Self Employed Mortgage in Canada 2026Comparing Your Options

What You Should Know

- You will need to have been self-employed for at least two years for your self-employed income to be considered, and provide proof such as your income tax returns.

- Self-employed borrowers do not have to verify their income with a stated income mortgage, but stated income mortgages have higher mortgage rates and down payment requirements.

- By verifying your self-employed income, you can borrow up to 95% Loan-to-Value (LTV) with CMHC insurance, or 90% LTV without verification through private insurers Sagen or Canada Guaranty.

- Without mortgage default insurance, you can borrow up to 80% LTV with a self-employed mortgage, the same as a traditional mortgage.

Getting a Mortgage When Self-Employed

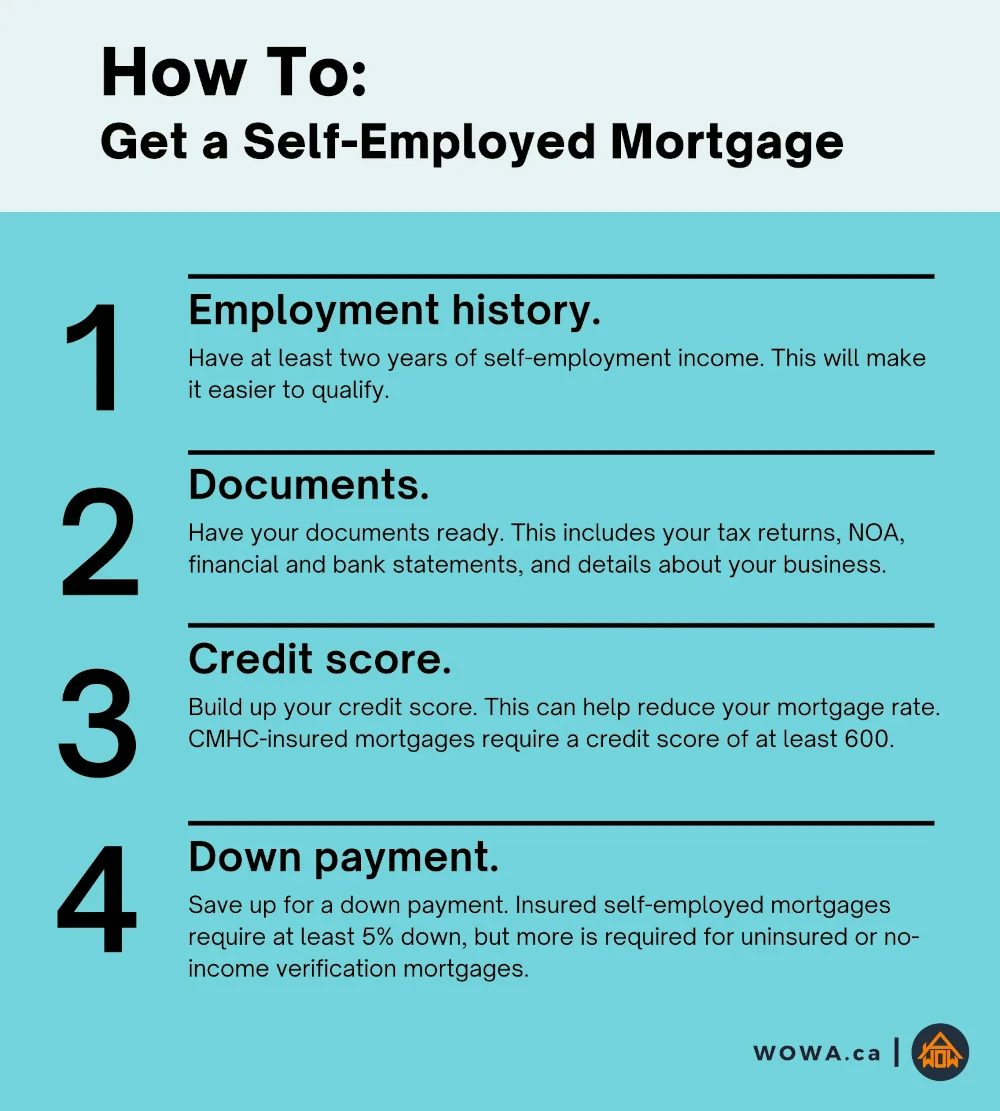

To apply for a self-employed mortgage at a bank, you need to have been operating your business or have been in the same occupation for at least 2 years. Some lenders require at least 3 years of history. There are three different ways that your income can be considered:

