Terms and conditions apply; rates are per annum and subject to change without notice. Eligible for CDIC deposit insurance. Non-Registered rates are tiered and based on your balance. 3.00% applies to deposits of $25,000 or more. See WealthONE website for current rates and applicable balance tiers. Highest rate in Canada for non-promotional HISA accounts, as confirmed by WOWA.ca as of June 25, 2026.

Non-Redeemable GICs in Canada

| Provider | 1-Year | 2-Year | 3-Year | 4-Year | 5-Year |

|---|---|---|---|---|---|

WealthONE | 3.55% | 3.90% | 3.90% | 3.95% | 4.10% |

Oaken Create a free account to see moreCreate a free account | 3.50% 1-Year | 3.85% 2-Year | 3.90% 3-Year | 3.95% 4-Year | 4.10% 5-Year |

MCAN Financial | 3.65% | 3.90% | 3.90% | 3.95% | 4.05% |

Achieva Financial | 3.60% | 3.65% | 3.70% | 3.75% | 4.05% |

Saven Financial Create a free account to see moreCreate a free account | 3.60% 1-Year | 3.70% 2-Year | 3.75% 3-Year | 3.80% 4-Year | 4.05% 5-Year |

3.30% | 3.55% | 3.65% | 3.75% | 4.00% | |

HomeEquity Bank Create a free account to see moreCreate a free account | 3.34% 1-Year | 3.43% 2-Year | 3.90% 3-Year | 3.85% 4-Year | 4.00% 5-Year |

MAXA Financial Create a free account to see moreCreate a free account | 3.55% 1-Year | 3.65% 2-Year | 3.75% 3-Year | 3.80% 4-Year | 3.95% 5-Year |

Outlook Financial Create a free account to see moreCreate a free account | 3.55% 1-Year | 3.65% 2-Year | 3.75% 3-Year | 3.80% 4-Year | 3.95% 5-Year |

Equitable Create a free account to see moreCreate a free account | 3.01% 1-Year | 3.65% 2-Year | 3.86% 3-Year | 3.86% 4-Year | 3.94% 5-Year |

Canadian Tire Create a free account to see moreCreate a free account | 2.35% 1-Year | 2.40% 2-Year | 2.45% 3-Year | 2.50% 4-Year | 3.93% 5-Year |

Hubert Create a free account to see moreCreate a free account | 3.55% 1-Year | 3.80% 2-Year | 3.75% 3-Year | 3.80% 4-Year | 3.90% 5-Year |

3.25% 1-Year | 3.55% 2-Year | 3.65% 3-Year | 3.75% 4-Year | 3.80% 5-Year | |

Steinbach Credit Union Create a free account to see moreCreate a free account | 3.45% 1-Year | 3.55% 2-Year | 3.60% 3-Year | 3.65% 4-Year | 3.75% 5-Year |

Laurentian Create a free account to see moreCreate a free account | 3.00% 1-Year | 3.35% 2-Year | 3.50% 3-Year | 3.65% 4-Year | 3.75% 5-Year |

Meridian Create a free account to see moreCreate a free account | 3.00% 1-Year | 3.35% 2-Year | 3.50% 3-Year | 3.60% 4-Year | 3.75% 5-Year |

LBC Digital Create a free account to see moreCreate a free account | 3.00% 1-Year | 3.35% 2-Year | 3.50% 3-Year | 3.65% 4-Year | 3.75% 5-Year |

Pathwise Credit Union | 3.70% | 3.80% | 3.60% | 3.55% | 3.70% |

ICICI Create a free account to see moreCreate a free account | 2.90% 1-Year | 3.40% 2-Year | 3.50% 3-Year | 3.60% 4-Year | 3.70% 5-Year |

DUCA Financial Create a free account to see moreCreate a free account | 3.00% 1-Year | 3.25% 2-Year | 3.40% 3-Year | 3.55% 4-Year | 3.70% 5-Year |

Manulife Create a free account to see moreCreate a free account | 3.00% 1-Year | 3.15% 2-Year | 3.30% 3-Year | 3.35% 4-Year | 3.65% 5-Year |

