Construction Loans in Canada

What You Should Know

- Construction loans allow you to finance building a new property—including custom, spec, or modular homes—as well as undertaking major structural renovations.

- To qualify, you generally need a credit score of 680 or higher, a down payment (or sufficient land equity), and detailed, professional construction plans and budgets.

- You do not receive the total loan value upfront. Instead, funds are released in stages (draws) only after a third-party appraiser verifies that specific building milestones have been met.

- Because financing an uncompleted property carries more risk for lenders than buying an existing house, construction mortgage rates are typically higher than conventional mortgage rates.

Whether you are a Canadian homebuyer looking to build your dream home or a real estate investor planning your next property from scratch, traditional financing won't work. Because the building doesn't exist yet, you need a specialized financial tool: a construction loan.

What is a Construction Loan?

A construction loan is a short-term financing product designed specifically to fund the construction of a new residential property or a substantial structural renovation. It provides the capital required to secure a plot of land, design a house, and pay for the physical build from the ground up.

How It Differs From a Conventional Mortgage

The biggest difference between the two products is how the funds are distributed:

- Conventional Mortgages: The lender releases a single, one-time lump sum on closing day to purchase an already-completed home.

- Construction Loans: The lender disburses funds progressively in stages—known as draws—as the building project advances.

Instead of handing over all the cash upfront, this milestone-based method ensures that money is systematically released exactly when your project needs it most to cover critical phases like excavation, pouring the foundation, framing, and roofing.

This guide will walk you through everything you need to know about navigating construction loans in Canada, from how the draw process works to application requirements and expert tips for securing approval.

Eligibility Criteria for Obtaining a Construction Loan

Similar to a down payment made for a conventional mortgage, construction loans may require you to put money up front to pay for construction expenses. However, unlike conventional mortgages, the collateral for a construction home is an unfinished home. Construction loans are riskier for lenders because they have a lower value and are more difficult to sell than a finished home. To see whether you can afford the construction loan, and eventually afford a mortgage, your lender will look at your income, debt levels, and credit score. Securing a construction loan involves stringent criteria to mitigate risks for the lender. Here's what a construction loan lender would look at:

Creditworthiness

Your credit score plays a crucial role in securing a construction loan. Most lenders in Canada require a minimum credit score of 680, with the minimum requirement possibly being 700 or higher, depending on the lender. Higher scores can secure better terms and lower interest rates, reflecting your reliability as a borrower.

Required Documentation

To qualify for a construction loan, you'll need more than just good credit. Lenders require detailed construction plans, a well-prepared budget, and a timeline for project completion. These documents help the lender assess the feasibility of your project and its financial requirements.

Financial Stability

Lenders will scrutinize your financial stability, including income verification, employment history, and existing debts. They want to see proof of sufficient income to cover both the interest payments during construction and eventual mortgage payments upon project completion.

Applying for and Securing a Construction Loan

Applying for a construction loan is more complex than a traditional mortgage, but understanding the steps can simplify the process.

Step-by-Step Application Process

- Project Planning: Before approaching lenders, have a detailed construction plan, budget, and timeline in place.

- Choose a Lender: Research and select lenders experienced in construction loans.

- Submit Application: Submit necessary documents, including construction plans, financial statements, and credit information.

- Appraisal and Approval: The lender will appraise the project’s feasibility and assess your financial stability before approving the loan.

Disbursement of Funds

Funds are typically disbursed in stages, known as "draws," corresponding to the completion of various construction phases. Each draw requires inspection and approval from the lender to ensure the project is progressing as planned.