Types of Self-Employed Income Verification

| Income Verification | Would I Qualify? | |

|---|---|---|

| Traditional Income Confirmation | Your income, such as employment income, is verifiable through your personal tax returns. | Most self-employed business owners would not be able to confirm their “real” income traditionally. |

| Non-Traditional Income Confirmation | Your personal tax return doesn't reflect your true income, but your business's financial statements and bank statements can prove your actual income. | This is most common for those that are self-employed. |

| Stated Income | Also known as “no income verification mortgages”, you're not able to verify your income. | Anyone can state their income, however, only B Lenders and private lenders accept stated income. |

| Best Mortgage Rates for Self-Employed in | |||||

|---|---|---|---|---|---|

| Credit Scores | |||||

| 500-550 | 550-600 | 600-640 | 640-680 | 680+ | |

| 1-Year Fixed | - | - | - | - | - |

| 2-Year Fixed | - | - | - | - | - |

| 3-Year Fixed | - | - | - | - | - |

| Best Mortgage Rates for Self-Employed in | |||

|---|---|---|---|

| Credit Score | 1-Year Fixed | 2-Year Fixed | 3-Year Fixed |

| 500-550 | - | - | - |

| 550-600 | - | - | - |

| 600-640 | - | - | - |

| 640-680 | - | - | - |

| 680+ | - | - | - |

Mortgages with traditional income confirmation will have the lowest mortgage interest rates and down payment requirements. Non-traditional income confirmation will come with a slightly higher mortgage rate, down payment, and may require mortgage default insurance. Stated-income mortgages have the highest mortgage rates out of the three, with large down payment requirements and restrictions on the type of property that you can buy.

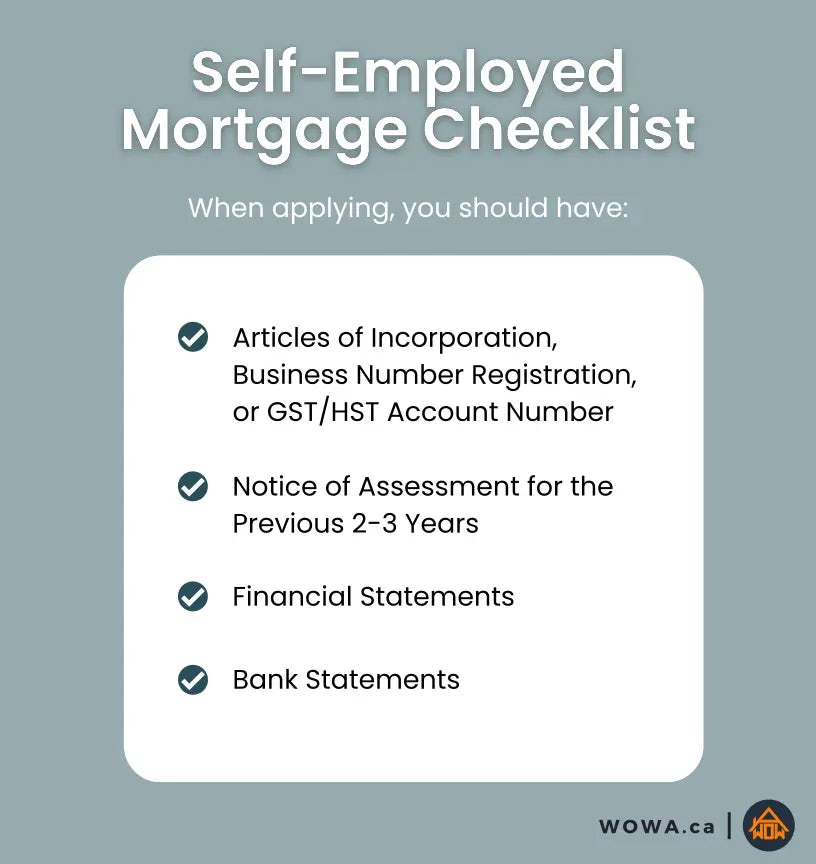

The documentation you may need to provide in your mortgage application include:

- Articles of Incorporation, Business Number Registration, or GST/HST Account Number: This is used as proof of how long you have been operating your business or have been self employed for. Only corporations will need to provide their articles of incorporation. You’ll need to have a GST/HST number if you make over $30,000 per year in gross sales or revenue.