Simplii Financial Create a free account to see moreCreate a free account | *2.86%* 1-Year | *2.96%* 2-Year | *3.16%* 3-Year | *3.49%* 4-Year | *3.59%* 5-Year |

FirstOntario Credit Union Create a free account to see moreCreate a free account | 3.00% 1-Year | 3.20% 2-Year | 3.35% 3-Year | 3.35% 4-Year | 3.50% 5-Year |

Peoples Bank Create a free account to see moreCreate a free account | 3.25% 1-Year | 3.00% 2-Year | 3.25% 3-Year | 3.25% 4-Year | 3.45% 5-Year |

Northern Birch Credit Union Create a free account to see moreCreate a free account | 3.25% 1-Year | 3.05% 2-Year | 2.90% 3-Year | 3.05% 4-Year | 3.40% 5-Year |

Desjardins Create a free account to see moreCreate a free account | 2.80% 1-Year | 3.00% 2-Year | 3.10% 3-Year | 3.15% 4-Year | 3.35% 5-Year |

National Bank Create a free account to see moreCreate a free account | 2.75% 1-Year | 3.00% 2-Year | 3.15% 3-Year | 3.30% 4-Year | 3.35% 5-Year |

Sun Life Create a free account to see moreCreate a free account | 2.90% 1-Year | 3.00% 2-Year | 3.05% 3-Year | 3.20% 4-Year | 3.30% 5-Year |

Alterna Bank Create a free account to see moreCreate a free account | 2.65% 1-Year | 2.85% 2-Year | 3.10% 3-Year | 3.25% 4-Year | 3.30% 5-Year |

Libro Credit Union Create a free account to see moreCreate a free account | 3.05% 1-Year | 3.15% 2-Year | 3.25% 3-Year | 3.20% 4-Year | 3.20% 5-Year |

Bridgewater Bank Create a free account to see moreCreate a free account | 3.36% 1-Year | 3.50% 2-Year | 3.63% 3-Year | 3.10% 4-Year | 3.15% 5-Year |

2.70% 1-Year | 2.75% 2-Year | 2.85% 3-Year | 3.00% 4-Year | 3.10% 5-Year | |

2.70% 1-Year | 2.80% 2-Year | 2.85% 3-Year | 2.90% 4-Year | 3.10% 5-Year | |

WFCU | 2.95% | 2.95% | 2.95% | 3.05% | 3.05% |

General Bank of Canada Create a free account to see moreCreate a free account | 3.34% 1-Year | 3.44% 2-Year | 3.87% 3-Year | 3.00% 4-Year | 3.00% 5-Year |

2.45% 1-Year | 2.50% 2-Year | 2.60% 3-Year | 2.70% 4-Year | 2.75% 5-Year | |

2.45% 1-Year | 2.55% 2-Year | 2.60% 3-Year | 2.70% 4-Year | 2.75% 5-Year | |

2.45% 1-Year | 2.55% 2-Year | 2.55% 3-Year | 2.70% 4-Year | 2.75% 5-Year |

Note: GIC rates shown are for non-registered, non-redeemable GICs with annual compounding.

*Compounded monthly

What Is a Non-Redeemable GIC?

The content below, excluding GIC rates, was last updated on: September 18th, 2023

Guaranteed Investment Certificates, or GICs, are a type of investment product that provide you with a guaranteed return for a set period of time. Your initial deposit is guaranteed, and it’s also insured by the CDIC or provincial regulators for participating financial institutions.

