Tenant Insurance Companies in Canada

What You Should Know

- Tenant insurance protects your belongings and provides liability coverage for tenants and renters.

- Although not required by law in Canada, tenant insurance can be required by landlords as a condition of your lease.

- Tenant insurance usually costs between $20 and $50 per month in Canada.

- You can often get discounts and cheaper tenant insurance rates by bundling with auto insurance, being claims-free, having a higher deductible, and having safety systems installed in the home.

What is Tenant Insurance?

Even if you don't own the property you are renting, there is always a risk that something could happen to your belongings or that you could be held liable for damages or injuries. Tenant insurance, also called renter’s insurance or contents insurance, is designed to protect tenants and renters in case of damage to their belongings or personal liability for damages. Most tenant insurance policies usually cover up to $1 million in Canada, however, you can purchase additional add-ons to your policy to extend your coverage.

It is important to note that tenant insurance does not cover the actual structure of the rental property. That would be covered by landlord insurance, and it would be paid for by your landlord. Even though it can be an additional cost on top of your rent, tenant insurance is relatively affordable, especially when you consider the peace of mind it can provide. It can also give you coverage for things like temporary accommodations if your rental unit becomes uninhabitable due to a fire, flood, or other disaster.

With so many options available in Canada, it can be difficult for first-time renters and seasoned renters alike to understand what tenant insurance is. This page will help you understand the basics of tenant insurance so you can make the best decision for your needs. This page will also take a look at what tenant insurance covers, the different types of tenant insurance, how much tenant insurance usually costs, and comparing Canadian tenant insurance providers. Plus, we'll also take a look at tips to get cheaper tenant insurance in Canada.

Tenant Insurance Companies in Canada

There are many tenant insurance companies to choose from in Canada. To help you compare between them, we've found sample quotes for an example property in Toronto. The rates indicated below are for a 40-year old renter that is looking for tenants insurance for a $500,000 high-rise condo located in Toronto. They currently have home insurance coverage that has been continuously held for more than 10 years. They also have no prior claims in the past five years.

We also indicate tenant coverage options offered by each insurer, additional coverage that you can add-on, and potential discounts.

Insurance

Sample Quote: $34.56/month

As Canada’s biggest bank, RBC offers a variety of products, including tenant’s insurance. Tenant's insurance with RBC Insurance is underwritten by Aviva, similar to their car insurance products. RBC may require a deposit when you buy tenant insurance with them. Coverage that is included in RBC's Comprehensive Tenant Insurance Policy, besides personal belongings, liability, and loss-of-use, include coverage for your personal property at other locations and property in your vehicle. For example, if your laptop gets stolen while travelling, your tenant’s insurance may cover the cost!

The sample quote of $34.56 per month is based on the following:

- $1,000 deductible

- $1 million personal liability limit

- $35,000 personal property limit

- $14,000 additional living expenses

- $5,000 voluntary medical payments

- $1,000 voluntary property damage

- $20,000 sewer backup coverage

You can easily customize your quote online. For example, increasing your deductible from $1,000 to $2,000 will reduce your quote to $32.04 per month. Increasing your deductible even further to $5,000 will reduce your quote to $29.43 per month.

RBC Insurance offers personal liability coverage up to $5 million. Increasing your personal liability limit to $2 million will increase your quote to $35.73 per month, while a limit of up to $5 million will cost $36.90 per month.

If you wish to increase your personal property limit, each $5,000 increase in coverage will cost approximately $1 more per month. For example, increasing from the standard $35,000 personal property limit to $50,000 will cost an additional $3 per month.

RBC also offers special coverage options for individual items. For example, animals, birds, and fish can be covered for up to $2,500. Collectibles, such as sports cards or comic books, can be covered up to $5,000. Art, such as paintings or drawings, can be covered for up to $15,000 each.

The table below shows the approximate additional cost of add-on coverage with RBC, based on the above sample quote.

