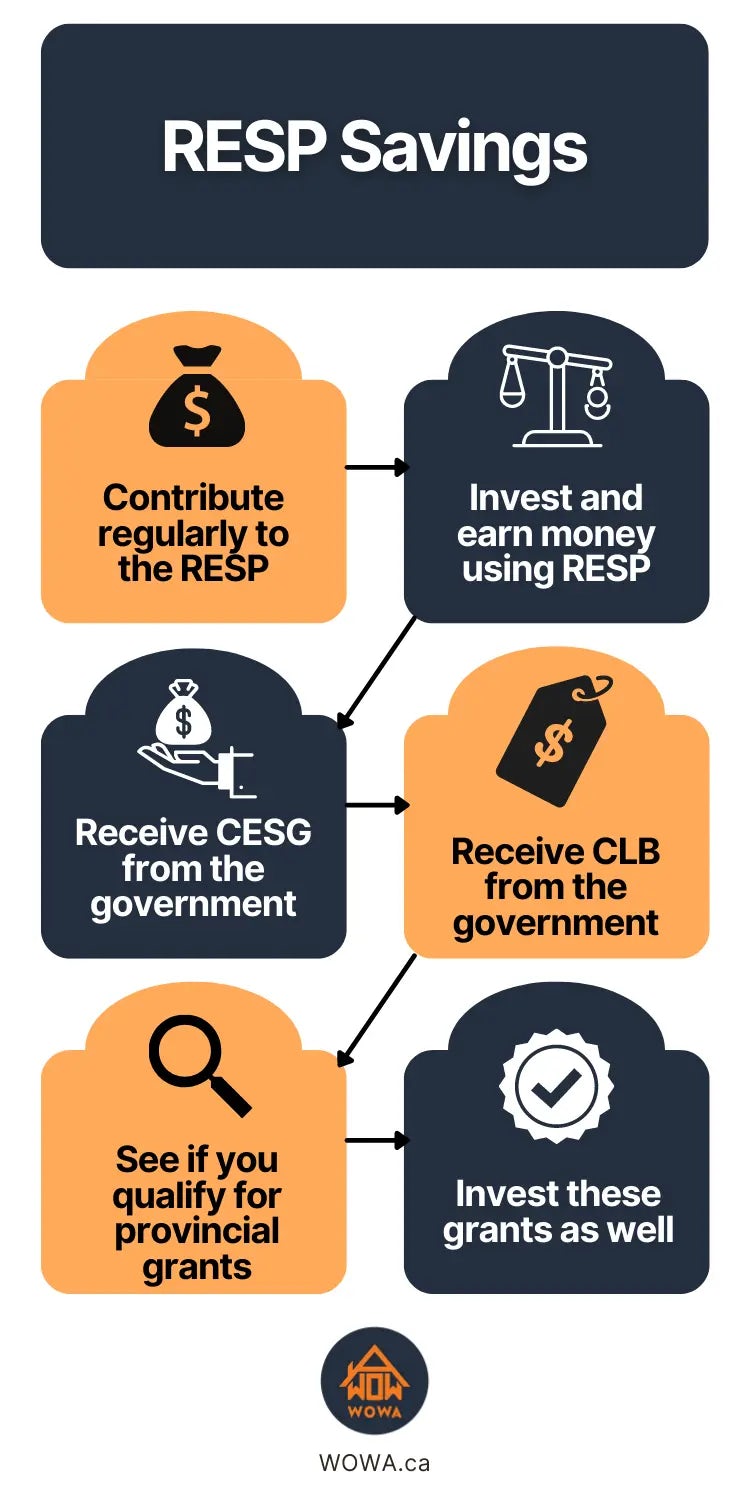

How to Calculate RESP?

A Registered Education Savings Plan (RESP) is a savings plan meant to fund a child’s educational future. By investing in an RESP account, you may qualify for a variety of national and provincial grant programs. You can visit our RESP page to learn more about how to qualify, apply for, and receive these grants. You can use our comprehensive RESP calculator given above to calculate how much you can save for your child’s education with RESP. Our comprehensive calculator accounts for the following:

- Money that you deposit into your RESP account

- The interest and investment earnings from this money

- Grants that you qualify for

- The interest and investment earnings from these grants

Annual Rate of Return

You can adjust the rate of return on your investments based on the type of assets you choose to invest in. If you choose to invest your RESP funds into a volatile asset such as stocks, this rate of return will not be consistent. Within your RESP account, you can invest in a variety of options such as mutual funds, ETFs, GICs, stocks, bonds, or any combination of the above. You should research the expected rate of return depending on your investment option and enter that number into the calculator for the most accurate calculation.

Government RESP Grants

The Canada Education Savings Grant (CESG) and Canada Learning Bond (CLB) are two grants that the Canadian government uses to incentive RESP investment. These two grants have very different qualification criteria and grant amounts.

CESG: The CESG matches 20% of the annual investment amount up to $500 per year. So, to receive the maximum amount of CESG, you will want to invest $2,500 yearly. If your family has a lower income, you can receive up to $600 per year. There is a lifetime limit of $7,200. Additionally, the CESG is only available while the beneficiary is under 18.

CLB: The CLB grants $500 in the first year that you invest in an RESP and $100 for every year afterwards that you invest in your RESP till the age of 15. The grant has a lifetime maximum amount of $2,000. This grant is only accessible to families below an income threshold, which depends on the number of children within the family. In the calculator, you only enter one net family income. If this income increases or decreases in the future, you should investigate qualify for the CLB. Additionally, the income thresholds change year to year, adjusting for inflation and other factors.

Additionally, some provinces also provide provincial grants for RESPs. Currently, there are only two provinces which offer grants - British Columbia and Quebec. You must be a resident of these two provinces to qualify for their programs. BC has the British Columbia Training and Education Savings Grant (BCTESG) and Quebec has the Québec Education Savings Incentive (QESI). The BCTESG grants $1,200 to eligible students, and the QESI matches up to 10% of annual RESP contributions depending on annual income. It has a yearly limit of $250 and a lifetime limit of $3,600.

Is the RESP Enough?

To estimate whether the RESP would be enough, you must enter all the inputs accurately. Be sure to estimate the cost of education per year carefully. This will include all living expenses for the beneficiary year to year. You must also account for inflation, which may increase costs substantially when the beneficiary attends higher education.

On a brighter note, the RESP is not the only possible funding source for the beneficiary’s education. Scholarships and government aid can drastically lower educational costs. Moreover, the RESP is a very powerful financial tool for planning for your child's future.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.