- Notice of Assessment for the Previous 2-3 Years: You may need to provide your T1 General income tax returns or your Notice of Assessments for the previous two or three years. These documents summarize your income, including self-employment income reported as business income.

- Financial Statements: For non-traditional income verification, where you want the lender to consider your business income in addition to your personal income, your financial statements serve as proof of your business income.

- Bank Statements: You will want to provide as much proof as possible to back up your business income claims. This could include your business’s bank statements and your T2 Corporation income tax return. It could also even include expected future income from signed contracts that haven’t been completed yet.

Your Notice of Assessment is particularly important since it shows how much you may owe in unpaid taxes. Having unpaid taxes is a large red flag, as the CRA can eventually register a lien on your home or seize and sell your asset if you don’t pay.

Documentation differs depending on your bank; check with your bank for their requirements. You can also apply for a self-employed mortgage with a credit union, mortgage finance company, or a private mortgage lender. For more information about self-employed mortgage lenders and their lending conditions, visit the Self-Employed Mortgage Conditions section below.

Definition of Self-Employed

A self-employed individual is defined as someone who works for themselves through securing contracts and servicing clients. A self-employed person does not work for an employer and does not earn a fixed salary or wage from a third-party employer.

Examples of those that earn self-employment income include business owners, commission sales persons, freelancers, farmers, and fishers.

For incorporated self-employed individuals, they are considered to be self-employed if they are employed by the corporation that they themselves own and earn a salary from it. Shareholders that are not employees of the corporation and only receive a dividend are not self-employed.

What is a Self-Employed Mortgage?

Self-employed mortgages are for borrowers that rely on self-employment income or business income instead of employment income.

Being self-employed means that your income will be different from regular borrowers. A self-employed mortgage takes into account these differences, and so they will have different requirements when compared to traditional mortgages.

Being self-employed includes business owners of sole proprietorships, partnerships, and corporations. 2.65 million Canadians were self-employed in 2022, making up 13.5% of Canada’s workforce. Out of all self-employed workers in Canada, close to 44% were self incorporated, with the rest being unincorporated with paid employees or no employees. For self-employed incorporated individuals, this means that they are business owners that have incorporated their business.

Incorporating your business comes with tax benefits, but sole proprietorships and partnerships also come with distinct tax advantages. This all affects the income that self-employed workers and business owners report on their tax returns.

When mortgage lenders evaluate a traditional mortgage application, they’ll look at the net income that you declared on your tax return. For self-employed Canadians, this income amount can be artificially low due to tax deductions and expenses claimed from operating their business. With a self-employed mortgage, you’ll have more flexibility in how your income is reported. In some cases, you won’t need to verify your income with some self-employed mortgage lenders, such as First National.

Self Employed Mortgage Lenders

Traditional lenders include A Lenders and B Lenders such as banks and credit unions. A Lenders include the largest banks in Canada, such as RBC, CIBC, BMO, TD, Scotiabank, and National Bank. Examples of B Lenders include Equitable Bank and Home Capital, as well as mortgage finance companies such as MCAP and MERIX Financial. Some B Lenders and private lenders offer Stated Income Mortgages to self-employed individuals.

A Lenders

The A lenders include the six largest banks in Canada. The A lenders generally have the most stringent lending criteria, which requires you to pass a mortgage stress test, and show you have a good credit history and a stable income.

What is a Credit Score?

A credit score is a numerical value assigned to each individual based on their history of repayments. It helps creditors predict how likely you are to repay your debts in the future. The credit scores range from 300-900 and a credit score above 660 is generally considered good, while a credit score above 725 is considered very good.