RBC Tenant Insurance Add-Ons

| Add-On | Approximate Additional Cost |

|---|---|

| Overland Water ($1,000 deductible) | $2.00/month |

| Jewelry (Up to $10,000) | $4.50/month |

| Claims Protector (First claim won’t affect claims-free discount) | $3.60/month |

| Identity Theft (Up to $40,000) | $2.70/month |

| Disappearing Deductible Endorsement (Every year without claims will reduce your deductible by 20%) | $4.10/month |

| Sewer Backup (Policy Limit) | $0.50/month |

RBC Tenant Insurance Discounts

Discounts that you may be eligible for include insured age discounts, bundling discounts, and buying online discounts. If you buy your tenant insurance online with RBC, you can get 5% off the first year. Bundling your RBC tenant insurance with RBC car insurance can save you up to 15%.

The age of the home can also give additional discounts. The discount depends on the age of the home, ranging from a 12% discount if the home is 6 years old or less, to a 1% discount if the home is 14 years old.

RBC Home Insured Age Discount

| Home Age | Discount |

|---|---|

| 6 years or less | 12% |

| 7 years | 11% |

| 8 years | 10% |

| 9 years | 9% |

| 10 years | 8% |

| 11 years | 6% |

| 12 years | 4% |

| 13 years | 2% |

| 14 years | 1% |

Insurance

Sample Quote: $46.08/month

TD Insurance offers a variety of insurance products. For tenant insurance, TD has a "home" package and an "enhanced home" package. The home package was used for the sample quote of $46.08 per month, and includes the following:

- $1,000 deductible

- $1 million personal liability limit

- $30,000 personal property limit

- $15,000 additional living expenses

- $30,000 water damage

- High-value items (Up to $500 for money, $2,000 for bikes, $5,000 for jewellery/furs, $10,000 for collectables, $10,000 for wine/spirits, $20,000 for art)

The enhanced home package had a sample quote of $59.33 per month, and included a boosted personal liability limit of $2 million, personal belongings of $40,000, living expenses up to $20,000, enhanced high-value item coverage, first-time claim forgiveness, family coverage, and identity theft coverage.

TD Tenant Insurance Discounts

Just like RBC, TD also gives a 5% discount if you buy tenant insurance with them online. For the same sample quote, you can save around $2 per month if you bundle car insurance with TD.

With TD Insurance Meloche Monnex, you can save even more on your tenant insurance by being an eligible alumni or professional. For example, being an University of Toronto alumni took off $5 per month from the quoted rate.

Insurance

Sample Quote: $35.67/month

Intact Insurance is a well known Canadian insurance company that offers a variety of insurance products for both individuals and businesses. Some of the products that Intact Insurance offers include: auto insurance, home insurance, life insurance, business insurance, and travel insurance.

For its tenant insurance offering, you can choose between paying your premium monthly or up-front annually. If you make monthly premium payments, you will be charged an additional 3% interest. The sample quote of $35.67 per month is based on:

- $1,000 deductible

- $1 million personal liability limit

- $30,000 personal property limit

- Sewer backup (up to policy limit)

- Flood/rainfall (up to policy limit)

Add-ons include Intact Insurance's Claims Advantage, which covers your deductible (up to $1,000) on your first claim. This costs an extra $2.50 per month. You can also add-on identity theft protection for an extra $4.16 per month.

Intact Tenant Insurance Discounts

Having a monitored alarm system can save you up to 5%, while a monitored smoke detector can save you an additional 5%. Having your car insurance with Intact can save you another 15%. If there is a smoker living in the home, your premium will cost 5% more.

Insurance

Sample Quote: $44.50/month

Desjardins Insurance is a subsidiary of Desjardins Group, the largest cooperative financial group in Canada. Headquartered in Quebec, Desjardins Insurance offers a full range of personal and commercial insurance products and services through its network of 215 caisses and 782 points of service across Quebec and Ontario.

