Desjardins Mortgage Rates & Reviews

Desjardins Bank Background

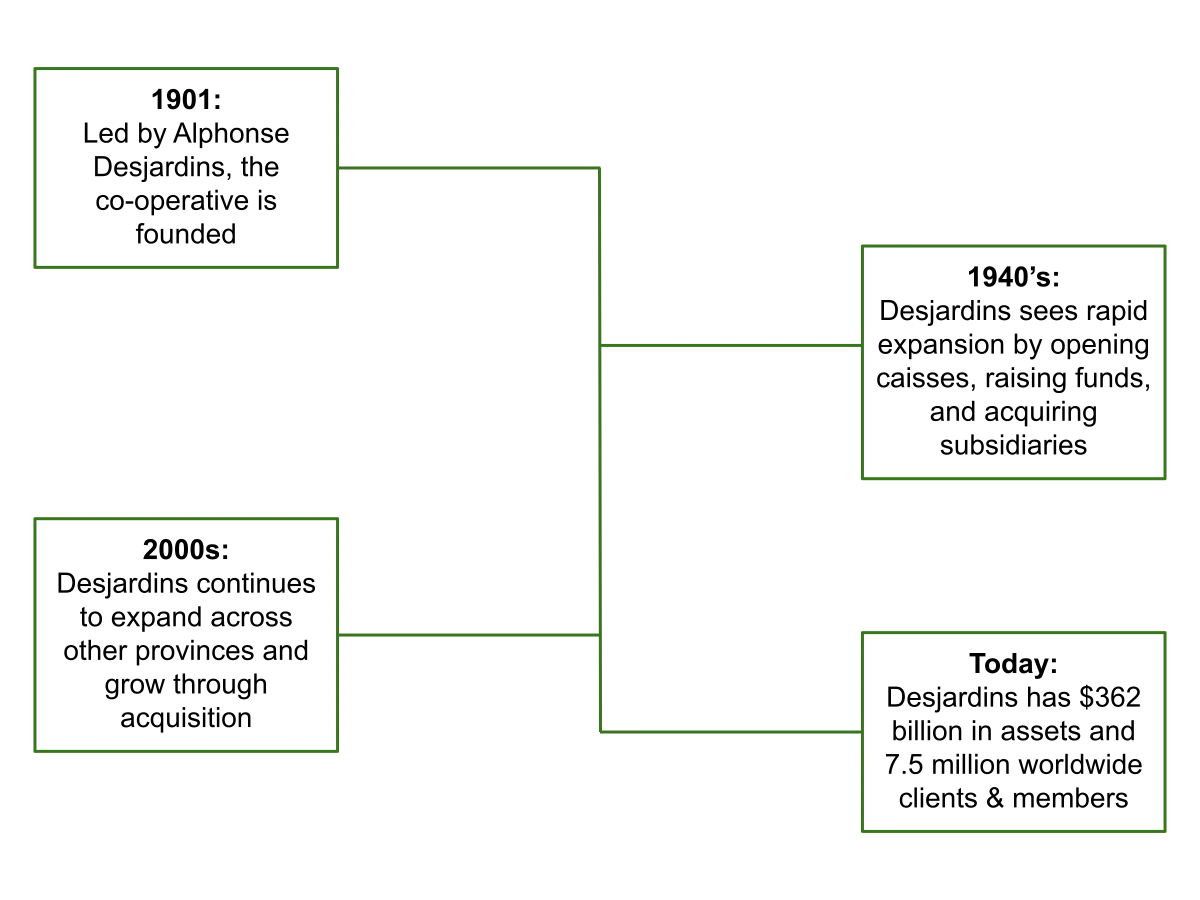

Desjardins Group is the largest financial cooperative in North America, with over 200 local branches and 660 service centers. Desjardins is a federation of caisse populaires that was founded in 1900 by Alphonse and Dorimène Desjardins. Similar to credit unions, caisse populaires are savings and credit co-operatives, with the difference being that Caisse Populaires primarily cater to residents of Quebec and other francophone communities. Desjardins currently has over 7.7 million members, most of whom are located in Quebec and Ontario. Desjardins was originally founded in Levis, Quebec, where its legal headquarters are still located. The group now has offices across Quebec and worldwide. In addition to retail banking, the Desjardins Group also offers several other financial products through their 20 subsidiaries, such as insurance, capital market services, wealth management, and venture capital funds. Desjardins is also active in 30+ developing countries, offering technical assistance programs and long-term investments.

