Reverse Mortgages in Canada 2026

What is a reverse mortgage?

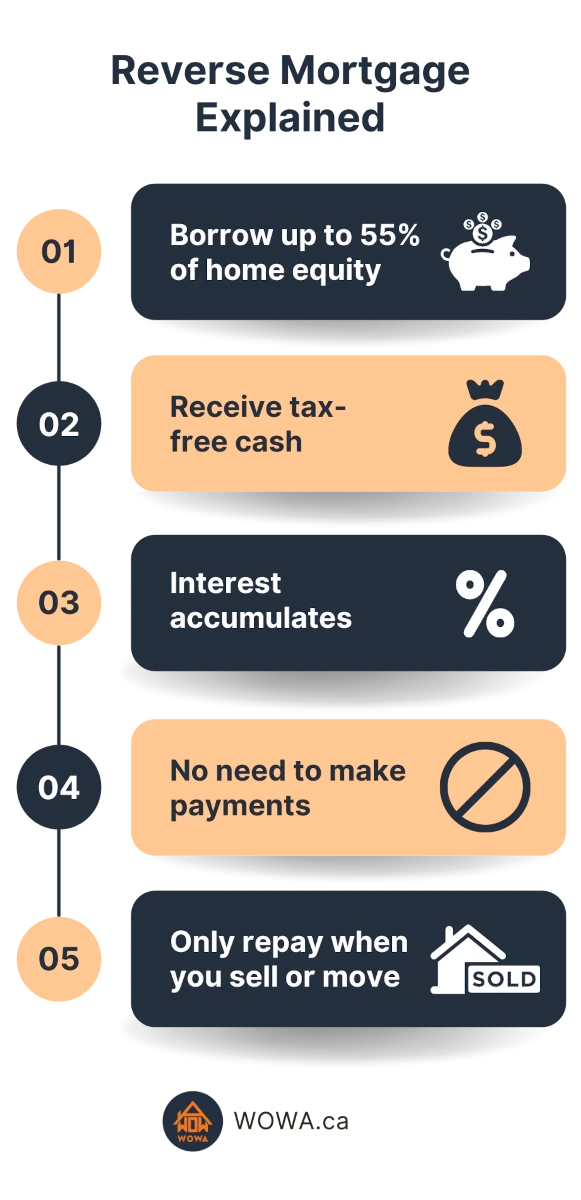

A reverse mortgage is a loan that lets older homeowners borrow against their home equity without making regular monthly mortgage payments. In Canada, reverse mortgages are available to homeowners aged 55 or older, and the loan is repaid later when the home is sold, the borrower moves out, or the last borrower dies.

Unlike a traditional mortgage or a home equity line of credit (HELOC), a reverse mortgage does not require regular payments. Instead, interest is added to the balance over time, which means the amount owing grows and the homeowner’s equity can decline. That trade-off is why reverse mortgages are usually best suited to homeowners who want to stay in their home and need access to cash in retirement.

In Canada, reverse mortgages are commonly used by homeowners aged 55+ who want to supplement retirement income, pay off debt, cover healthcare or home-repair costs, or access cash without moving.

Reverse Mortgage Features

A reverse mortgage can provide tax-free cash as a lump sum, regular advances, or a combination of both, depending on the lender and product. You still own your home, and the money you receive is borrowed money rather than income, so it is tax-free and does not affect Old Age Security (OAS) or Guaranteed Income Supplement (GIS) benefits.

Many Canadian reverse mortgage products also include a no negative equity feature, which generally means you will not owe more than the fair market value of your home when the mortgage is repaid.

Reverse Mortgage vs Traditional Mortgage

A traditional mortgage usually requires regular mortgage payments of principal and interest, which gradually reduce your debt over time, and borrowers are qualified based heavily on income, debt ratios, and credit score. A reverse mortgage works differently: regular payments are not required, and eligibility depends more on age, home value, property type, location, and lender criteria.

