Terms and conditions apply; rates are per annum and subject to change without notice. Eligible for CDIC deposit insurance. Non-Registered rates are tiered and based on your balance. 3.00% applies to deposits of $25,000 or more. See WealthONE website for current rates and applicable balance tiers. Highest rate in Canada for non-promotional HISA accounts, as confirmed by WOWA.ca as of June 25, 2026.

U.S. Dollar GICs in Canada

Best USD GIC Rates in Canada

as of January 2025

| Provider | 1-Year | 3-Year | 5-Year |

|---|---|---|---|

Tangerine | 4.00% | 4.30% | 4.40% |

RBC | 4.10% | 3.80% | 3.80% |

TD | 4.35% | 3.65% | 3.75% |

BMO | 3.75% | 3.75% | 3.75% |

BlueShore Financial | 3.60% | 3.45% | 3.35% |

Canadian Western Bank | 3.50% | 3.15% | 3.10% |

ATB | 3.00% | 3.00% | 3.00% |

National Bank | 2.75% | 2.85% | 2.95% |

Servus Credit Union | 4.00% | - | - |

Note: GIC rates shown are for non-registered, non-redeemable GICs with annual compounding.

Note: Tangerine GIC Rates were last updated August 07 2026

*Compounded monthly

Terms and conditions apply. Rates are per annum and subject to change without notice. Eligible for CDIC deposit insurance. See WealthONE's website for current rates and applicable balance tiers. Highest rate in Canada for RRSP HISA accounts, as confirmed by WOWA as of July 24 2026

What is a USD GIC?

The content below, excluding GIC rates, was last updated on: April 23rd, 2024

USD GICs are a type of foreign currency guaranteed investment certificate (GIC) which allows you to earn a fixed rate of interest while protecting your initial investment principal. USD GICs are sometimes called U.S. Dollar Term Deposits or US Dollar Guaranteed Investments at some banks.

Unlike regular GICs that you buy from a Canadian bank or credit union which are denominated in Canadian Dollars, USD GICs are issued in U.S. Dollars. USD GICs are the most popular type of foreign currency GIC in Canada. However, some Canadian banks may also offer other currencies, such as Euros.

Long-term USD GICs, which are those with a term length of 1 year or more, are usually available as a non-redeemable GIC. This means that you can’t cash in your GIC before its maturity date. Short-term USD GICs, which have a term length of less than 1 year or less, may have the option to be redeemable or cashable. Some but not all banks offer 1-year cashable USD GICs. Cashable GICs allow you to withdraw money from your GIC investment at any time while still earning interest up until the date of withdrawal. This means you can withdraw without incurring any interest penalties.