Desjardins Bank Fixed Mortgage Rates

Desjardins fixed rate mortgage is more popular than a variable rate mortgage because of the peace of mind it offers. With a fixed-rate mortgage, you will have the same Desjardins mortgage rate over your entire term, even if interest rates rise during that time. This gives you the ability to plan out how your mortgage balance will be reduced over your term while also giving you an added layer of certainty. Although a fixed-rate mortgage will have the same interest rate over the entire term, you may have to renew your mortgage at a higher rate when your mortgage term is finished. Out of all fixed-rate terms, the 5-year fixed mortgage term is generally the most popular, which gives you the peace of mind of having the same interest rate over a 5-year period.

| Term | Desjardins Rate | Canada's Lowest Rate |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

Desjardins Variable Mortgage Rates

A Desjardins variable rate mortgage gives you the ability to have a mortgage rate that will change along with the prime rate at Desjardins. This means getting a variable mortgage rate can be a good option if you expect mortgage rates to fall during your term. A Desjardins variable rate mortgage will have the same mortgage payment amount till the end of the term unless some situation mentioned in your agreement arises that requires your payment amount to be modified. The only difference in your monthly payments will be how much of the payment goes to interest on the mortgage, with more of your payments going to interest as your mortgage rate rises and vice versa. On the other hand, getting a variable-rate mortgage will give you less control over your mortgage rate, meaning that if interest rates rise, so will your mortgage rate. This is why a fixed-rate mortgage with Desjardins is more popular than a variable-rate mortgage.

| Term | Desjardins Rate | Canada's Lowest Rate |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

Desjardins Posted Rates

Desjardins Posted Rates are the official rates used when calculating your mortgage break penalty, the fee you pay if you want to break or refinance your mortgage early. Your mortgage payment, interest, and stress test will be based on a different rate which is usually lower than the posted rate.

Desjardins Mortgage Break Penalty

In situations that require you to break your mortgage contract before the term is up, you will be charged a mortgage break penalty. This can be because you want to pay off your mortgage sooner, change your mortgage terms, or refinance your mortgage with another lender. The table below shows how your mortgage break penalty will differ depending on the type of mortgage you have:

| Bank or Lender | Variable Rate Mortgage | Fixed Rate Mortgage |

|---|---|---|

| 3 Months’ Interest | Greater of 3 Months’ Interest or the IRD amount |

The difference between your current mortgage rate and Desjardin’s current posted rate for a term similar to the time left on your mortgage, less any rate discounts that you received. This difference in interest rates is used to calculate your mortgage break penalty.

To see how much you can expect to pay in prepayment charges, utilize the Desjardins mortgage penalty calculator below:

Are you looking to pay off your mortgage early? Or refinance the terms of your mortgage at a lower interest rate? Maybe you sold your home. Whatever the case, you most likely will have to pay a mortgage break penalty set by your lender. Whatever the situation, our calculator will help you determine the cost to break your mortgage so you can be confident about your mortgage decisions.

What is the remaining balance on your mortgage?

What is your current regular mortgage payment amount?

What is the term-length and type of your current mortgage?

What is your current mortgage interest rate?

If applicable, what was the rate discount you received when you signed your current mortgage agreement?

When did your current mortgage start?

Is the Property:

Who is your current mortgage lender?

What is Desjardins's current interest rate for a 1-year fixed rate mortgage?

What would you like to do?

Please complete all fields before calculating.

By using the calculator, you agree to our Terms of Service

Desjardins Prime Rate

The prime rate at Desjardins is important to know, as it is the foundation for mortgage interest rates. Desjardins determines the interest rates for different lending products by adding or subtracting a spread to the prime rate. Since mortgages are secured by a home, your Desjardins mortgage rate will be calculated by subtracting a spread from the prime rate. Other lending products where the prime rate is used to determine your interest rate are:

Current Desjardins Prime Rate: 4.45%

Desjardins Prime Rate History

Desjardins History

Desjardins Mortgage Features

Desjardins mortgage protection insurance

For people looking to purchase a home, Desjardins offers monthly mortgage protection insurance for both life and disability coverages. Mortgage protection insurance can be a good way to give yourself peace of mind when taking out a mortgage, with this coverage paying some or all of your mortgage amount if you become disabled or pass away. Since there are only a few health questions required before getting coverage, this may be a good way to cover your mortgage if you cannot qualify for general life insurance. It can also be a good way just to add more protection for your family. The cost of coverage will depend on the type of coverage you get, your age, and the size of your mortgage. The maximum limit for Desjardins’ life insurance coverage is $10 million.

