The Complete Guide to Car Title Loans in Canada

What You Should Know

- Car title loans are short-term loans that allow you to get a loan using your car as collateral.

- To get a car title loan, you typically must own your car outright (no loan or lien).

- Interest rates and fees are usually very high, and therefore, car title loans are often best used as a last resort.

- If you frequently miss payments on your car title loan, your lender may seize your vehicle.

What Is a Car Title Loan?

Car title loans are short-term loans that use your car equity as collateral. Such loans provide fast access to cash, often with minimal paperwork. Many lenders don’t even require a credit check, making it easier for borrowers with poor credit to qualify.

Car title loans should not be confused with car loans. Car loans allow you to buy a vehicle using a loan, while a car title loan allows you to borrow against a vehicle you already own.

If you fail to make payments on time, the lender can seize and sell your car to recoup their losses.

Car Title Loan Lenders in Canada

| Lender | Loan Amount | Interest Rate (APR) | Funding Time |

|---|---|---|---|

| Canada Car Cash | $1,500 – $100,000 | Up to 35% | Same Day |

| Canada Loan Shop | Up to $65,000 | Up to 35% | Same Day |

| Snap Car Cash | $1,000 – $50,000 | 7.5% – 29% | Same Day |

| Get Loan Approved | Up to $50,000 | 8% – 29% | Same Day |

| Car Title Loans Canada | Up to $25,000 | Up to 35% | Same Day |

| Pit Stop Loans | $1,000 – $25,000 | Up to 35% | Same Day |

| Prudent Financial (Ontario) | Up to $50,000 | Up to 35% | From 30 minutes |

| Fast Action Finance (Ontario) | Up to $25,000 | Up to 35% | Same Day |

Key Features of Car Title Loans

Car title loans, also known as auto title loans, are a type of secured loan that uses an individual's car as collateral. They often provide borrowers with funding within hours. Typically, lenders want the car to be fully paid off and be no older than six to eight years.

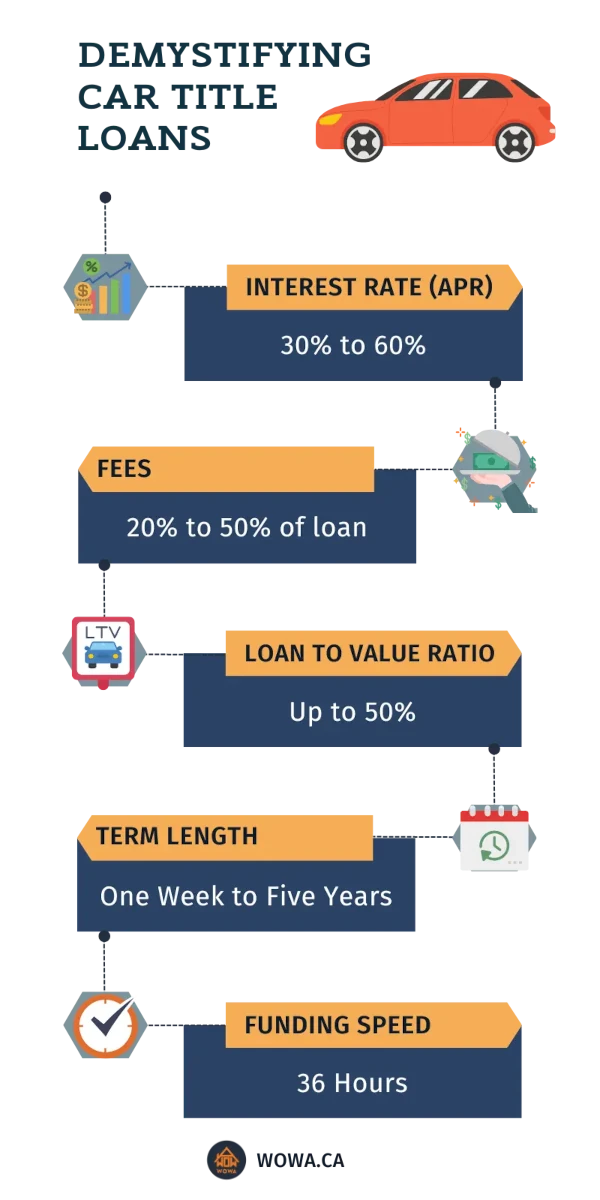

- High Interest Rates: High interest rates with APRs up to 35%.