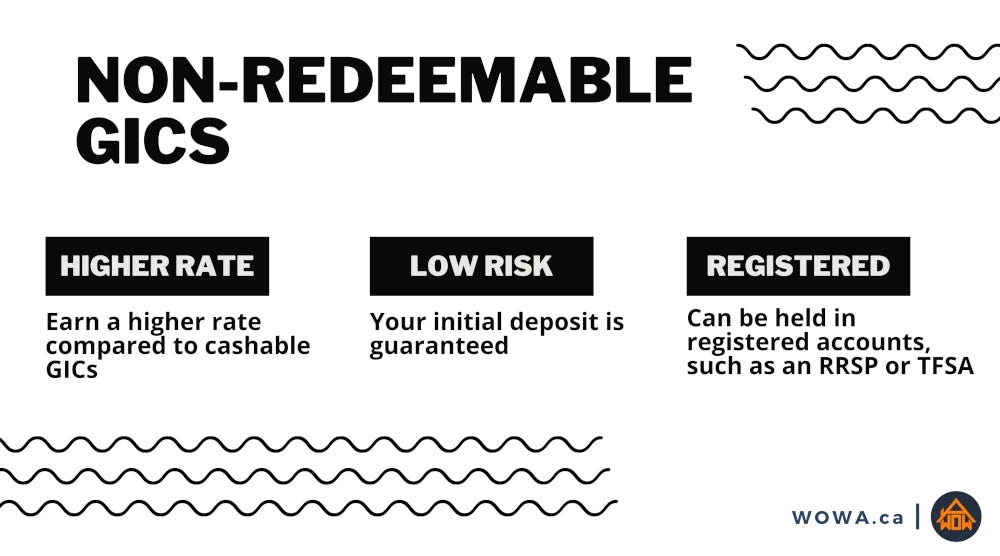

A non-redeemable GIC is a type of investment that cannot be redeemed or cashed in before the maturity date. This means that once you invest in a non-redeemable GIC, your money is locked in for the entire term. Non-redeemable GICs typically have higher interest rates than cashable or redeemable GICs, but they also come with more risk since you cannot access your money until the end of the term. For non-redeemable GICs with a fixed interest rate, you can calculate the return on a GIC in advance. This return is guaranteed and even covered by CDIC insurance, which means you’ll know exactly how much money you will get back at the end of your GIC’s term.

Just like other GIC types, non-redeemable GICs can be held in non-registered and registered accounts. This means that you can purchase non-redeemable GICs for your RRSP, TFSA, or RESP, if offered by the GIC provider.

What Does Non-Redeemable GICs Mean?

A non-redeemable GIC means that you can’t touch the money in the GIC until the GIC’s term is over. The GIC’s term is the length of time that the GIC will mature, or reach its end date. When a GIC matures, you get your original investment back plus interest that has accrued over the term. This interest is based on your GICs interest rate, which is usually compounded annually.

Non-redeemable GICs usually offer higher interest rates than other types of investments, such as savings accounts and even high interest savings accounts (HISAs), because you're agreeing to leave your money untouched for a set period of time. The opposite of a non-redeemable GIC is a redeemable GIC. There are also cashable GICs, which are an even more flexible alternative.

Non-Redeemable GICs vs Cashable and Redeemable GICs

Non-redeemable GICs are similar to term deposits, while cashable GICs are similar to savings accounts. The difference between these GIC types is the ability to make withdrawals. For example, you can withdraw from a savings account at any time. If you do withdraw from a savings account, you’ll still be paid interest and won’t need to forfeit any accrued interest. A cashable GIC works similar to a savings account, but cashable GICs usually have a minimum waiting period of 30 days. If you withdraw from a cashable GIC before 30 days, you’ll still receive your original investment back, but you won’t receive any interest.

Redeemable GICs can be withdrawn from at any time, but the difference is that you’ll be penalized by receiving a lower interest rate based on the time that you have held the GIC for before withdrawing. For example, if you redeem a 1-year redeemable GIC after only 6 months, you will still receive the interest that was paid out for those 6 months, but you’ll earn interest at a lower redemption rate. It’s often significantly lower than what you would earn if you held the GIC until maturity. Even so, redeemable GICs give you the ability to cash-out. In comparison, non-redeemable GICs cannot be cashed-out at all, barring a few exceptions.

| Non-Redeemable GICs | Cashable GICs | |

|---|---|---|

| Interest Rate | Higher | Lower |

| Term Length | Up to 10 Years | Usually 1 Year |

| Waiting Period | None | 30 Days |

| Withdrawable? | Can’t be withdrawn early | Can be withdrawn early |

| Guaranteed Principal? | Yes | No |

Can You Break a Non-Redeemable GIC?