Desjardins prepayment features

Desjardins offers you multiple ways to pay off your mortgage sooner, including the following features:

Increase your payment frequency: Desjardins gives you the ability to choose how often you want to pay your mortgage, with the options of monthly, weekly, and bi-weekly payments. Even if you decide you want to speed up or slow down how frequently you pay your mortgage, Desjardins lets you change this at any time. By choosing weekly or bi-weekly payments instead of monthly, you will be making more payments towards your principal balance, meaning you will pay less interest over time.

Increase your payment amount: You will have the option to increase your mortgage payments to up to double the original amount. This will help you reduce the time it takes to pay down your mortgage and will also reduce your lifetime interest, considering that all of the extra mortgage payment amounts will go directly to your mortgage balance.

Desjardins prepayment limit: Your yearly prepayment limit will be 15% of your original mortgage balance. Any prepayment towards your mortgage above this limit will trigger a prepayment penalty, meaning if you plan to pay down your mortgage balance very aggressively, an open mortgage may be a better option.

Desjardins Green Homes Program

For people looking to purchase or build a sustainable and energy-efficient green home, Desjardins offers up to $2,000 in cashback. Desjardins qualifies homes as green homes based on their LEED Canada, Novoclimat, or ENERGY STAR certifications. Besides the cashback benefit, a green home can help reduce your carbon footprint while saving you money on energy bills. Additionally, if you have mortgage insurance from CMHC or Sagen, you can also receive a 25% refund on your mortgage insurance through CMHC Eco Plus or Sagen Energy Efficient Housing Program.

Desjardins prepayment penalty refund

If you are to sell your home before your mortgage is paid off, it's likely you will have an initial mortgage break penalty. However, Desjardins offers the ability to get a full prepayment penalty refund when you apply for a new Desjardins mortgage within 90 days, only with the same terms however. If your new mortgage amount is equal or greater than your prior mortgage amount, you will have all your prepayment penalties refunded. If you apply for a smaller mortgage than your prior one, you will receive only a partial refund.

Other Desjardins Mortgage Products

Desjardins HELOC

As you build equity in your home over time by paying down your mortgage, a Desjardins home equity line of credit (HELOC) is a good way to utilize that equity. HELOC is a revolving credit that lets you borrow up to 65% of your home’s value. To be eligible for HELOC, you must have at least 20% equity built up in your home. Once you have more than 20% equity, you can set up a HELOC and start borrowing from the equity built over the minimum 20%, up to a maximum of 65% of the home’s value. This makes a HELOC great for consolidating debts, doing home renovations, and using it for a down payment on a second property.

Desjardins rental property mortgage

Desjardins offers you the ability to purchase a rental property using residential rental property financing. Desjardins will consider both your needs and the quality and value of the building when determining your loan amount, while allowing you to use other properties in your real estate portfolio as collateral. You are able to get loan terms between 1 and 10 years, while choosing a fixed, variable, or a combined loan. You will also be able to take advantage of the multi-project option Desjardins offers, which allows you to re-borrow up to your initial loan amount, giving you more financial flexibility.

Desjardins hybrid mortgage

A Desjardins hybrid mortgage allows you to split up your mortgage into 2 or more loan tranches, which allows each co-borrower the ability to customize their interest rate, term, and payment frequency. This can be a great option if you are having family members pay part of the loan with you, or are purchasing a shared property. The ability to customize your payments to be different from other tranches of the loan gives everyone involved the flexibility to be able to get a loan for a property on the terms that are best for their situation.

Branch Locations

Desjardins is comprised of 204 caisse populaires and credit unions in the provinces of Quebec and Ontario and 669 service centres. You can find the nearest branch using Desjardins’ branch locator. It is also noteworthy that Desjardins is the third largest employer in the financial sector in Canada. It is also noteworthy that Desjardins is the third largest financial sector employer in Canada.

Desjardins Structure

Desjardins has multiple business lines across financial services, including:

- Personal and business financial solutions: This includes financing solutions such as mortgages, credit cards, line of credits, as well as business and capital market services.

- Wealth management and health & life insurance: This division includes wealth products and services for consumer and group needs.

- Property and casualty insurance: This includes Desjardins home insurance, auto insurance, and other coverages to protect against damage.

Contact Desjardins

Besides meeting with a mortgage representative at your local Desjardins caisse populaires or credit union, you can contact a mortgage representative at the number 1-844-626-2476 for Canada and the US, and 514-745-9499 for the Montreal area. As well, you can apply for a mortgage through the online Desjardins mortgage application portal.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.