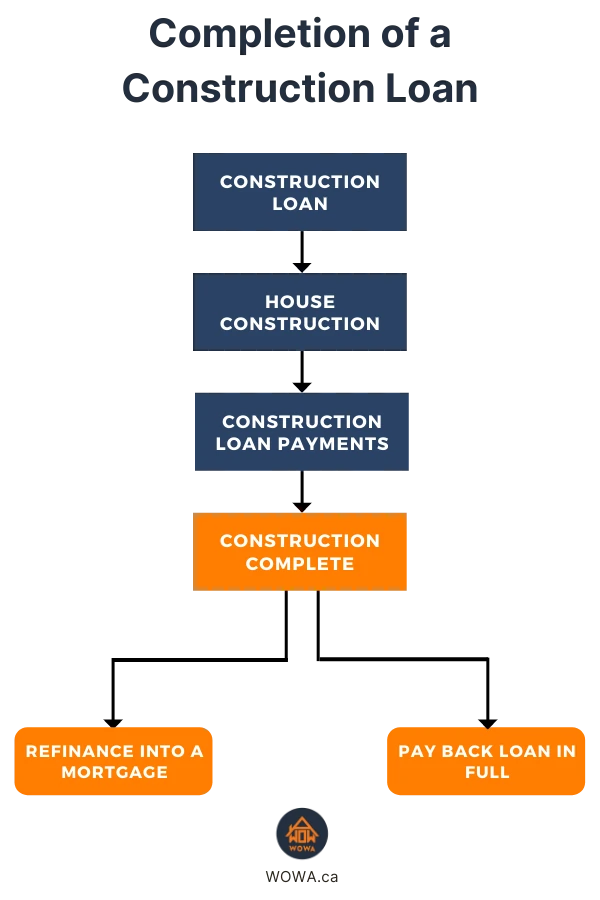

Converting to a Permanent Mortgage

Once construction is complete, the construction loan typically converts to a standard mortgage. The terms of this mortgage would generally be agreed upon beforehand. This allows for a smooth transition from construction financing to long-term homeownership or investment property holding.

Why Choose a Construction Loan over a Traditional Mortgage?

Home construction loans differ from regular mortgages in the loan term and when you receive access to the loan. Construction loans are meant to be a short-term way for you to finance your new home construction. On the other hand, mortgages apply to existing homes, can have longer terms, and have lower mortgage interest rates.

Construction loans offer the flexibility that traditional mortgages lack. They are structured to meet the specific needs of a construction project, offering incremental disbursements rather than a one-time, upfront payment. This model helps borrowers ensure funds are available when needed, with borrowers only paying interest to borrow money when they need it.

Most construction loan agreements allow borrowers to make interest-only payments during the construction phase. This can ease the financial burden during the months when borrowers are paying for building materials and labour.

Comparing Construction Loans & Conventional Mortgages

| Construction Loans | Commercial Mortgage | Residential Insured Mortgage | |

|---|---|---|---|

| Maximum Amortization Period | Non-Amortizing | 40 years | 25 years |

| Interest Rates | Highest | Medium | Lowest |

| Maximum LTV | 75% | 85% | 95% |

| Draw Schedule | Typically 3 to 5 progress draws. | One-time lump sum | One-time lump sum |

| Approval Criteria | Detailed construction plans & borrower’s financials | Property income generation & borrower's financials | Borrower’s financials |

How Do New Construction Loans Work?

A construction loan—frequently called a draw mortgage—is a specialized financing product designed for building a home from the ground up. Unlike a conventional mortgage that releases a lump sum all at once on closing day, a draw mortgage releases funds in increments (or “draws”) as major building milestones are completed.

How the Draw Process Works

To manage risk, lenders do not provide the money upfront. Instead, a construction loan operates on a backward-looking schedule:

- Proportional Payouts: Funds are advanced only for work that has already been completed and verified by a physical inspection from a third-party appraiser.

- The Legal Process: In Canada, lenders typically advance draw funds directly to your real estate lawyer. Your lawyer is responsible for verifying that no construction liens have been placed on the property and managing statutory holdbacks before releasing the cash to your builder.

Budgeting and Approval Requirements

Because a bank is financing an asset that doesn't exist yet, its approval process is rigorous. Lenders require a blueprint, a construction contract, and a highly realistic, itemized budget.

To ensure approval, you must work with your contractor to secure an accurate, all-inclusive cost breakdown. General home building cost estimates or unverified DIY projections will cause lenders to reject the application.

Financing Limits: The 75% Rule

Most conventional lenders will finance up to 75% of the project's total value.

⚠️ Key Nuance: This 75% limit is calculated against the “as-completed” appraised value (what the home and land will be worth when finished), not just the raw cost of materials and labor. Furthermore, if you already own the land, the equity in that land can often count toward your 25% down payment, significantly reducing the amount of cash you need to provide out of pocket.

Self-Build Construction Loans

If you plan to act as your own general contractor rather than hiring a licensed, professional home builder, you will need a specialized self-build construction loan. Because owner-built projects have a statistically higher rate of budget overruns and delays, lenders are highly cautious. To qualify, you must formally demonstrate to the lender that you have the licensed expertise or professional construction management experience required to pull the project off.