Several banks have specific mortgage products for self-employed individuals, and these include National Bank Mortgage for the Self-Employed, RBC Self Employed Mortgage, and Scotia Mortgage for Self Employed. While CIBC doesn’t make their CIBC Self-Employed Recognition Mortgage well-known, it is featured on their mortgage selector. CIBC’s Self-Employed Recognition Mortgage doesn't require any income verification if you have more than 35% equity or down payment.

Meanwhile, BMO and TD do not have a specific mortgage application for self-employed individuals but will consider all mortgage applications regardless of your employment type.

A-lenders offer fixed and variable rate mortgages. Documentation that is required includes your Notice of Assessment for 2-3 years prior to your application, financial statements, and articles of incorporation if you are incorporated.

Different banks have different minimum down payment and maximum loan requirements. The mortgage down payment is what you are required to pay upfront to obtain a mortgage and you can check your required mortgage down payment ahead of time. The Home Buyers’ Plan may also allow you to withdraw up to $60,000 from your RRSP if you are a first-time home buyer.

Self-Employed Mortgage Conditions/Requirements for the Big Banks

| Mortgage Loan Amount | Minimum Down Payment | Documentation and Other Requirements | |

|---|---|---|---|

| National Bank | Maximum of $600,000 | 10% |

|

RBC |

| 20% with no default insurance or 5% with default insurance |

|

| Scotiabank |

| 10% (Must have default insurance if loan to value ratio exceeds 65%) | N/A |

BMO | Up to 80% LTV with no default insurance or up to 95% LTV with default insurance | 20% with no default insurance or 5% with default insurance | N/A |

CIBC | A minimum of $10,000, up to 65% LTV | 35% |

|

TD | Up to 80% with no default insurance or up to 95% with default insurance | 20% with no default insurance or 5% with default insurance |

|

The Gross Debt Service ratio is the percentage of your monthly income required to pay your monthly housing costs while the Total Debt Service ratio is the percentage of your monthly income required to pay all your monthly living expenses (including housing and non-housing expenses).

B Lenders:

In 2023, approximately 80% of mortgages for new home purchases were approved by A Lenders, which includes chartered banks and credit unions. Self-employed mortgage applicants may have an unstable income or a less than sufficient credit rating to qualify for a mortgage with an A lender. In this case, you may be looking towards obtaining a loan from a B Lender. B Lenders include creditors such as Equitable Bank, Home Capital, MCAP, Merix Financial, and Street Capital Financial Corporation.

B Lenders typically have less stringent requirements than A Lenders because banks and credit unions are subject to more regulation. The regulated mortgage market in Canada is overseen by the Office of the Superintendent of Financial Institutions (OSFI). As a simple comparison, MCAP has a Gross Debt Service ratio of 39% (compared to 32% at Scotiabank) and a Total Debt Service ratio of 44% (compared to 40% at Scotiabank). The higher the ratio, the less income you are required to have compared to your housing costs and living expenses, and this makes it easier to qualify for a mortgage.

To apply for a mortgage with a B Lender, you are typically required to go through a mortgage broker. A mortgage broker is a professional who is specialized in finding mortgages based on your unique financial situation. Your mortgage broker will let you know what documentation you are required to provide.

As B Lenders typically lend out riskier mortgages, the rates are also generally higher than those offered at A Lenders. However, if your mortgage is insured by mortgage default insurance, you may be able to secure a lower rate as the insurance renders your mortgage riskless to the lender.

Private Lenders:

Private lenders should be used as a mortgage lender of last resort as their interest rates are generally very high -- around 7-18%. Also, private mortgage fees including broker fees and fees for setting up the loan can amount to 1-3% of your property value. As private lenders are part of the unregulated mortgage market, their approval process is much easier and less stringent than those of the abovementioned lenders. Private lenders will consider the value of your property as well as your creditworthiness. Private lenders offering a Stated Income Mortgage will use your gross income to calculate the amount of mortgage you qualify for. Private lenders include individual lenders and syndicate (group) investors.

How Self-Employed Mortgages Work

B Lenders, Private Mortgage Lenders, or Traditional Lenders?

