Subprime Mortgages in Canada

What You Should Know

- Subprime mortgages, also known as private mortgages or B lender mortgages, are for borrowers with a poor credit score, low income, high debt, or past bankruptcy.

- A credit score below 660 might classify you as a subprime or near-prime borrower.

- Subprime mortgages have higher interest rates than those offered by the major banks to prime borrowers.

- The subprime mortgage crisis in 2008 led to reforms and put stricter regulations on the banking industry.

What is a Subprime Mortgage?

A subprime mortgage is a type of mortgage loan that is typically offered to homebuyers with less-than-perfect credit. Because subprime borrowers are considered to be at a higher risk of defaulting on their loans, Canadian subprime mortgages usually come with higher interest rates and less favourable terms than prime mortgages.

While they might sound like a forbidden type of mortgage, especially after the 2008 financial crisis, subprime mortgages are more common in Canada than you think! Did you know that 12% of Canadians are subprime borrowers? That surprising statistic is based on estimates by TransUnion Canada. TransUnion also estimated in 2020 that about a third of Canadians have a "below-prime" credit score. Subprime borrowers still need a way to finance their home purchase, and this is where subprime mortgages come into play in Canada.

Subprime mortgage lenders are more commonly known as “B Lenders” and private mortgage lenders in Canada. You can typically access subprime lenders with a mortgage broker. B Lenders and private lenders fill the gap left behind by “A Lenders”, which include the major banks, as A Lenders have stricter requirements due to government regulations. Subprime mortgage lenders are not directly regulated by the government, which allows them to offer bad credit mortgages to borrowers that might otherwise be denied by a bank or credit union.

Relaxed mortgage rules for subprime mortgages include the possibility of an amortization period as long as 40 years and a down payment as little as 10% (or a loan-to-value (LTV) ratio of 90%). However, some private lenders may require a larger down payment, or they might have a lower maximum LTV ratio.

Why Is It Called a Subprime Mortgage?

The term "subprime" refers to the creditworthiness of the borrower. A prime borrower is considered to be someone that is at low risk of defaulting on a mortgage loan. This is usually based on their credit score. On the other hand, a subprime borrower is considered to be a higher risk than a prime borrower, and as such, they will pay a higher interest rate for their mortgage.

This relates to prime rates being given to a bank’s “prime” borrowers. If you have a good credit score and strong financials, you will be able to get better rates that are reserved for a bank’s prime customers. This could include discounts to their posted mortgage rates. Subprime borrowers will see higher rates, if they are approved in the first place.

Who Are Subprime Mortgages For?

Subprime mortgages typically target those with poor credit, high levels of debt, or low income, that would otherwise not be accepted by a bank. A good credit score in Canada is considered to be 660 or higher, while a credit score of at least 600 is required in order to be eligible for CMHC-insured mortgages. While the definition of a prime borrower varies by lender, you will generally need to have a credit score of at least 660 in order to qualify for the best mortgage rates at A lenders.

If you have a credit score lower than 660, you might need to consider a subprime mortgage from a B mortgage lender instead. In the United States, the Consumer Financial Protection Bureau (CFPB), a federal government agency, defines someone as being a subprime borrower if they have a credit score between 580 and 619. They consider someone to be a prime borrower if they have a credit score between 660 and 719. There are other extensions of this range too, such as being deep subprime with a credit score below 580, or being super-prime with a credit score above 720.

Subprime vs Prime Credit Scores

| Classification | Credit Score Range |

|---|---|

| Deep Subprime | Less than 580 |

| Subprime | 580 - 619 |

| Near-prime | 620 - 659 |

| Prime | 660 - 719 |

| Super-prime | 720 or higher |

As defined by the U.S. Consumer Financial Protection Bureau

Subprime mortgages are only meant as a temporary solution until the borrower improves their credit and can qualify for a regular mortgage. For example, the typical subprime mortgage term ranges from 6 months to 24 months. Since the average subprime mortgage rate is 6.5% to 15%, you wouldn’t want to have to pay this interest rate for very long!