Financing Multi-Unit & '4+1' Properties

When a property crosses the threshold from a 4-unit building to a 5-unit building (often referred to as a '4+1' property), it transitions from a standard residential mortgage into the territory of commercial multi-unit financing.

Lenders and the Canada Mortgage and Housing Corporation (CMHC) have introduced aggressive programs specifically to incentivize this type of high-density construction:

CMHC Apartment Construction Loan Program (ACLP)

For projects featuring 5 or more units, developers can bypass traditional, restrictive bank construction financing (which typically caps out at 65%–75% Loan-to-Cost).

- Up to 100% LTC: Following recent federal expansions, the ACLP provides low-interest construction financing covering up to 100% of the building costs.

- Below-Market Rates: Construction-period interest rates under this program are subsidized and typically sit 0.5% to 1.5% lower than conventional private construction loans.

- Amortization: Seamlessly transitions from a construction loan into permanent financing with amortization periods extending up to 50 years.

CMHC MLI Select

If your 4+1 multi-unit build commits to specific targets regarding affordability, energy efficiency, or accessibility, you can unlock preferred underwriting terms through CMHC's MLI Select point system. This program drastically reduces mortgage insurance premiums and lowers the equity requirements needed to break ground.

Construction Draw Schedules

A construction draw schedule outlines when construction draws are paid. The contractor negotiates a draw schedule before construction begins. While the bank might already have a standardized draw schedule, your contractor or the bank's appraiser may propose alternate payment schedules. This can be due to differing construction timelines or costs. Construction draw schedules can be based on milestones, such as when the foundation or roof is complete or a general percentage of the total home finished.

Interest only starts incurring once each construction draw is disbursed. As a borrower, you may want to receive draws as late as possible to reduce interest costs during construction. On the other hand, the contractor would want to receive their pay as early as possible. If your contractor or lender proposes an alternative payment schedule, you should review it to ensure that it allows your contractor to be paid on time, but is also reasonable.

Example of a Construction Draw Schedule

| Funding Stage | Project Phase | % Complete | Disbursement Details |

|---|---|---|---|

| Initial Advance | Land Purchase (Optional) | 0% | Up to 65%–75% of the land value is advanced (if the land is not already owned). |

| Draw 1 | Foundation & Framing | ~15%–20% | Funds are advanced once excavation is done, the foundation is poured, and subflooring is secure. |

| Draw 2 | Roof-Tight / Lock-Up | ~50% | Funds are advanced once the roof, windows, doors, and exterior siding protect the structure from weather. |

| Draw 3 | Drywall & Rough-ins | ~75% | Funds are advanced once plumbing, electrical, and HVAC are roughed in and drywall is taped. |

| Draw 4 | Final Completion | 100% | The remaining funds are released for occupancy, minus the provincial statutory lien holdback (typically held for 45 to 60 days depending on the province). |

Example Home Completion Schedule

| Work Completed | % of Total | Running Total (Cumulative Progress) |

|---|---|---|

| Excavation, Site Prep & Permits | 3.0% | 3.0% |

| Foundation & Footings | 10.0% | 13.0% |

| Framing & Structural Sheathing | 18.0% | 31.0% |

| Roofing & Waterproofing | 4.0% | 35.0% (Roof-Tight Milestone) |

| Windows & Exterior Doors | 4.0% | 39.0% |

| Exterior Siding / Masonry | 7.0% | 46.0% |

| HVAC & Ductwork (Rough-in) | 4.0% | 50.0% |

| Plumbing (Rough-in) | 6.0% | 56.0% |

| Electrical (Rough-in) | 6.0% | 62.0% |

| Insulation & Vapor Barrier | 3.0% | 65.0% (Lock-Up Milestone) |

| Drywall (Hang, Tape & Texture) | 8.0% | 73.0% |

| Painting (Interior & Exterior) | 4.0% | 77.0% |

| Flooring & Tiling | 6.0% | 83.0% |

| Cabinets, Countertops & Trim | 12.0% | 95.0% |

| Final Electrical, Plumbing & Cleanup | 5.0% | 100.0% (Final Completion) |

| Total | 100% |

How many construction draws can I receive?

Standard progress draw mortgages in Canada typically feature 3 to 5 draws. The exact number depends on your lender, the size of your project, and whether you already own the land.