There are unique challenges in obtaining a self-employed mortgage from a traditional lender such as a bank or credit union. Traditional lenders use your net income from line 150 of your T1 tax return from the past 2 or 3 years to determine the mortgage you qualify for while many private lenders offering a Stated Income Mortgage will use your gross income. Your net income is calculated as your gross income less any business expenses that you may have deducted. For instance, you may have deducted business expenses such as legal expenses, business travel, business meals, or office supplies expenses from your gross income to get to your net income.

Having a lower net income allows you to save on income tax, but the disadvantage of having a low net income is that it may be harder for you to qualify for a self-employed mortgage from a traditional lender. For information about self-employment taxes, visit our income tax calculator.

Let’s say in 2023 you earned $100,000 in gross income and your business expenses totalled $45,000. In 2022 you earned $90,000 in gross income and your business expenses totalled $40,000. Therefore, your net income would be $55,000 and $50,000 respectively.

A traditional lender will use your average net income of $52,500 while a B Lenders or private lender with a stated income mortgage will use your average gross income of $95,000. Using the higher gross income can help you qualify for a self-employed mortgage more easily, but B Lender and private lenders generally offer higher rates than traditional lenders, meaning that you are likely to pay more for your mortgage. However, some select B Lenders and private lenders specialize in stated income mortgages who offer discounted rates for self-employed mortgages.

Stated Income Mortgages

With a stated-income mortgage, your lender will not verify your income. They won’t look at your tax returns, financial statements, or bank statements. For example, commission salespersons might have trouble verifying their income if their commissions are spotty and not stable. Instead, you will “declare” or “state” your income. Your stated income must be reasonable, and will be compared to your industry and business.

This leads to the possibility of fraud as borrowers overstate their income in order to get a mortgage larger than they could qualify for. The Federal Reserve Bank of Philadelphia even goes as far as describing stated-income mortgages as “liar-loans”, with overstated incomes leading to mortgage defaults during the 2007-2008 housing crisis.

Stated income mortgages require a large down payment or it will need to be insured. If you don’t want to pay for mortgage default insurance premiums, you will most likely need to make a down payment of 35% or more. Stated income mortgages are also only offered by B Lenders and private mortgage companies. You generally won’t be able to get a stated income mortgage from a bank, such as RBC or TD, without income verification.

For insured stated income mortgages, you’ll need to pay insurance premiums. You can make a down payment as low as 10% for insured stated income mortgages. You will need to have a good credit score in order to get a stated income mortgage. If you have bad credit, you’ll need to prove your income.

The CMHC does not insure stated income mortgages. Instead, you will need to go with a private mortgage default insurer, such as Sagen or Canada Guaranty.

How do I state my income?

For self declared income, you'll need to complete a declaration form or letter. You may need a witness when signing the form. The following information will be asked:

- Gross earnings or net income of the previous year

- Name and address of the business

- Nature of business

- Years in business

- Number of employees

- Percentage of business ownership

- Retained earnings for corporations

Are Stated Income Mortgages Illegal?

Stated income mortgages are not illegal in Canada. Stated income mortgages became illegal in the United States after the Frank-Dodd Act in 2010 required borrowers to prove their income for owner-occupied properties.

The Eligible Mortgage Loan Regulations under Canada's Protection of Residential Mortgage or Hypothecary Insurance Act states that mortgage lenders must verify the borrower’s income and employment status if they are employed. For self-employed borrowers, lenders just need to judge if the income reported by the self-employed borrower is “plausible”.

In other words, the stated income that a self-employed borrower declares must be reasonable. To do this, lenders will look at the industry, how long you have been in business for, and your occupation. For example, freelance photographers make roughly $40,000 per year in Canada. If a self-employed freelance photographer in their first year of business declares a stated income of $400,000 per year, their self-employed mortgage application will most likely not be approved. Their income will need to be verified in this case.

Insured Stated Income Mortgages

CMHC Self Employed Mortgage Insurance

The Canadian Mortgage and Housing Corporation (CMHC) provides insurance to self-employed mortgage lenders should the borrower default on their mortgage. In Canada, the OSFI requires you to purchase mortgage default insurance if your down payment is below 20%, however, some banks might require you to have insurance for down payments up to 35%. The higher your down payment, the lower your insurance costs.