However, many people found themselves stuck in these high-interest loans in the United States in the early 2000’s, and when the housing market crashed in 2007, they were left underwater on their mortgages. This was known as the subprime mortgage crisis. Being underwater on a mortgage means that you owe more on your mortgage than the home is actually worth. This led to a wave of foreclosures and further instability in the housing market.

Lenders in Canada and especially the United States have since tightened up their standards for issuing subprime mortgages, but there are still some people who may benefit from this type of loan. If you're considering a subprime mortgage, make sure you understand the risks involved.

Snapshot of Subprime Mortgages

Average Subprime Mortgage Interest Rate: 6.5% to 15%

Typical Subprime Mortgage Term: 6 months to 24 months

Average Subprime Mortgage Size: $260,120

Source: CMHC Residential Mortgage Industry Report (October 2021)

Types of Subprime Mortgage Borrowers

While subprime mortgages are often an alternative mortgage lender out of necessity for those denied a mortgage at a bank, there are many other use cases for them. This includes those who have a past bankruptcy or consumer proposal, if you are recently self-employed, if you have unconventional income sources, or a high debt-to-income ratio. The section below takes a look at the characteristics of common subprime mortgage borrowers in Canada.

For Borrowers with a Past Bankruptcy or Consumer Proposal

If you have had a recent bankruptcy or consumer proposal in the past, it will be difficult for you to qualify for a mortgage at a bank or credit union. However, you may still be able to qualify for a subprime mortgage.

Depending on the subprime mortgage lender, they may require that your bankruptcy or consumer proposal be discharged for at least one year before considering you for a loan. This requirement can be as little as three months or less after being discharged from bankruptcy. On the other hand, traditional lenders, such as banks, may require a minimum of two years to pass before being able to qualify for a prime mortgage.

For Self-Employed Borrowers

While many banks offer self-employed mortgages, they often require you to have been self-employed with proof of income for at least two years. This is to ensure that your income is steady and can be used to repay your mortgage loan.

If you have recently started a business or became self-employed for less than two years, you might require a subprime mortgage from a private lender or B lender. Some lenders might not even verify your self-employment income for a subprime mortgage! This is known as a stated income mortgage, which is legal in Canada. In comparison, stated income mortgages are illegal in the United States.

For Borrowers with Unconventional Income Sources

Unconventional income sources, such as borrowers that rely on commission income, investment income, or freelance income, may have difficulty obtaining a mortgage. That’s because these income sources can be unstable or fluctuate from year-to-year. Similar to self-employed borrowers, a stated income mortgage or no income verification mortgage can help borrowers with irregular or unconventional income.

For Borrowers with a High Debt-to-Income Ratio

Mortgage lenders use your debt-to-income (DTI) ratio in order to determine whether or not you qualify for a loan based on your current debt load. It also plays a role in how much you are able to borrow.

DTI is calculated by dividing your total monthly debts by your gross monthly income. Lenders typically like to see a DTI of 36% or less, but some may go as high as 44%, the highest allowed by the CMHC for insured mortgages. If your DTI is too high, you may not be able to qualify for a regular mortgage at all. Even if you do, you may only be able to borrow a smaller amount than you otherwise would have been able to.

To lower your DTI, you can either work on increasing your income or decreasing your debts. If you're not able to do either of those things, there's still hope - and that’s where subprime mortgages come in. Subprime mortgages may allow a maximum total debt service (TDS) ratio as high as 50%, while some private lenders might not have a maximum limit at all!

Interest-Only Mortgages

Borrowers that have cash flow issues might look towards an interest-only mortgage. Since the borrower will only be paying interest payments, rather than principal payments, the monthly mortgage payments are more manageable. However, as long as the principal is not being paid off, the borrower will still owe the same amount of money at the end of the mortgage term. Interest-only mortgages should only be used as a temporary measure while the borrower improves their income and pays down debt.

The Subprime Mortgage Crisis

The term “subprime mortgage” comes with an unpleasant and sometimes even negative connotation due to the subprime mortgage crisis in the United States.

The U.S. housing bubble, and the eventual market crash in 2008, was mainly caused due to subprime mortgages. The root cause was the ease that banks lent out mortgages to subprime borrowers, even to those who could not afford or keep up with their mortgage payments. That’s because banks and hedge funds bundled these subprime mortgages into mortgage-backed securities (MBS), which were “insured” with credit default swaps (CDS), and then sold off to investors.