The trade-off is cost. Reverse mortgage rates are generally higher than mortgage rates and HELOC rates, and the balance grows over time because interest is added to what you owe. That means reverse mortgages can be useful, but they are not interchangeable with a standard mortgage.

If you meet the eligibility criteria, you may be able to borrow up to 55% of your home’s equity through a reverse mortgage, or even higher, based on some special reverse mortgage products. In comparison, with a conventional mortgage, you can borrow up to 80% of your home's value, and with an insured mortgage, you can access between 90% and 95% of your home’s value. You can use a reverse mortgage calculator to determine how much you can borrow.

| Feature | Traditional Mortgage | Reverse Mortgage |

|---|---|---|

| Payments | Regular principal and interest payments are required | Regular payments are not required |

| Debt over time | Debt generally decreases as you make payments | Debt generally increases as interest is added |

| Qualification | Based heavily on income, debt ratios, and credit score | Based more on age, home value, property type, location, and lender criteria |

| Interest rates | Usually lower than reverse mortgage rates | Generally higher than mortgage and HELOC rates |

| Borrowing amount | Up to 80% of home value for a conventional mortgage; 90% to 95% with an insured mortgage | Up to 55% of home value, or higher, with some special products |

| Best suited for | Borrowers who can make regular payments and want to buy or refinance a home | Retired homeowners who want to access home equity without making regular payments |

Reverse Mortgage Eligibility in Canada

To qualify for a reverse mortgage in Canada, lenders generally require that all title holders meet the age requirement, that the home is your primary residence, and that the property meets lender rules for type, condition, value, and location. The amount you can borrow typically depends on the age of the youngest borrower, the home’s value, and the lender’s underwriting criteria. Generally, reverse mortgage lenders in Canada require these conditions to be met:

- Everyone on the home's title is 55 or older. The higher their age, the more money they can borrow in a reverse mortgage.

- The home is your primary residence (you live there for six months minimum each year). Primary residence status is important because almost all proceeds from the sale of your primary residence can be used to pay your debts. In contrast, part of the proceeds from selling other properties belongs to CRA as income tax on capital gains.

- The home type is detached, semi-detached, condo or a townhouse.

- All property title holders apply as joint borrowers with you.

- Province availability also varies by lender. HomeEquity Bank’s CHIP Reverse Mortgage is available in all 10 provinces. Equitable Bank is only available in Alberta, British Columbia, Ontario, and Quebec, and Home Trust is only available in Ontario, British Columbia, Alberta, and Nova Scotia, with lending-area restrictions

You may also need to pay off and close any existing mortgage or HELOC secured by the home, since the reverse mortgage lender may require first-position security. In some cases, the lender will allow the reverse mortgage proceeds to be used for that payout.

How Does A Reverse Mortgage Work in Canada?

Since reverse mortgage lenders want their claim to have a first position on the title, any loans tied to your home must be paid off beforehand, such as a mortgage or a HELOC. You then choose to receive a lump sum or regular payments, which can be used for anything, such as household expenses or renovations. These payments are not subject to income tax because they are not income; they are money you borrowed.

A reverse mortgage can be particularly useful for older homeowners who have a large amount of equity in their home but are finding their income (their pension, retirement funds and potentially their salary) inadequate. In other words, reverse mortgages are suitable for those who are house-rich but cash-poor.

Once approved for a reverse mortgage, you can receive the funds as a lump sum, scheduled advances, or a mix of both, depending on the product. You do not need to make regular mortgage payments, but interest continues to accrue and is added to your balance over time.

The reverse mortgage becomes due when you sell the home, move out, the last borrower dies, or you default under the mortgage terms. Since lenders set their own repayment timing and default rules, borrowers should review the contract carefully and ask about prepayment charges, estate timelines, and what events could trigger default. Examples of such events might include not keeping up with home maintenance or being late on your property tax payments.