- Fees and Upfront Charges: You may need to pay application fees, origination fees, vehicle evaluation fees and more.

- Loan Amount: The loan amount is often up to 50% of the car’s value, with maximum limits often between $25,000 and $50,000.

- Term Lengths: Typical term lengths are 3 months to 3 years, with some lenders offering from 15 days up to 5 years.

- Same-Day Funding: Some lenders can approve and fund a loan the same day, though timing depends on your documents, vehicle appraisal, and the lender’s process.

- GPS Tracker: Some lenders may require a GPS device to be installed in the vehicle to help locate it if payments are missed, and an ignition immobilizer to shut off your car remotely. Ask about any installation, rental, or removal fees.

- Car Insurance: Lenders may require proof of valid auto insurance and may ask for comprehensive coverage while the loan is outstanding.

- Vehicle Lien: The lender typically registers a lien against your vehicle, which can limit your ability to sell or refinance the car until the loan is repaid.

- Repayment: Loan payments are often made through pre-authorized debit.

- Vehicle Seizure: The lender may seize your vehicle if you fail to make payments.

Car Title Loan Interest Rates and APR

Car title loans in Canada are among the most expensive ways to borrow. As of January 1, 2025, the Canadian government officially lowered the criminal rate of interest to an Annual Percentage Rate (APR) of 35%.

Before this change, lenders could charge an Effective Annual Rate (EAR) of up to 60% (roughly 48% APR). While the 35% cap provides more protection, it remains significantly higher than traditional secured loans (like a standard auto loan or a home equity line).

Important Note: Always confirm if the rate quoted is the APR. Some lenders may quote a "monthly rate" or a "base interest rate" that excludes mandatory fees. Under Canadian law, the APR must reflect the total cost of borrowing, including interest and most fees.

Fees to Watch For

Each car title loan lender charges fees at the time of loan origination. These fees are often significant and are not included in the interest rate; therefore, it is important to check the APR, which is the true cost of borrowing. Fees may be as high as 20% to 50% of the loan amount. Lenders may charge lower interest rates to draw customers and reveal the higher fees later in the application process.

Using an APR calculator will help you compare the true cost of borrowing for different lenders. Common types of fees may include:

- Application Fees: This fee helps to defray the cost of processing an application.

- Origination Fees: This one-time fee compensates the lender for their work in arranging and processing your loan.

- Processing Fees: Some lenders charge a processing fee to cover the cost of additional paperwork or other associated expenses.

- Vehicle Evaluation/Appraisal Fee: Fees to cover the cost of vehicle inspection to get its value appraised by a professional.

- Search Fee: Fee to search public records of the car to check for existing liens or accident history.

- Late Payment Fees: If you miss a payment, you may be charged this additional fee to cover the lender's costs.

Before signing a car title loan, ask about all fees and read the contract carefully. Clarifying the terms upfront can reduce risk and help you make an informed decision.

How to Avoid Car Title Loan Lender Tricks

Some lenders may use tricks that could mislead the general public. While some lenders offer reasonable interest rates, many have high fees and expensive payments. These are some things to be aware of:

- Quoting Monthly Rates: Monthly rates are much lower than annual rates, and quoting them can mislead a borrower. Borrowers must beware of rates under 5%.

- Hiding Fees Until the End: Some lenders wait until you are deep in the application process before revealing administrative fees.

- Directing Attention to the Monthly Payment: Lenders may offer lower monthly payments by stretching the loan over many years. While the monthly cost feels manageable, the total interest paid over time will be much higher.

Borrowing Limits and Terms

How Much You Can Borrow

Most lenders allow a maximum loan-to-value ratio (LTV) of 50% for car title loans, meaning you can't borrow more than 50% of your car's value.

- Example: If your car is worth $20,000, your maximum loan would be $10,000.

- Factors: Lenders prefer newer, low-mileage vehicles because they act as better collateral.

Lenders typically also have a limit to how much they can lend, with ceilings often ranging from $25,000 to $50,000.