CMHC’s Self Employed program provides mortgage loan insurance for self-employed borrowers. CMHC self-employed borrowers who can verify their income are treated the same as borrowers of traditional mortgages, with the same mortgage insurance premiums and the same qualification criteria as employed workers. These CMHC requirements are:

- Maximum LTV/Minimum Down Payment: You can borrow up to a 95% loan-to-value (LTV) or make a down payment as low as 5% for the first $500,000, and 10% for the remainder.

- Maximum Loan Amount: The price or value of the property must be less than $1 million.

- Minimum Credit Score: The minimum credit score is 600.

- Maximum Debt Service Ratios: The maximum Gross Debt Service Ratio (GDS) is 39% and the maximum Total Debt Service Ratio (TDS) is 44%.

- Maximum Amortization Period: 25 years

CMHC self-employed mortgages can be owner-occupied properties with up to four units, or non-owner occupied for rental properties up to four units. For rental properties that are not owner-occupied, the minimum down payment is 20%.

The biggest difference between CMHC self-employed mortgage insurance and private mortgage insurance is that the CMHC requires you to verify your income. Stated income mortgages cannot be insured by the CMHC. Private insurers Canada Guaranty and Sagen allow stated income mortgages.

You will need to have been in business for at least 24 months (2 years). To verify this, the CMHC will look at your income tax returns, Notice of Assessment, credit reports, GST returns, financial statements, articles of incorporation, or business license.

To verify your income, the CMHC will look at your Notice of Assessment and T1 General tax return, or your T2125 Statement of Business or Professional Activities. T2125 includes your business income and professional income, including professional fees and work-in-progress (WIP).

Recently Self-Employed

If you're recently self-employed and do not have 24 months of operating history, you can still qualify for a CMHC self-employed mortgage if you have enough cash reserves, you're acquiring an established business, or you have a good credit history with training or education.

To verify recently self-employed income, the CMHC can look at any signed contracts for future work, your previous employment income, and your bank statements.

Gross Up

The CMHC allows sole proprietorships and partnerships to increase their self-employment income by 15%. This “gross up” or “add back” is to compensate for deductions that might have been made, such as capital cost allowances or expenses.

CMHC Self-Employed Mortgage Premium Rate

| Loan-to-Value (LTV) | Premium Rate |

|---|---|

| Up to 65% | 0.60% |

| 65.01% - 75% | 1.70% |

| 75.01% - 80% | 2.40% |

| 80.01% - 85% | 2.80% |

| 85.01% - 90% | 3.10% |

| 90.01% - 95% | 4.00% |

Source: CMHC Mortgage Premiums

To calculate how much you will be paying in mortgage default insurance, use the CMHC Mortgage Insurance Calculator. The CMHC self-employed policy covers different business organizations forms including proprietorships, partnerships, and incorporated companies.

Sagen - Business for Self (Alt. A)

Formally called Genworth Canada, Sagen’s Business for Self (Alt. A) program allows self-employed borrowers to get a mortgage without verifying their income. Self-employed commission salespersons do not qualify for Sagen’s Business for Self mortgage. You also cannot qualify if you have had a previous bankruptcy.

- Maximum LTV/Minimum Down Payment: You can borrow up to a 90% loan-to-value (LTV), or make a down payment as low as 10%.

- Maximum Loan Amount: In Toronto, Vancouver, and Calgary, you can borrow up to $750,000. In the rest of Canada, you can borrow up to $600,000.

- Minimum Credit Score: The minimum credit score required is 650 if you make a down payment greater than 20%. Otherwise, the minimum credit score is 680.

- Maximum Debt Service Ratios: The maximum GDS is 39% and the maximum TDS is 44%.

- Maximum Amortization Period: 25 years

Sagen's Business for Self mortgage is only available for owner occupied properties. You can have owner-occupied rental properties up to two units, with one unit being owner-occupied. You can not use it for other rental properties, second homes, and vacation homes.

While you don't need to verify your income, you still need to verify the history and operation of your business and that it has been operating for at least two years. You'll need to provide a recent Notice of Assessment that shows that you have no tax arrears.