In Canada, your estate will be responsible for repaying the reverse mortgage after your death, most likely by selling your home. If your estate does not do this, the bank will sell the home and recover what it is owed. A reverse mortgage will never create a liability for your beneficiaries, nor will it affect their interest in your other assets. Canada only has a few reverse mortgage providers: HomeEquity Bank, Equitable Bank, Home Trust, and Bloom Financial. HomeEquity Bank's Canadian Home Income Plan is also known as CHIP. Home Trust, Equitable Bank, and Bloom Financial offer their product in limited geographic areas.

Reverse Mortgage Pros vs Cons

Pros/Advantages

- No payments required until you move or sell: This can be helpful for those who cannot afford to make payments, or even interest-only payments, that would normally be required for other loans.

- Turns your home equity into tax-free cash: This allows you to unlock your home equity without selling your home. Thus, a reverse mortgage can serve as an alternative to downsizing for retirement if you want to keep your home either because of an emotional connection or because you think it will appreciate fast.

- Allows you to still own your home: You remain the owner of the home, not the bank.

- Flexible options can set up a steady stream of cash: You can choose to borrow a lump-sum amount or set up recurring monthly, quarterly, semi-annual, or annual advances.

- Does not affect OAS (Old Age Security) or GIS (Guaranteed Income Supplement) benefits

- You can use it as a down payment for a second home.

Cons/Disadvantages

- Higher interest rates than regular mortgages: This increases the cost of borrowing.

- Requires a home value of at least $300,000 for a CHIP Max or CHIP Open reverse mortgage and $250,000 for an Equitable Bank reverse mortgage, a regular CHIP reverse mortgage, or a Home Trust reverse mortgage.

- Interest accrued will reduce your home equity: In exchange for requiring no interest payments during the life of the mortgage, your home equity will be reduced.

- Fees if you pay off the reverse mortgage early: Paying off a reverse mortgage early will incur a prepayment charge

- May require you to borrow a minimum amount: For example, Equitable Bank requires you to borrow at least $25,000 initially, even if you do not need the full amount upfront.

How Rising and Falling Home Prices Affect Reverse Mortgages

When home prices go up, the part of the home that really belongs to the homeowner, their equity, can also go up. That can make a reverse mortgage more helpful, because the homeowner may be able to unlock more money from their home later if needed, usually after a new appraisal and lender approval. In simple terms, when the home becomes more valuable, the homeowner may have a bigger cushion of equity to borrow against. In a rising housing market, the increase in a home’s value may help offset some or even all of the growing reverse mortgage balance.

In a flat or declining housing market, however, the homeowner may be limited to the original amount they were approved to borrow. As that money is used and interest accrues over time, the homeowner’s remaining equity will shrink. If they later need to sell the home or move into another living arrangement, they may have less equity left than expected.

How to Get a Reverse Mortgage

Step 1: Submit an Initial Application

You can usually start by completing an online application with a reverse mortgage lender. At this stage, you may be asked for basic information about yourself, your home, and your finances. Based on the information you provide, the lender may give you an initial estimate of how much you could borrow.

Step 2: Speak With the Lender

After your application is reviewed, the lender will usually contact you to answer questions and learn more about your situation. Unlike a traditional mortgage, reverse mortgages generally do not require proof of employment income or a down payment. However, the lender will want to know whether there are any existing mortgages, HELOCs, or other loans registered against your home. In many cases, those debts may need to be paid off using the reverse mortgage proceeds.

Step 3: Review the Offer and Complete the Appraisal

If you decide to move forward, the lender will confirm the terms of the reverse mortgage with you. You will also need to meet with an independent lawyer for independent legal advice before the reverse mortgage can be finalized.

Depending on the lender and product, you may be able to receive the funds as a lump sum, scheduled advances, or a combination of both. For example, you might take an initial lump sum and then receive additional advances later.

The lender will also arrange a property appraisal to determine your home’s market value. Your final borrowing limit will be based in part on this appraisal.

Step 4: Receive the Funds

Once the mortgage is finalized, the funds are advanced according to the payment option you selected. In most cases, no regular mortgage payments are required while you continue to live in the home and meet your mortgage obligations. The loan is repaid later, such as when the home is sold or the last borrower leaves the home.