Many of these subprime mortgages were adjustable-rate mortgages (ARMs), which had low initial interest rates that would later reset at much higher levels, often causing borrowers to default as they could only afford the initial low rate.

The most popular subprime adjustable-rate mortgage (ARM) was the 2/28 ARM, where the first two years of the loan features a very low "teaser" rate that is fixed, while the remaining 28 years of the 30 year amortization is at a variable interest rate, and is much higher. Lured in by the initial low teaser rates, only to be financially crippled by higher interest rates later, was the basis of the subprime business model.

The table below compares initial "teaser" subprime mortgage rates offered in the United States from 2004 to 2007 with the full variable rate that borrowers would face after this promo period. The teaser rates ranged from 7% to 8%, and the full variable rate ranged from 9% to 11%, both higher than the prime rates offered. While this difference between the teaser rate and post-teaser rate might seem small, it had significant implications on financially unstable households.

Subprime Mortgage Rates: Teaser Rates and ARMs

| Year of Origination | 1-Year Prime ARM | Teaser Rate | Post-Teaser Rate |

|---|---|---|---|

| 2004 | 3.9% | 7.3% | 11.5% |

| 2005 | 4.5% | 7.5% | 10.5% |

| 2006 | 5.5% | 8.5% | 9.1% |

| 2007 | 5.7% | 8.6% | 9.1% |

Source: Federal Reserve Bank of Boston

The problem was exacerbated by the fact that many lenders did not properly vet borrowers' ability to repay the loans, and then used the proceeds from MBS sales to investors to lend out even more subprime loans.

High demand for mortgage-backed securities prompted banks to loosen lending requirements in an effort to fill this demand, and this went as far as lending out mortgages to borrowers with “no income, no job, and no assets” - also known as NINJA mortgage loans.

How Common Were Subprime Mortgages?