When you purchase a non-redeemable GIC, you’ll need to sign and accept your bank’s terms and conditions for the GIC being purchased. For non-redeemable GICs, you will need to agree that the GIC cannot be redeemed before maturity. If you need to redeem the GIC before maturity, such as if you are facing financial hardship, you will need to get permission from your GIC provider to break the contract. This is not guaranteed, and your GIC provider is not obligated to allow you to break a non-redeemable GIC.

In the event that your bank or GIC provider allows you to break a non-redeemable GIC, you can expect to pay penalties for the withdrawal. This can include a portion of, or even all of, the interest accrued up until the date of redemption.

Some banks allow you to transfer or assign ownership of your GIC to someone else. If you need to access your money before the maturity date, this may be an option for you. Be sure to check with your bank or GIC provider to see if this is something that they allow. There may be restrictions or fees associated with transferring or assigning ownership of your GIC, as well as tax implications, so be sure to ask about these before making a decision.

Terms and conditions apply. Rates are per annum and subject to change without notice. Eligible for CDIC deposit insurance. See WealthONE's website for current rates and applicable balance tiers. Highest rate in Canada for RRSP HISA accounts, as confirmed by WOWA as of July 24 2026

Best Non-Redeemable GICs in Canada

RBC Non-Redeemable GIC

RBC Non-Redeemable GIC

- 1-Year Non-Redeemable GIC: 2.45%

- 3-Year Non-Redeemable GIC: 2.55%

- 5-Year Non-Redeemable GIC: 2.75%

- Minimum Investment: $1,000

- Eligible for: RRSP, TFSA, RESP, RRIF, LIF, and RDSP (min. $500)

Current RBC GIC Rates as of July 31 2026

RBC offers a wide variety of non-redeemable GICs. Available term options for RBC GICs include:

- 1 to 364 days

- 1 year

- 2 years

- 3 years

- 4 years

- 5 years

- 7 years

- 10 years

Beginning in 2020, the CDIC started insuring GICs with term lengths over 5 years. This addition also brought in CDIC insurance for foreign currency deposits, such as USD GICs. Previously, only Canadian Dollar GICs with a term of 5 years or less were eligible to be CDIC-insured.

RBC's minimum required investment is $500 for most registered accounts (RRSP/TFSA/RESP/RDSP), $1,000 for other registered accounts (RRIF/LIF/PRIF) and terms of 1-year or more, $5,000 if the term is less than 1 year or has a monthly interest payment, and $100,000 if the term is less than 30 days.

Unlike RBC's redeemable GICs, which can only be held in non-registered, RRSP, and TFSA accounts, RBC non-redeemable GICs can also be held in RESPs, RRIFs, LIFs, and RDSPs. Just like other banks, RBC GICs are also CDIC-insured.

TD Non-Redeemable GIC

TD Non-Redeemable GIC

- 1-Year Non-Redeemable GIC: 2.70%

- 3-Year Non-Redeemable GIC: 2.85%

- 5-Year Non-Redeemable GIC: 3.10%

- Minimum Investment: $1,000

- Eligible for: RRSP, TFSA, RESP, and RRIF

Current TD GIC Rates as of July 31 2026

TD has a wide range of non-redeemable GICs. This includes:

Short-Term GICs:

- 30 days

- 60 days

- 90 days

- 120 days

- 180 days

- 270 days

Long-Term GICs:

- 1 year

- 2 years

- 3 years

- 4 years

- 5 years

Special GIC rates are also offered for 14-month and 18-month terms. Non-registered and TFSA accounts require a minimum investment of $1,000, while RRSP, RRIF, and RESP accounts have a lower minimum of $500. RESP and RRIF non-redeemable GICs can also be cashable for RESP and RRIF payments.