Where Can You Get a Reverse Mortgage in Canada?

Reverse mortgages in Canada are available from a limited number of lenders, including HomeEquity Bank, Equitable Bank, Home Trust, and Bloom Financial. Availability can vary by province, city, property type, home value, and lender underwriting rules, so not every homeowner will qualify with every provider.

HomeEquity Bank offers the CHIP Reverse Mortgage, which is available across all 10 provinces. Equitable Bank offers reverse mortgages in selected urban areas in British Columbia, Alberta, Ontario, and Quebec. Home Trust offers its EquityAccess reverse mortgage through mortgage brokers in Ontario, British Columbia, Alberta, and Nova Scotia, subject to lending-area restrictions. Bloom Financial also offers reverse mortgages in selected provinces, including Ontario, Alberta, and British Columbia.

CHIP Reverse Mortgage

HomeEquity Bank’s CHIP reverse mortgage is the most popular option in Canada and is available in all provinces. To qualify for a CHIP reverse mortgage, you must be 55 years or older, your spouse must also be 55 years or older, and your home must be worth at least $250,000. HomeEquity Bank determines a maximum lending amount for you, which would at most be 55% of your home market value, and HomeEquity Bank guarantees that the amount that you will have to repay eventually will not exceed the market value of your home or the proceeds of sale if it is sold.

The reverse mortgage can be paid off in full early; however, fees may be charged. Advances can be received as a lump-sum payment, or monthly installments can be scheduled. Homeowners will also keep any appreciation in the value of the home.

Equitable Bank Reverse Mortgage

Equitable Bank’s reverse mortgage is only for properties in urban centres in British Columbia, Alberta, Ontario, and Quebec, and for homes with a value of at least $250,000. You must also be 55 years old or older, and live in your home for more than 6 months per year as your primary residence. With Equitable Bank’s Reverse Mortgage Flex PLUS, you can borrow up to 59% of your home’s value.

The minimum amount you can borrow from Equitable Bank's Reverse Mortgage is $25,000. Equitable Bank offers a no negative equity guarantee, where you will never owe more than the market value of your home when it is sold.

You can choose from a variety of fixed terms, ranging from 6 months to up to 5 years. If you choose a fixed interest rate, you can not schedule payments. Instead, payments will be requested as single advances, with the minimum amount of each payment being $500. These payments can be requested at any time.

Payments can be scheduled for up to 15 years if your interest rate is adjustable. Minimum payments depend on the frequency of your scheduled payments, with each payment accruing interest at the current adjustable interest rate at the time of each payment.

Under both the fixed and adjustable interest rate products, there is an initial minimum payment of $25,000.

Equitable Bank’s Minimum Disbursements by Scheduled Frequency

| Frequency | Minimum Payment |

|---|---|

| Monthly | $500 |

| Quarterly | $1,500 |

| Semi-Annually | $3,000 |

| Annually | $6,000 |

Home Trust Reverse Mortgage

Home Trust's reverse mortgage offering is the EquityAccess reverse mortgage for Canadian homeowners aged 55 and older. Its reverse mortgage is currently available through mortgage brokers in Ontario, Nova Scotia, Alberta, and British Columbia. Home Trust also highlights a no negative equity guarantee, which generally means borrowers will not owe more than the fair market value of their home at repayment, provided they continue to meet their mortgage obligations. Home Trust offers both a lump-sum option and a product that combines lump-sum and scheduled advances.

Bloom Financial Reverse Mortgage

Bloom reverse mortgages are currently available in Ontario, Alberta, and British Columbia, and it markets its reverse mortgage as a way to access up to 55% of a home’s value without required monthly mortgage payments, while allowing the homeowner to keep ownership of the property. Bloom also highlights transparent flat fees, including processing, appraisal, and independent legal advice-related costs.

Reverse Mortgage Rates in Canada

Reverse mortgage rates in Canada are generally higher than regular mortgage rates and HELOC rates because lenders are repaid later and take on more risk over time. If you want detailed rate tables, product comparisons, APR information, and lender-by-lender breakdowns, see our Reverse Mortgage Interest Rates page.

