RFA Bank Mortgage Rates & Reviews

What You Should Know

- RFA offers GICs and a variety of mortgages.

- RFA only offers GICs through investment advisors and investment dealers.

- Most mortgages are offered via mortgage brokers, but members of the public can obtain a mortgage directly from RFA.

- RFA does not offer pre-approval.

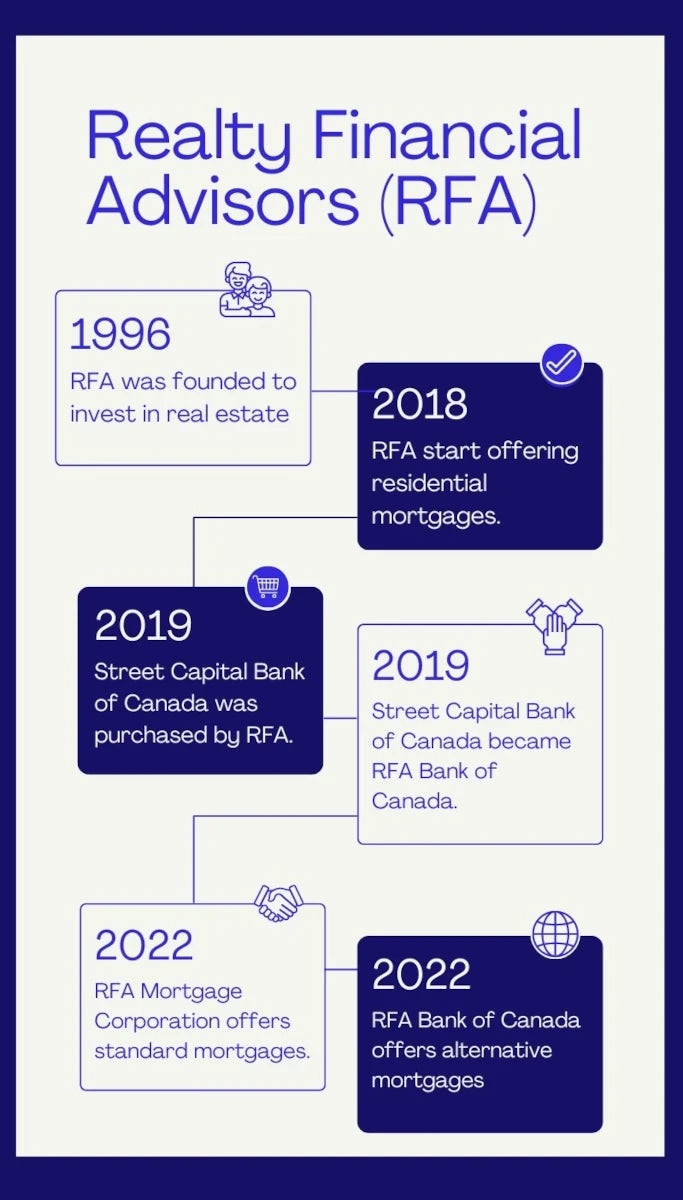

Realty Financial Advisors (RFA) was founded in 1996 as an investment firm focused initially on commercial real estate. In 2018, RFA entered the residential lending business by offering residential mortgages through brokers. In 2019, RFA acquired Street Capital Bank of Canada and renamed it RFA Bank of Canada. In the RFA group, RFA Mortgage Corporation specializes in Prime mortgages, while RFA Bank of Canada is an alternative mortgage lender.

Street Capital Financial Corporation was founded in 2007 as a residential mortgage lender. In the year 2017, Street Capital received approval from the Office of the Superintendent of Financial Institutions to become a federally regulated bank. Thus Street Capital Bank of Canada was born. Subsequently, it was acquired by the RFA and renamed RFA Bank of Canada.

Currently, the main products of RFA which are of interest to the public are residential mortgages and GICs. Because of CDIC insurance, their GICs are as safe as those offered by the largest Canadian banks. RFA mortgages are offered in all Canadian provinces except for the province of Quebec. Their business model is more geared towards providing services through mortgage brokers instead of advertising and incurring customer acquisition costs.

Similar to their mortgages, their GICs are priced competitively. Unfortunately, their GICs are only sold through investment advisors and deposit dealers.