Other non-redeemable GICs offered by TD include Market Growth GICs, which can provide a return of up to 50% for a 5-year term based on their linked index performance. With a market growth GIC, your initial investment is still protected and CDIC-insured, but it has the possibility of earning a much higher interest rate. The ones available include the TD Canadian Banking & Utilities GIC, the TD Canadian Banks GIC, and the TD U.S. Top 500 GIC. They all have a guaranteed minimum interest return, however, the maximum return is also capped.

TD Market Growth GICs

| Index | Minimum Return | Maximum Return | |

|---|---|---|---|

| TD Canadian Banking & Utilities GIC | 50% S&P/TSX Bank Index 50% S&P/TSX Capped Utilities Index | 3-Year: 6% 5-Year: 12% | 3-Year: 35% 5-Year: 50% |

| TD Canadian Banks GIC | S&P/TSX Bank Index | 3-Year: 12% 5-Year: 20% | 3-Year: 22% 5-Year: 35% |

| TD U.S. Top 500 GIC | S&P 500 | 3-Year: 7.5% 5-Year: 10% | 3-Year: 20% 5-Year: 30% |

Note: Market-linked GIC rates are current as of August 2023

Scotiabank Non-Redeemable GIC

Scotiabank Non-Redeemable GIC

- 1-Year Non-Redeemable GIC: 2.45%

- 3-Year Non-Redeemable GIC: 2.60%

- 5-Year Non-Redeemable GIC: 2.75%

- Minimum Investment: $500

- Eligible for: RRSP, RESP, TFSA, RDSP, RIF, LIF, LRIF, and RLIF

Current Scotiabank GIC Rates as of July 31 2026

Scotiabank’s wide selection of non-redeemable GICs ranges not only from the term lengths offered, but by special features as well. This includes Scotiabank Market Linked GICs and Scotiabank’s unique Guaranteed Income Optimizer (GIO) product.

Terms available for Scotiabank non-redeemable GICs are:

Short-Term GICs:

- 30 days

- 60 days

- 90 days

- 120 days

- 150 days

- 180 days

- 270 days

Long-Term GICs:

- 1 year

- 18 months

- 2 years

- 3 years

- 4 years

- 5 years

- Up to 10 years

Scotiabank has a lower minimum investment than other banks, at just $500. Terms range from 30 days to 10 years, with semi-annual or annual interest compounding. Investing at least $5,000 gives you access to monthly interest payments. U.S. Dollar GICs are also available.

Scotiabank's GIO provides guaranteed income for those that would like cash flow, such as for retirees. This gives guaranteed payments for terms ranging from 1 to 10 years. You can choose between bi-weekly, monthly, quarterly, semi-annual, and annual payments. If you still have funds in your GIO at the end of the term, you'll receive the left-over amount as a lump-sum payment as maturity.

Scotiabank Market Growth GICs have a minimum investment of $500 as well, but provide a minimum guaranteed return with the possibility for a higher rate based on a linked index. 2-year, 3-year, and 5-year terms are available, and they're also CDIC-insured and eligible for RRSP, RESP, TFSA, RRIF, and RDSP accounts.

Scotiabank Market Growth GICs

| Annual Minimum Return | Minimum Return | Maximum Return | |

|---|---|---|---|

| Scotiabank Canadian Top 60 | 3-Year: 2.44% 5-Year: 2.66% | 3-Year: 7.5% 5-Year: 14% | 3-Year: 25% 5-Year: 50% |

| Scotiabank U.S. Top 500 | 2-Year: 1.49% 3-Year: 2.44% 5-Year: 2.11% | 2-Year: 3% 3-Year: 7.5% 5-Year: 11% | 2-Year: 15% 3-Year: 20% 5-Year: 30% |

| Scotiabank Canadian Low Volatility Index | 2-Year: 1.98% 3-Year: 2.28% 5-Year: 2.47% | 2-Year: 4% 3-Year: 7% 5-Year: 13% | 2-Year: 13% 3-Year: 18% 5-Year: 35% |

| Scotiabank Canadian Utilities | 2-Year: 2.10% 3-Year: 2.12% 5-Year: 2.29% | 2-Year: 4.25% 3-Year: 6.5% 5-Year: 12% | 2-Year: 18% 3-Year: 30% 5-Year: 50% |