- 3-Draw Schedule: Common for smaller projects or modular home builds.

- 4-Draw Schedule: The standard framework for most traditional custom home builds.

- 5+ Draws: Often permitted by specialized or private lenders for large-scale, high-budget custom estates to help the builder maintain cash flow.

Benefits and Drawbacks of Using a Construction Loan

While construction loans offer unique advantages, they also have potential drawbacks.

Benefits

Customization: Construction loans allow for customizing homes or properties from scratch to meet specific needs and preferences rather than buying a pre-built home.

Control Over Quality: Direct involvement in the construction process ensures better control over the quality of materials and workmanship.

Financial Flexibility: Interest-only payments during construction ease the financial burden until the project is complete.

Drawbacks

Complexity: The application process for construction loans is more complex and time-consuming than traditional mortgages.

Higher Interest Rates: Construction loans often come with higher interest rates compared to standard mortgages.

Inspection Requirements: Frequent inspections by the lender can slow down the construction process and add additional layers of bureaucracy.

Examples of Using Construction Loans

Homebuyers in Vancouver

Sarah and John wanted to build their dream home in Vancouver. Unable to find a pre-built house that met their needs, they opted for a construction loan. With detailed planning and a reputable builder, they secured the loan, managed the disbursements efficiently, and successfully moved into their custom-built home within a year.

Real Estate Investors in Toronto

A group of investors in Toronto aimed to construct a multi-unit rental property. They used a construction loan to finance the project, leveraging the phased disbursement to manage cash flow effectively. The project was completed on time and within budget, resulting in a highly profitable investment.

Tips for Homebuyers and Real Estate Investors

Do Your Homework

Before applying, research multiple lenders to compare terms, interest rates, and fees. Understanding the nuances of each lender’s offerings can save you time and money.

Hire Experienced Professionals

Engage a reputable builder and, if possible, a construction consultant. Their expertise can help you avoid costly mistakes and ensure the project stays on track.

Keep a Contingency Fund

Despite planning, unexpected costs do arise. Having a contingency fund of 10-15% of the total project cost can provide a financial cushion.

Construction Loan Financing Programs

Home Improvement Mortgages

A Purchase Plus Improvements mortgage lets you roll the cost of renovations into your mortgage at the time of purchase, so you can buy a home and finance upgrades to it with a single loan. This is useful when a property needs work — anything from new flooring or a kitchen update to more substantial renovations — that you'd rather not pay for in cash.

The amount you can add for improvements is capped. Depending on the mortgage default insurer, you can typically borrow up to 20% of the home's as-improved value (or 10% with CMHC), to a maximum of $40,000 — whichever is less. Lenders such as Meridian offer this type of financing. The improvement funds are not advanced upfront: your lender holds them back and releases them only after the work is completed and verified, so you'll need to cover the renovation costs in the interim (through savings or short-term credit) and be reimbursed on completion.

Because the improvements raise the property's value, your down payment is calculated on the higher, as-improved figure rather than the original purchase price. Specifically, the lending value is the lesser of the improved value of the property or the purchase price plus the improvement costs, and your minimum down payment is based on that amount.

CMHC Rental Construction Financing

If you are constructing multi-unit rental housing, you may qualify for funding from the Canada Mortgage and Housing Corporation. You can borrow up to 100% of construction costs, with a minimum loan of $1,000,000.

CMHC rental construction financing provides CMHC mortgage loan insurance for free. No CMHC premiums are required. CMHC financing is on a 10-year term with a fixed interest rate, for up to a 50-year amortization period. Only interest payments are required during construction.

The CMHC will charge you an application fee. The application fee is $200 per residential unit for the first 100 units, then $100 for each additional unit, up to a maximum fee of $55,000. For non-residential portions of a building, the fee is 0.3% of the loan amount for non-residential portions if the loan for it is over $100,000. The program is fully explained on CMHC’s webpage for the Apartment Construction Loan Program, which used to be called the Rental Construction Financing Initiative (RCFi).

CMHC Affordable Housing Fund

Previously called the National Housing Co-Investment Fund (NHCF), the Affordable Housing Fund is designed to finance the development of energy-efficient, accessible and socially inclusive housing throughout Canada. The housing can be for mixed-income, mixed-tenure and mixed-use affordable housing purposes. Builders can receive up to a 95% loan-to-cost through low-interest and forgivable loans.