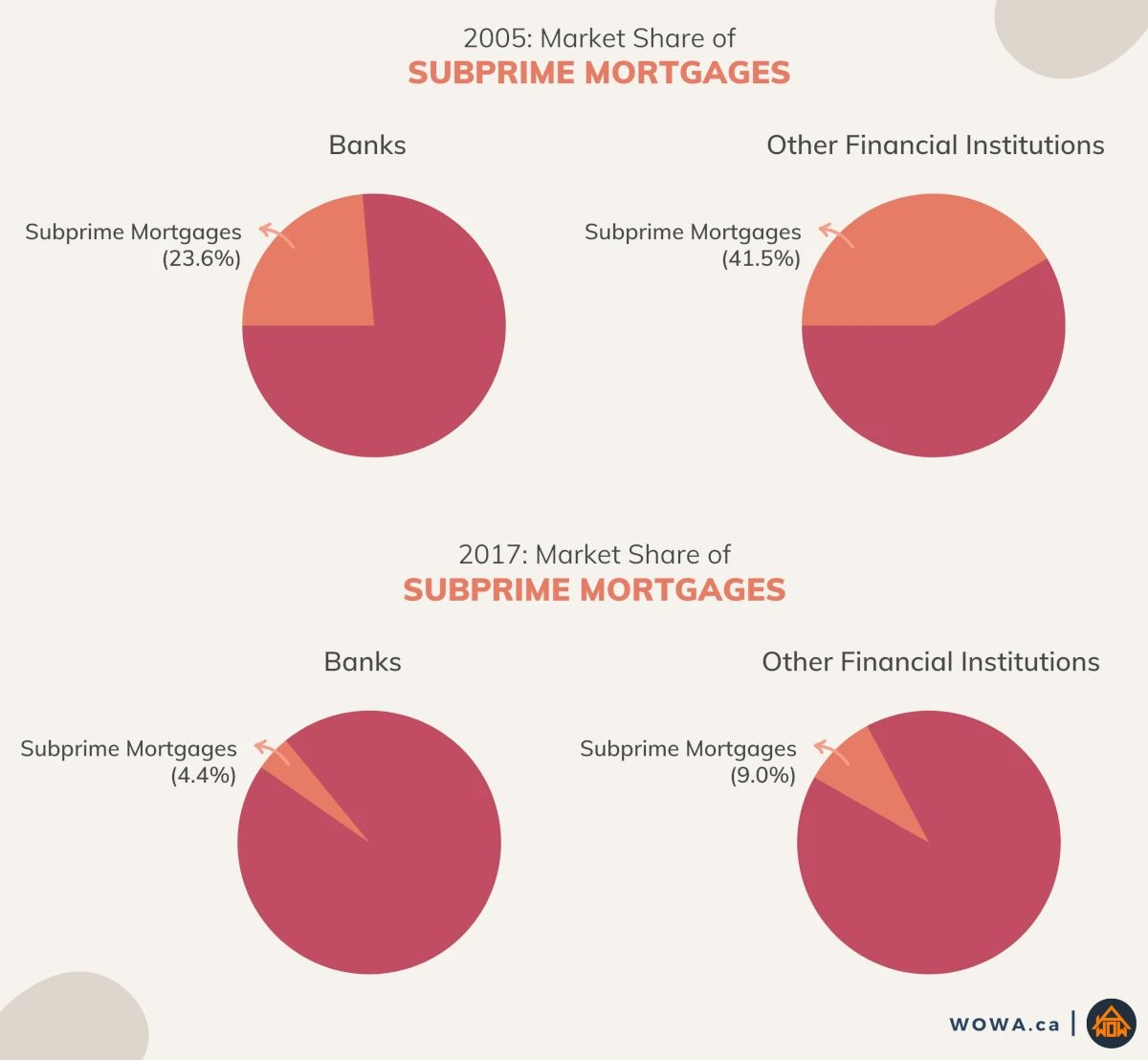

Subprime mortgages made up almost a third of all mortgage originations in 2005, with 23.6% of all mortgages originated by banks in 2005 being a subprime mortgage. This figure is higher for other financial institutions, where subprime mortgages made up 41.5% of their originated mortgages. Credit unions had a muted role in the subprime mortgage industry, with only 3.6% of credit union mortgages being subprime. After the financial crisis, subprime mortgage originations became much more limited.

Subprime Mortgage Originations (% of Mortgages)

| Year of Origination | Banks | Other Financial Institutions | Credit Unions |

|---|---|---|---|

| 2004 | 9.7% | 26.5% | 3.6% |

| 2005 | 23.6% | 41.5% | 3.6% |

| 2017 | 4.4% | 9.0% | 4.6% |

Source: Credit Union National Association (CUNA)

The prevalence of subprime mortgages also depended on the region and property type. For example, 14.8% of all homes purchased in Massachusetts in 2005 were bought using subprime mortgages. However, 32.6% of all multi-family home purchases were with a subprime mortgage, but only 13.2% of single-family home purchases were with a subprime mortgage.

Homes Purchased with a Subprime Mortgage in Massachusetts

| Property Type | 1999 | 2000 | 2001 | 2002 |

|---|---|---|---|---|

| Single-Family | 2.3% | 2.3% | 2.6% | 3.5% |

| Condo | 2.2% | 2.1% | 2.2% | 2.5% |

| Multi-Family | 4.2% | 4.6% | 6.4% | 9.4% |

| All Homes | 2.5% | 2.5% | 3% | 4% |

| Property Type | 2003 | 2004 | 2005 | 2006 | 2007 |

|---|---|---|---|---|---|

| Single-Family | 5.9% | 8.6% | 13.2% | 11.4% | 2.6% |

| Condo | 4.3% | 6% | 10.7% | 10.7% | 3.4% |

| Multi-Family | 18% | 26.4% | 32.6% | 28.6% | 5.8% |

| All Homes | 7% | 10.1% | 14.8% | 13.1% | 3.1% |

Source: Federal Reserve Bank of Boston

The Fallout of the Subprime Mortgage Crisis

When the housing bubble started to deflate and home prices tumbled, many people who took out subprime mortgages were unable to keep up with their payments and ended up losing their homes to foreclosure. As foreclosures increased, so did the number of vacant properties. This led to further declines in property values, which caused even more people to default on their mortgages. The result was a vicious cycle that contributed to the worst housing market crash in the United States since the Great Depression, and it had far reaching impacts around the world.