Note: Market-linked GIC rates are current as of August 2023

BMO Non-Redeemable GIC

BMO Non-Redeemable GIC

- 1-Year Non-Redeemable GIC: 2.70%

- 3-Year Non-Redeemable GIC: 2.85%

- 5-Year Non-Redeemable GIC: 3.10%

- Minimum Investment: $1,000

- Eligible for: RRSP, TFSA, RESP, RIF, and RDSP

Current BMO GIC Rates as of July 31 2026

BMO's non-cashable GICs include short-term, long-term, and special feature GICs. This includes the BMO Income Generator, RateRiser Max, and RateOptimizer Max.

A $1,000 minimum investment is required for all accounts, with the exception of RESPs which only require a $500 minimum investment. Non-residents, as well as business clients, can also purchase non-registered BMO GICs. BMO GICs can also be transferred.

The BMO Income Generator provides a steady stream of monthly payments for 5-years, based on your initial investment. It requires a minimum investment of $10,000.

With the BMO RateRiser Max GIC, you'll receive an interest rate that increases each year. This is available in 3-year and 5-year terms.

The BMO RateOptimizer Max GIC does GIC laddering for you, with automatic re-investments each year that blends and extends your GIC term and rate. Each year, 20% of your GIC is re-invested. This diversifies your GIC rates. This is only available in 5-year terms.

BMO offers 8 different types of market-linked GICs. This includes banks, utilities, and blue chips.

CIBC Non-Redeemable GIC

CIBC Non-Redeemable GIC

- 1-Year Non-Redeemable GIC: 2.45%

- 3-Year Non-Redeemable GIC: 2.60%

- 5-Year Non-Redeemable GIC: 2.75%

- Minimum Investment: $1,000

- Eligible for: RRSP, TFSA, RRIF, and LIF

Current CIBC GIC Rates as of July 31 2026

CIBC's short-term GICs can range from 30 days to 270 days, while long-term GICs can range from 1 year to 5 years.

CIBC’s EasyBuilder GIC uses an automatic GIC laddering strategy to split into 5 different GICs that get re-invested each year for a 5-year GIC term. This means that 20% of your investment gets re-invested annually, but you'll also have the ability to withdraw 20% each year if you wish.

CIBC’s market-linked GICs have a lower minimum investment of $500, and they follow returns based on Canadian equities, utilities, banks, and other indices.

National Bank Non-Redeemable GIC

National Bank Non-Redeemable GIC

- 1-Year Non-Redeemable GIC: 2.75%

- 3-Year Non-Redeemable GIC: 3.15%

- 5-Year Non-Redeemable GIC: 3.35%

- Minimum Investment: $500

- Eligible for: RRSP and TFSA

Current National Bank GIC Rates as of July 31 2026

National Bank offers terms of up to 5-years for their non-redeemable GICs. For short-term GICs, National Bank’s Extra GIC and Monthly Cash Management GIC provide an unique benefit in being able to be cashed-in without penalties every 90 days or 30 days. That’s due to their short term lengths. The minimum investment for these short-term GICs is just $500, which is much lower compared to other banks. For example, RBC requires a minimum investment of $5,000 for terms of less than 1 year, or $100,000 if less than 30 days.

National Bank’s Optimarket GIC is a series of market-linked GICs. These are non-redeemable GICs that have a variable interest rate based on a market index. Since your principal is guaranteed, a market downturn means that you won’t lose any money.

National Bank Market Growth GICs

| Minimum Return | Maximum Return | |

|---|---|---|

| Stability | 4-Year: 14.31% (3.4% annualized) | 4-Year: 42.31% (9.22% annualized) |

| Balanced | 4-Year: 9.91% (2.39% annualized) | 4-Year: 53.91% (11.38% annualized) |

| Performance | 4-Year: 5.50% (1.35% annualized) | 4-Year: 65.50% (13.42% annualized) |

Note: Market-linked GIC rates are current as of August 2023

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.