The low-interest loans offer a 10-year fixed interest rate. You can also receive up to a 50-year amortization period. Projects with low cash flow are eligible to receive forgivable loans. However, they will not be prioritized for funding. You can learn more and apply to the program through CMHC’s Affordable Housing Fund.

Laneway House Mortgages

A laneway house is a small detached house built on the same lot of land as an existing house, usually facing a lane at the rear of the property. They help to gently increase density in existing residential neighbourhoods while increasing the range of rental housing options. Some lenders, such as Vancity and Equitable Bank, offer laneway house mortgages to finance the construction of a new laneway house. These mortgages may have relaxed eligibility requirements. For example, Equitable Bank’s laneway house mortgage can consider the potential rental income of the unit when calculating the borrower’s debt service ratio, making it easier to qualify.

Government Incentives for Gentle Densification

If you are a regular homeowner or an investor looking to add additional housing units to a smaller residential property (1 to 4 units), several new initiatives make construction financing significantly easier to obtain:

CMHC Refinance for Secondary Suites

Homeowners looking to build a self-contained secondary suite (such as a basement apartment, garden suite, or laneway coach house) can now access up to 90% Loan-to-Value (LTV) of the property's as-improved value.

- Progress Advances: Much like a standard construction loan, funds are advanced in up to 4 progressive draws to pay contractors as the suite is built.

- Extended Amortization: Allows up to a 30-year amortization period to keep monthly carrying costs affordable during and after construction.

CMHC Improvement Program

For purchasing a property that requires immediate, major structural construction to add units (up to a 4-plex), this program allows you to secure an insured mortgage covering up to 90% of the final, completed value of the 3-to-4 unit property.

Tax Rebates & Cost Savings

To spur the construction of new rental housing, the tax landscape for builders has shifted dramatically:

- Full GST Elimination on Purpose-Built Rentals: The federal government has eliminated the 5% GST on the construction of new multi-unit rental housing (buildings with 4+ or 5+ units depending on structure). This removes tens of thousands of dollars in upfront construction costs. The federal program requires a minimum of 4 residential units to successfully qualify for the full 5% GST rebate.

- Provincial HST Rollbacks: Multiple provinces (such as Ontario) have introduced matching legislation to temporarily remove the provincial portion of the HST on new residential builds up to certain values, allowing total tax savings of up to 13% for eligible projects.

- CMHC Eco Plus Premium Refund: If your new construction project meets specific green building or energy-efficiency standards, you can claim a 25% refund on your CMHC mortgage insurance premium after completion.

FAQs

Do I have to make monthly payments on construction loans?

You still have to make monthly payments on your construction loan, even if construction is ongoing and your home is not occupied. Some lenders, such as Meridian Credit Union, only require monthly interest-only payments during construction. You will be required to make principal and interest payments once construction is complete.

Some construction lenders may even allow you to use future construction draws to pay for interest on the loan.

Can I receive money to purchase land with a construction loan?

If you do not already own land to build on, your first construction draw would usually be used to purchase the land. This first draw can be paid in advance before construction starts and can be from 65% to 75% of the cost of the land. Not all lenders pay the first draw in advance. You might be expected to cover the vacant land purchase cost with your own money.

What happens to a construction loan when construction is complete?

Once construction of the home is completed, the construction loan would either need to be refinanced into a conventional mortgage or paid off in full.

Do contractors receive the full amount of construction advances?

Contractors do not receive the full amount of any construction draw. A construction holdback, required by a province's builders' lien legislation, withholds 10% from the payments you make to your general contractor. This holdback is released only after the province's lien period expires, provided no liens have been registered against your property.

The length of that period varies by province. Under British Columbia's Builders Lien Act, the holdback can generally be released 55 days after the certificate of substantial completion. Under Ontario's Construction Act (formerly the Construction Lien Act), lien claimants now have 60 days to preserve a lien. Alberta and other provinces have their own equivalent statutes and timelines, so the exact period — typically in the range of about 45 to 60 days — depends on where your project is located.

You may be asked to sign a Certificate of Substantial Completion, which is generally issued once the work is substantially performed — meaning the property can be used for its intended purpose and only a small percentage of the contract value remains to be completed (the exact threshold is set by a formula in each province's legislation). You do not have to sign this certificate if you are not satisfied with the contractor's work.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.