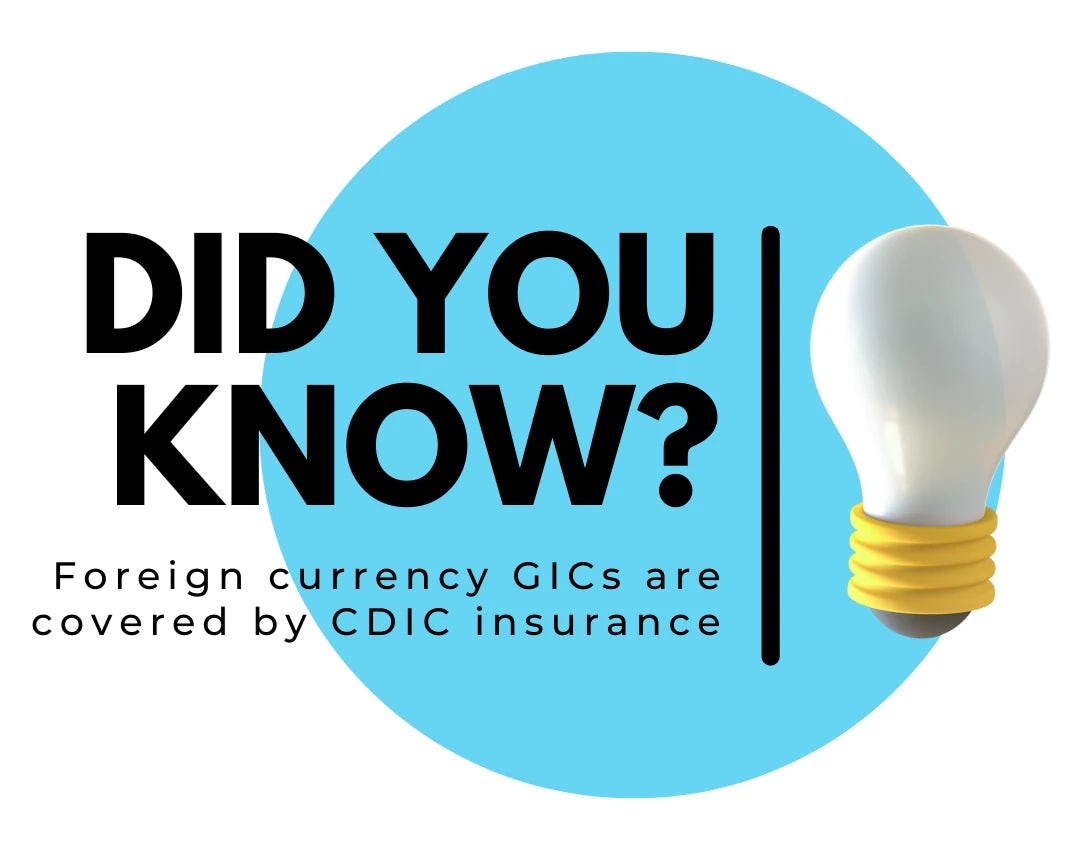

CDIC Coverage for USD GICs

Yes, USD GICs are eligible for CDIC insurance! In 2020, the Canada Deposit Insurance Corporation (CDIC) expanded its deposit insurance coverage to foreign currency deposits as well as GICs with a term longer than 5 years. This means that you can invest in USD GICs knowing that your principal is protected, even if your bank fails.

An important thing to note is that CDIC coverage is only up to $100,000 CAD per category. For example, if you had $150,000 CAD worth of foreign currency GICs at a Canadian bank, you’ll only be covered up to $100,000 CAD. If you had $100,000 CAD worth of USD GICs at a bank and $50,000 CAD of regular GICs at the same bank, then $50,000 would not be covered as it is over the category limit. Coverage is also based in Canadian Dollars, and the CDIC does not cover GICs issued by foreign banks that are not participating members. You may still receive coverage, such as FDIC deposit insurance for some U.S. banks. The foreign currency conversion rate used when calculating CDIC coverage is based on the Bank of Canada’s published exchange rates.

Can I Buy USD GICs With My RRSP or TFSA?

USD GICs in Canada are usually only for non-registered accounts. This means that you can’t buy or invest in USD GICs with your RRSP, TFSA, or other registered account. An alternative would be a U.S. Dollar investment account from a brokerage or online trading platform, where you can hold USD in cash and other securities.

How Do I Buy USD GICs?

You can purchase USD GICs from a bank online, over the phone, or at a branch. Some banks require you to become a banking client in order to be able to purchase GICs. You will need U.S. Dollars to buy USD GICs. If you have a USD bank account, you can use your funds to purchase a USD GIC directly. If you do not already have U.S. Dollars, you will need to convert your Canadian Dollars into USD . The exchange rates offered by your bank might be unfavourable. For example, Tangerine’s USD/CAD spread is approximately 3.5%.

When buying a USD GIC, you'll choose the amount of money to invest, the term length, how interest payments are treated, and what to do at maturity. For example, you can choose to have your monthly or annual interest payments made to your bank account, or have them re-invested. The same choice can be made for maturity as well. Once your USD GIC matures, you can have it paid out to your bank account, or automatically reinvest it into another selected GIC term.

Best USD GICs in Canada

1-Year USD GIC Rate 4.35% TD as of January 2025 | 3-Year USD GIC Rate 4.30% Tangerine as of January 2025 | 5-Year USD GIC Rate 4.40% Tangerine as of August 2026 |

Tangerine USD GIC

Current Tangerine USD GIC Rates as of August 2026

Tangerine GIC products are unique in having no minimum investment requirement, unlike GICs from most other providers. This means that you can purchase a Tangerine USD GIC for as little as $1. Tangerine also currently offers the best USD GIC rates in Canada as of August 2023 for a 1-year term, and tied for the best for 3-year and 5-year terms.

The conversion fee to fund your USD GIC using your Canadian Dollar Tangerine bank account is approximately 1.5%. You’ll pay this fee once when you buy your Tangerine USD GIC, built into Tangerine’s exchange rates, and once when your USD GIC matures and is converted back to CAD. As of August 22, 2023, the spread for buying and selling USD with Tangerine was approximately 3.3%.

| BUY USD | SPREAD | SELL USD |

|---|---|---|

| 1.332* | 3.3% | 1.377* |

Term options available for Tangerine's USD GICs are:

- 90 Days

- 180 Days

- 270 Days

- 1 Year

- 1.5 Years

- 2 Years

- 3 Years

- 4 Years

- 5 Years

RBC USD GIC

Current RBC USD GIC Rates as of January 2025

RBC USD GICs have a high minimum investment requirement of $5,000 USD. This applies to USD GICs with terms from 30 days to 364 days, and long-term GICs from 1 year to 5 years. For GICs of less than 30 days, the minimum investment is $100,000 USD.