Surprisingly, a sizable percentage of borrowers that defaulted on their mortgage in 2006 and 2007 initially purchased their home with a prime mortgage, yet later refinanced and defaulted on a subprime mortgage. This leans into the fact that 30% of homes that would eventually be foreclosed were purchased with subprime mortgages, yet subprime mortgages made up 45.2% of all defaulted mortgages between 2006 and 2007. In other words, it wasn’t uncommon for even prime borrowers to get a subprime refinance, which eventually resulted in financial hardship.

Property and Mortgage Type (% of Foreclosures)

Foreclosures in the State of Massachusetts (2006-2007)

Comparing Property and Mortgage Type (% of Foreclosures)

Foreclosures in the State of Massachusetts (2006-2007)

| Mortgage | Property Type | % of Foreclosures | |

|---|---|---|---|

| Prime | Single-Family | 44.1% | 70% |

| Condo | 9.7% | ||

| Multi-Family | 16.2% | ||

| Subprime | Single-Family | 14.2% | 30% |

| Condo | 3.6% | ||

| Multi-Family | 12.2% | ||

Source: Federal Reserve Bank of Boston

Comparing Subprime Purchase Mortgages vs. Defaulted Mortgages

| Property Type | Subprime Purchase Mortgages (% of Foreclosed Homes) | Subprime Mortgages (% of Defaulted Mortgages) |

|---|---|---|

| Single-Family | 24.3% | 42.2% |

| Condo | 27.3% | 40.1% |

| Multi-Family | 43.0% | 53.3% |

| All Homes | 30.0% | 45.2% |

Source: Federal Reserve Bank of Boston

Reforms after the subprime mortgage crisis included the Dodd-Frank Wall Street Reform and Consumer Protection Act. This act made it more difficult for people with poor credit to get mortgages. It also created the Consumer Financial Protection Bureau (CFPB), and put stricter regulations on the banking industry. For example, no documentation (no doc) mortgages are no longer allowed in the United States, as borrowers must provide proof of income. Interestingly, no doc mortgages are still allowed in Canada for self-employed borrowers.

Canada During the Subprime Financial Crisis

Canada walked away from the subprime financial crisis relatively unscathed compared to the United States, and this was thanks to Canada’s relatively more stringent mortgage regulations. This made Canada's housing market and economy less vulnerable, versus loosening standards for subprime mortgages in the United States.

A commentary from the Federal Reserve Bank of Cleveland found that the mortgage loan-to-value (LTV) ratios in Canada were lower on average compared to the United States. As an example, 12% of U.S. mortgages had an LTV above 90% in the runup to the financial crisis, while only 6% of Canadian mortgages had an LTV above 90%. In fact, the median LTV of new subprime mortgages in the United States in 2005 was 100%!

Looking at all mortgages, over 5% of prime and subprime mortgages in the United States had an LTV ratio of 100% or more. This means that 5% of mortgages were underwater, where they owed more money than the home was worth!

Comparing Canadian vs. U.S. Mortgages by LTV Ratio

| United States | Canada | |||

|---|---|---|---|---|

| LTV Ratio | 1999 | 2005 | 2007 | 2006 |

| 0% - 80% | 76.48% | 79.14% | 78.12% | 84.79% |

| 80% - 90% | 10.55% | 8.98% | 9.66% | 8.81% |

| 90% to 100% | 7.56% | 6.37% | 6.93% | 1.53% |

| 100% or higher | 5.41% | 5.51% | 5.28% | 4.87% |

Source: Federal Reserve Bank of Cleveland

Subprime Mortgages Today

Despite the role that subprime mortgages played in the housing market crash, they can still be a useful tool for people with poor or limited credit histories, along with other situations that might result in a denial from a bank. When used responsibly, subprime mortgages can help people buy homes that they otherwise would not have been able to afford, giving them a start to homeownership as they rebuild their credit. However, it is important to remember that subprime mortgages come with higher interest rates and greater risks.

The eventual goal for subprime borrowers would be to qualify for a mortgage from an A lender with a lower interest rate. If you are considering a subprime mortgage, make sure you understand the risks involved and that you have a strong plan in place to shore up your finances.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.