Today's Reverse Mortgage Rates

For a full list of rates for various terms and products, visit our reverse mortgage rates page.

Alternatives to Reverse Mortgages

Before getting a reverse mortgage, it is worth comparing other ways to access cash or reduce housing costs. Alternatives include selling and buying a smaller home, renting, moving into assisted living, getting a HELOC, getting a traditional mortgage, or using another type of personal loan.

HELOC

A HELOC may be cheaper than a reverse mortgage, but it usually requires income qualification and at least interest payments. It may suit homeowners who have enough income to support payments and want lower borrowing costs.

Traditional Mortgage or Refinance

A regular mortgage or mortgage refinance may also cost less than a reverse mortgage, but qualification is usually stricter, and monthly payments are required. This may work better for homeowners with sufficient income and stronger credit.

Downsizing or Selling

Selling the home and buying a smaller home, renting, or moving to a different housing option can free up equity without taking on compounding reverse-mortgage interest. For some retirees, this may leave more flexibility and reduce long-term borrowing costs.

Personal Loan or Other Financing

Depending on the amount needed, another type of loan may be more suitable. The right option depends on your income, goals, housing plans, and whether preserving home equity for later is important.

Frequently Asked Questions

A reverse mortgage may be worth considering if you want to stay in your home, need access to cash, and do not want the burden of regular monthly mortgage payments. It may be less suitable if preserving as much home equity as possible is your priority, or if a cheaper option, such as a HELOC, refinance, downsizing, or selling, is realistic for you.

The biggest drawbacks of a reverse mortgage are usually higher interest rates, declining home equity over time, and the possibility that your estate will have less value left after the loan is repaid. There are also prepayment charges depending on when you want to repay the mortgage.

Yes, you can make prepayments up to a certain limit without charge.

- Interest: For Equitable Bank, you can prepay outstanding interest once per month.

For CHIP, you can only prepay interest through fixed automatic withdrawals. - Principal Payments: For Equitable Bank, you can prepay up to 10% every 12 months.

For CHIP, you can prepay up to 10% every 12 months within 30 days of the anniversary date of the reverse mortgage. - After 5 Years with Equitable Bank, you can prepay more than 10% within 30 days of the interest reset date of your mortgage.

- After 10 Years with Equitable Bank, you can prepay more than 10% at any time.

- After 5 Years with CHIP, you can prepay any amount within the 30 day period after your interest reset date.

Reverse Mortgage Pre-Payments

| Equitable Bank | CHIP | |

|---|---|---|

| Interest Payments | Prepay interest once per month. | Prepay interest through fixed withdrawals. |

| Principal Payments | Up to 10% of your principal every 12 months. | Up to 10% of your principal and outstanding interest every 12 months within 30 days of your mortgage’s anniversary date. |

| After 5 Years | Any amount within 30 days of your interest reset date or with three months of advanced notice. | Any amount within 30 days after your interest reset date. |

| After 10 Years | Any amount at any time. | Any amount at any time. |

Reverse mortgage payments are not taxable. Since the money that you receive is a loan advance, the money would not be taxed as income.

A reverse mortgage is repaid when you sell your home, move, default, or die. The lender will usually guarantee that you will not owe more than the fair market value of your home. If you pass away, your estate will repay your reverse mortgage.

Since no payment is required, a reverse mortgage default occurs if you break the terms of your reverse mortgage contract, such as not maintaining your home, not paying property taxes, not insuring your home or lying on your application.

If you already have a mortgage, you can still get a reverse mortgage. Your mortgage will need to be paid off from the funds from the reverse mortgage so that the reverse mortgage can be the first lien on the home.

If your spouse dies, you will continue to be a borrower. The reverse mortgage will only be required to be paid back if both borrowers die in the case of spouses, if you sell the home, or you move.

Yes, bad credit will not prevent you from getting a reverse mortgage.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.