TD USD GIC

Current TD USD GIC Rates as of January 2025

There are two types of U.S. Dollar investments at TD: term deposits and GICs. TD US$ term deposits require at least $5,000 USD to be invested, with terms ranging from 30 days to 369 days. At least $100,000 USD is required for terms of 1-29 days. TD term deposits can be cashed at any time, but you’ll lose the interest earned.

1-year USD cashable GICs, as well as non-cashable USD GICs from 1-year to 5 years, are also available. These GICs also have a minimum investment of $5,000 USD.

BMO USD GIC

Current BMO USD GIC Rates as of January 2025

BMO has three U.S. Dollar GIC options: the BMO US$ Fixed-Term Deposit, the BMO US$ Term Deposit Receipt, and the BMO US$ Redeemable Short-Term Investment.

Most people looking to buy a BMO USD GIC will be looking for the BMO US$ Term Deposit Receipt. This offers terms from 30 days to 5 years, with a minimum investment amount of US $1,000. The term options are:

- 30-59 Days

- 60-89 Days

- 90-119 Days

- 120-179 Days

- 180-269 Days

- 270 Days to less than 1 Year

- 1 to less than 2 Years

- 2 to less than 3 Years

- 3 to less than 4 Years

- 4 to less than 5 Years

- 5 Years

For redemptions between 30 days and 365 days, BMO's redemption rate is 1.00%. Redemptions between 366 days and 5 years have a redemption rate of 1.50%.

BMO's cashable USD GIC has a minimum investment of US $5,000 with a term of 364 days, at a rate of 3.00%. Cashable GICs do not have a lower redemption rate, unlike redeemable GICs. In exchange for that, you’re only paid interest if you withdraw from a cashable GIC after a certain waiting period, which is usually 30 days after opening.

For those looking to invest larger amounts of money, the BMO US$ Fixed-Term Deposit has a minimum investment of US $100,000 for terms also ranging from 1 day to 5 years. This type of GIC is non-redeemable.

National Bank USD GIC

Current National Bank USD GIC Rates as of January 2025

You can invest in a National Bank USD GIC with as little as $500, with both redeemable and non-redeemable options available. Term lengths include three months, six months, one year, two years, three years, four years, and five years.

ICICI Bank USD GIC

Current ICICI Bank USD GIC Rates as of January 2025

In addition to 1-5 year non-redeemable USD GICs, ICICI Bank also offers 1-5 year redeemable USD GICs and term deposits. The main difference between ICICI Bank’s redeemable USD GICs and redeemable GICs from other banks is that ICICI Bank requires at least a 6-month waiting period before you can earn interest on early withdrawals. You can still redeem your USD GIC early, but you won't earn any interest if it's within 6 months of opening.

Canadian Western Bank USD GIC

Current Canadian Western Bank USD GIC Rates as of January 2025

Canadian Western Bank (CWB) has one of the largest selections of USD GICs in Canada. This includes fixed long-term USD GICs with terms from 1-year to 10-years, short-term USD GICs from 1 day to 90 days, and floating rate redeemable USD GICs from 30 days to 1 year.

CWB’s floating rate USD GIC is based on the CWB prime rate. For USD GICs, this would be the bank's USD prime rate. If the prime rate increases, your floating rate USD GIC rate will increase too. If the prime rate decreases, your rate will decrease. However, you can always redeem and cash-out your floating rate USD GIC early.

Term options available for Canadian Western Bank’s USD GICs are:

- 1-6 Days

- 7-20 Days

- 21-29 Days

- 30 Days

- 60 Days

- 90 Days

- 1 Year

- 2 Years

- 3 Years

- 4 Years

- 5 Years

- 6 Years

- 7 Years

- 8 Years

- 9 Years

- 10 Years

Why Invest in USD GICs?

USD GICs are also a great way to diversify your investment portfolio. By investing in a foreign currency, you can protect yourself from fluctuations in the value of the Canadian dollar.

USD GICs are also a good option for those that currently have U.S. Dollars sitting around and are looking to invest them. For example, you might be waiting for a favourable USD/CAD exchange rate before converting your USD to CAD. In the meantime, you can invest your USD funds into a USD GIC to earn some interest while you wait.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.