Loan Terms and Term Lengths

Term lengths for car title loans typically range from 3 months to 3 years, though some short-term options exist for 30 days. Terms vary by lender, and some may offer up to six years for more creditworthy borrowers.

If you only need a small amount of money for a short period, then opt for a shorter length to keep your total interest as low as possible. However, if you need a more significant sum, a longer term may be better to decrease the monthly payment.

Additionally, you'll want to ask your lender if the loan is open or closed.

- An open loan will allow you to prepay without penalties. However, closed loans have penalties.

- With a closed loan, you could be stuck in a high-interest loan to avoid excessive fees.

As a result, an open loan is better if you expect to improve your financial situation shortly. This is because you can refinance into a lower-interest-rate loan.

Getting Approved: Application & Documents

Applying for a car title loan is designed to be a fast, straightforward process. You can typically complete the application in person at a local branch or entirely online from your home.

Application Process

- Gather Your Documents: Gather all the personal and vehicle documents listed below.

- Submit Your Info: Pick a lender and provide the documents required.

- Review & Verification: A representative will review your application and contact you to verify your details.

- Appraisal: The lender will conduct a vehicle inspection. If you are applying online, you may be asked to submit clear photos of the car’s exterior, interior, VIN, and odometer.

- Review the Offer: Once approved, the lender will provide a loan offer.

Documents Required

To ensure your application is processed without delays (often in less than 24 hours), have the following documents ready:

| Document Type | Examples & Details | Why Lenders Need It |

|---|---|---|

| Proof of Identity | Valid Driver’s License or Passport (must be government-issued). | Verify your legal age and check that your name matches the vehicle title. |

| Proof of Address | Utility bill, lease agreement, or a recent bank statement. | Confirm your provincial residency where the loan is being issued. |

| Proof of Income | Recent pay stubs, employment letter, or benefit statements (CPP, ODSP, EI). | Ensure you have a steady monthly cash flow. |

| Vehicle Ownership (Title) | The physical "Title" or "Vehicle Permit" (must be in your name). | Prove you own the car without any existing loans or liens. |

| Registration & VIN | Current provincial registration and your 17-digit VIN. | Verify the car is legally roadworthy and check for past accident history. |

| Vehicle Details | Year, Make, Model, and current Odometer reading (Mileage). | Determine the wholesale value of the car, which sets your borrowing limit. |

| Proof of Insurance | Valid insurance card (often requires Comprehensive/Collision). | Protect the lender's collateral in case the vehicle is stolen or totalled. |

| Banking Info | A void cheque or a direct deposit/PAD form. | Deposit your funds quickly and set up automatic monthly repayments. |

Other items that may be requested:

- Recent Photos of the Vehicle (or an in-person inspection)

- Second Set of Keys (some lenders request this)

Approval and Funding Timeline

Many car title loan lenders offer fast processing in less than 24 hours. However, some may take up to 72 hours, depending on the complexity of your application. For example, you may be required to provide additional information or documentation if the lender needs to verify your income and creditworthiness before approving a loan amount.

Repayment & Lien Removal

How Repayments Work

In most cases, the lender will deduct payments from your bank account through pre-authorized debits (PAD).

- Payment Schedules: Payments are typically monthly, but some lenders offer weekly or bi-weekly options to align with your payday.

- NSF Risk: If your account has insufficient funds, you will likely be hit with a Non-Sufficient Funds (NSF) fee from your bank and potentially from the lender. If you are aware of a funds shortage, you can request the lender to delay the payment.

- Early Payoff: If you have an open loan, you can pay off the entire balance at any time to save on interest.

Lien Registration on Your Vehicle

When you sign your loan agreement, the lender registers a lien against your vehicle in a provincial registry (like the PPSA in Ontario or the RDPRM in Quebec), which gives them the right to repossess the vehicle if you default on your loan payments. Thus, making loan payments is essential to ensure your vehicle is not seized.

Insurance Requirements: Because of the lien, most lenders require you to maintain full coverage (Collision and Comprehensive) insurance so their collateral is protected in case of an accident.

Getting Your Title Back (Lien Discharge)

Once your final payment is processed and your balance reaches $0, you must ensure the lien is removed.