For sole proprietorships and partnerships, you will also need to provide a T1 General tax return for the past two years or audited financial statements or a business license or your GST/HST return summary.

For corporations, you must provide either your audited financial statements for the previous two years or your articles of incorporation.

Sagen’s self-employed mortgage premiums are significantly higher than CMHC insurance premiums for traditional mortgages. With a premium rate of 5.85% for a down payment of less than 15%, a $500,000 mortgage will cost $29,250.

Sagen (Genworth) Self-Employed Mortgage Premium Rate

| Loan-to-Value (LTV) | Premium Rate |

|---|---|

| Up to 65% | 1.50% |

| 65.01% - 75% | 2.60% |

| 75.01% - 80% | 3.30% |

| 80.01% - 85% | 3.75% |

| 85.01% - 90% | 5.85% |

Source: Sagen Business for Self

Canada Guaranty - Low Doc Advantage

Canada Guaranty’s Low Doc Advantage is for self-employed borrowers with limited income documentation.

- Maximum LTV/Minimum Down Payment: You can borrow up to a 90% loan-to-value (LTV), or make a down payment as low as 10%.

- Maximum Loan Amount: In Toronto, Vancouver, and Calgary, you can borrow up to $750,000. In the rest of Canada, you can borrow up to $600,000. The maximum property value is $1,000,000.

- Minimum Credit Score: You will need to have a strong credit score and credit history.

- Maximum Debt Service Ratios: The maximum GDS is 39% and the maximum TDS is 44%.

- Maximum Amortization Period: 25 years

Canada Guaranty's qualifications are similar to Sagen. You must have been self-employed for at least two years, you cannot be on commission sales income, you haven't defaulted on a mortgage or undergone bankruptcy in the past 5 years, and the property must be owner-occupied with up to two units.

You also cannot borrow your down payment. At least 5% down payment must be from your own resources, while the rest can be gifted.

Unlike Sagen, you do not need to provide documents such as audited financial statements or business licenses. However, your stated income must be reasonable. This is done by looking at your Notice of Assessment (NOA), your type of business, the ownership structure, and your percentage of ownership of the business

Canada Guaranty’s self-employed mortgage premiums are the same as Sagen’s premiums.

Canada Guaranty Self-Employed Mortgage Premium Rate

| Loan-to-Value (LTV) | Premium Rate |

|---|---|

| Up to 65% | 1.50% |

| 65.01% - 75% | 2.60% |

| 75.01% - 80% | 3.30% |

| 80.01% - 85% | 3.75% |

| 85.01% - 90% | 5.85% |

Source: Canada Guaranty Low Doc Advantage

FAQ About Self-Employed Mortgages

How much can I borrow for a mortgage if I'm self-employed?

With mortgage default insurance, you can borrow up to 95% of the value of the home. Without insurance, you can only borrow up to 80% of the value of the home. The same debt service ratio limits apply to self-employed mortgages, which for CMHC insurance would be 39% GDS (Gross Debt Service) and 44% TDS (Total Debt Service). This leads to the affordability of your mortgage, which depends on your self-employment income, other income, and your regular expenses. To calculate how much you can afford as a self-employed borrower, use our mortgage affordability calculator.

How many years do you have to be self-employed to get a mortgage?

Although lenders prefer to see at least two years of self-employment income, you can still get a mortgage if you’ve been recently self-employed. However, mortgages for recently self-employed borrowers are harder to qualify for and will require additional documentation.

Can I get a self-employed mortgage without proof of income?

Yes, you can get a self-employed mortgage without proof of income. The only mortgage default insurers that allow borrowers to get a self-employed mortgage without proof of income are Sagen and Canada Guaranty, which would be for a stated income mortgage. You’ll need to make a down payment of at least 10% and borrow with a lender that works with one of these insurers. CMHC-insured mortgages require self-employed borrowers to show proof of income.

Are mortgage rates higher for self-employed borrowers?

Self-employed mortgage rates can be higher than normal mortgages, but there is no fixed rule that self-employed rates must be higher. If you have mortgage default insurance on your self employed mortgage, your mortgage rate can be as low as any other insured mortgage.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.