RFA Bank Mortgage

RFA offers prime mortgages for those who want to purchase a home, refinance their mortgage or switch their mortgage from another lender. A prime mortgage is a mortgage which is considered to have a low risk of default. A prime mortgage requires a gross debt service ratio below 39% and a total debt service ratio of at most 44%. For a mortgage to be considered prime, the borrower must also pass the stress test and have a good credit history (a credit score over 660).

| Term | RFA Bank Rate | Canada's Lowest Rate |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

RFA offers fixed-rate mortgages and adjustable-rate mortgages. It might also offer variable-rate mortgages. RFA prime mortgages include high-ratio mortgages, conventional insurable mortgages and conventional uninsurable mortgages. A mortgage with a loan-to-value (LTV) ratio greater than 80% is considered a high-ratio mortgage, while a mortgage with an LTV of less than 80% is considered a conventional mortgage.

Obtaining a high-ratio mortgage requires purchasing mortgage insurance. CMHC is the largest provider of mortgage insurance in Canada. CMHC limits its mortgage insurance to properties with a price tag under the 1 million dollar mark. As a result, a mortgage for a property more expensive than 1 million dollars is considered uninsurable.

The amortization period is the length of time in which a mortgage will be paid back. The most common amortization in Canada is 25 years. If you can afford to pay larger installments, you can reduce your interest payment by choosing a shorter amortization period. However, asking for an amortization longer than 25 years makes the mortgage ineligible for CMHC insurance. Moreover, most lenders would ask for a higher mortgage rate when you increase the amortization beyond 25 years.

In a fixed-rate mortgage, interest rate, amortization period and installment amount are all fixed for the term of the mortgage.

An adjustable-rate mortgage interest rate is fixed relative to the RFA prime rate. An adjustable-rate mortgage has a fixed amortization period. Thus the amount of principal to be paid in each installment is predetermined. Any increase in the interest rate results in larger installments, while any decrease in the interest rate results in smaller installments.

In contrast, a variable rate mortgage is a mortgage where the interest rate is fixed relative to the prime interest rate and would change with changes in the prime rate, but installments are fixed. An increase in the rate of interest results in a longer amortization period, while a decrease in the rate of interest results in a shorter amortization period.

Prepayment

A mortgage can be either open or closed. An open mortgage has the flexibility to be repaid at any time while paying a closed mortgage before the end of the term requires paying a penalty. Because rates on closed mortgages are considerably lower, most people choose closed mortgages, and open ones are quite uncommon.

RFA offers attractive terms, and their mortgages are quite flexible. RFA mortgages have prepayment privileges totalling 20% of the principal per year. Among mortgage lenders, 20% prepayment per year is on the generous side. But as is common in the Canadian mortgage industry, making prepayments greater than your prepayment privilege results in incurring prepayment penalties.

The prepayment penalty on a fixed-rate mortgage is calculated as the greater of 3 months of interest and the interest rate differential. Interest rate differential is the amount of interest that your lender would lose by loaning the money you just prepaid for the remainder of your term at their posted rate. For adjustable-rate mortgages and variable-rate mortgages, the prepayment penalty is three months of interest.

If you want to sell your house, you need to remove the lender's lien before being able to transfer the title. To remove the lien, you would have to pay down the mortgage, which involves fully prepaying your mortgage.

Fortunately, RFA offers two choices for you to avoid prepayment penalties when you need to move. One option is to port your mortgage to your new house, and the second option is for your purchaser to assume your mortgage.

When porting your mortgage, you repay it when selling your house. You have a limited time to take out the mortgage on another property to avoid prepayment penalties. The effect of porting a mortgage is changing the collateral supporting the mortgage. When porting your RFA mortgage, RFA Bank allows you to increase your mortgage balance with a new blended rate.

Transferring a mortgage to a purchaser can be done only if the purchaser satisfies lending criteria set by RFA.

Alternative Mortgage

For subprime borrowers, those who do not qualify for a prime mortgage, RFA Bank of Canada offers subprime mortgages which it has to keep on its balance sheet. The interest rate on these loans depends on the credit score of the borrower and the loan-to-value ratio of the mortgage.

How to Take Out an RFA Mortgage

You can email the customer service department at SM-CustomerService@rfabank.ca. The customer service department would refer you to the sales department, and the sales department would discuss your mortgage needs. Alternatively, you can call them at 647.259.7873 or 1.877.416.7873.

RFA Prime Rate

Current RFA Prime Rate: 4.45%

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.