- Lien Release Letter: The lender is legally obligated to send you a "Release of Interest" or "Lien Discharge" letter. This could take 7–10 business days after the final payment clears.

- Verification: You can verify the lien has been removed by conducting a provincial lien search or using a service like CARFAX Canada.

- Notify Insurance: Once you have the release letter, send a copy to your auto insurance company. This could help lower your premiums or adjust your coverage now that a lienholder is no longer listed on the policy.

Pros and Cons of Car Title Loans

Pros of Car Title Loans

Car title loans offer a few benefits. For car owners, it can provide an invaluable lifeline in times of financial hardship. Often, the approval process is rapid and requires minimal paperwork. Some advantages include the following:

- Quick Access to Cash: Car title loans can be approved in just a few hours or a few days, so you don't have to wait long before getting your money.

- May Not Need Credit Checks: Some lenders do not require a credit check when approving a car title loan, making it easier to get the funding you need, even if you have a low credit score.

- High Approval Rates: Car title loans are assessed on a case-by-case basis. Lenders try to work with you for approval.

Cons of Car Title Loans

While there are some advantages of car title loans, there are also a few downsides. Some downsides include the following:

- High Interest Rates: Car title loan APRs in Canada can range up to 35%, significantly higher than most other types of loans.

- Complete Ownership Required: Most lenders require you to own your car outright. This means no existing car loans or liens are allowed. If you have an existing car loan, you could still borrow money with a car equity loan.

- Hidden Fees: There may be additional charges not clearly stated in the agreement, so it's essential to read the fine print carefully.

- Repossession Risk: If you default on your payments, you may lose your car to the lender.

Alternatives to Car Title Loans

The following alternatives may offer a lower interest rate and better terms than car title loans.

Personal Loans

Personal loans allow you to borrow at interest rates starting from around 6%. Most banks and credit unions in Canada offer personal loans, but the approval is tougher.

Home Equity Loans

Home equity loans are loans against your home’s equity. They take longer to process, and you can expect up to two weeks for approval and funding. There are different types of home equity loans, such as home equity lines of credit (heloc), second mortgage, cash-out refinance and reverse mortgage.

Credit Cards

Canadian credit cards typically have interest rates ranging between 12.99% - 19.99%. You can also withdraw cash using a cash advance. The main downside is that your credit limit may not be as high as a car title loan. There are various types of credit cards to meet all kinds of demands, such as bad credit, balance transfer (low interest rate for a few months) and instant approval.

Frequently Asked Questions

Yes, you remain the registered owner and keep possession of your vehicle. However, the lender becomes a lienholder. This means they have a legally secured interest in the car. While you continue to drive the vehicle, the lender holds your title (or a registered interest in the provincial database) as collateral. If you default on your payments, the lender has the legal right to repossess and sell the vehicle to recover the debt.

Most traditional car title lenders require you to own your vehicle "free and clear," meaning it must be fully paid off with no existing loans. However, if your car is still being financed but has a high market value, you may qualify for a Car Equity Loan. In this scenario, a lender may offer you a "second lien" loan based on the difference between what the car is worth and what you still owe. Note that these are harder to find and often come with stricter requirements.

Yes. One of the primary reasons Canadians choose car title loans is that they are asset-based, not credit-based. Because the loan is secured by the value of your vehicle, lenders are far more concerned with the car’s condition and your ability to make monthly payments than your credit score. Even with a history of bankruptcy or low credit, you can typically get approved as long as you have sufficient equity in your vehicle and a stable source of income.

Many car title lenders in Canada require a GPS tracking device or an ignition immobilizer (a device that can remotely prevent the car from starting) to be installed. Under Canadian privacy laws (PIPEDA), lenders must obtain your explicit consent before installing these devices.

Yes. Because car title loans are secured by the vehicle’s value, lenders are often more flexible with income types than traditional banks. Most lenders will accept non-employment income, including:

- Canada Pension Plan (CPP) or private pensions.

- Old Age Security (OAS).

- Employment Insurance (EI).

- Provincial disability benefits (like ODSP in Ontario or AISH in Alberta). As long as you can prove you have a steady monthly deposit to cover the payments, you are likely to qualify.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.