The sample quote of $44.50/month is based on:

- $1,000 deductible

- $1 million personal liability limit

- $30,000 personal property limit

- $10,000 water coverage

- $6,000 additional living expenses

- $5,000 voluntary medical payments

- $1,000 voluntary damage payments

When estimating the right personal property limit for you, Desjardins recommends $8,000 to $10,000 per room. You should also consider the replacement cost of the items, rather than the current value of the items, when choosing your personal property limit. While an old fridge might not be worth much today, replacing it with a new fridge will cost more than the cash value of the old fridge.

Desjardins Tenant Insurance Discounts

Desjardins offers a variety of discounts, such as:

- Up to 15% off for bundling with auto insurance

- Up to 10% off if you have a leak detection system with automatic water shutoff

- Up to 5% off if you have at least five monitored leak detectors

- Up to 10% off your ground water and sewer backup coverage if you have a pneumatic backflow system

- Up to 10% off if you have a monitored fire and burglar alarm system

- Up to 20% off if you are claims-free

- Up to 10% off if your home is LEED-certified

Insurance

Sample Quote: $27.31/month

APOLLO is a digital insurance broker that offers a variety of insurance products, from tenant insurance to renovations insurance, and even wedding insurance. For APOLLO’s tenant insurance, you can choose between three packages: basic, enhanced, and premium.

The enhanced package includes accidental damage coverage, while the premium package adds water coverage on top of that. APOLLO has lower standard coverage limits for items than other insurers, however, you can always choose to purchase higher limits. Examples of the standard coverage limits include $2,000 for jewellery, $1,000 for bikes, $1,000 for art, and $2,500 for computers. Increasing your personal liability coverage from $1 million to $2 million costs an extra $3 per month.

The sample quote of $27.31 is based on:

- $1,000 deductible

- $1 million personal liability limit

- $30,000 personal property limit

- $5,000 additional living expenses

- $3,000 freezer food spoilage

- $6,000 voluntary medical payments

- $2,000 voluntary damage payments

Paying your premium annually can save you 10% compared to a monthly payment plan. APOLLO requires a 25% premium deposit for tenant’s insurance.

One

Sample Quote: $15.21/month

Based in Vancouver, Square One offers tenant insurance in British Columbia, Ontario, Quebec, Alberta, Manitoba, and Saskatchewan. You can completely customize your tenant insurance coverage with Square One, which allows for very affordable rates if you don’t need any add-ons. Square One also doesn’t charge interest for making monthly premium payments.

The sample quote of $15.21 is based on:

- $1,000 deductible

- $1 million personal liability limit

- $40,000 personal property limit

- $35,000 additional living expenses

The basic additional living expenses coverage is up to $5,000. Increasing it to $35,000 will cost an additional $2.49 per month. Personal liability coverage can be reduced to $500,000 from the standard $1 million limit, saving you about $1 per month. Increasing to $2 million will cost an extra $3 per month.

Increasing your deductible from $1,000 to $2,500 can save you $1.50 per month. Increasing it to $5,000 can save you $3.00 per month. Reducing your deductible to $500 will cost an extra $5.50 per month, while a deductible of $250 will cost an extra $8.00 per month.

Square One Tenant Insurance Add-Ons

| Add-On | Approximate Additional Cost |

|---|---|

| Recreational Equipment (Up to $5,000) | $6.89/month |

| Business Property (Up to $5,000) | $2.16/month |

| Art/Collectibles (Up to $6,000) | $2.17/month |

| Jewellery/Watches (Up to $6,000) | $3.35/month |

| Identity Theft (Up to $10,000) | $1.67/month |

| Legal Protection (Up to $100,000) | $2.50/month |

Insurance

Sample Quote: $21.00/month

CAA Insurance is one of the leading providers of auto insurance in Canada. CAA also offers home and renters insurance. The sample quote of $21.00 is based on:

- $1,000 deductible

- $1 million personal liability limit

- $40,000 personal property limit

- $10,000 water coverage

- Home equipment coverage (up to $100,000)

For an extra $2 per month, you can add claim forgiveness on your first claim, allowing you to keep your claims-free discount.

CAA Tenant Insurance Discounts

CAA members can save an additional 10% on their tenant insurance. Bundling with auto insurance can save you 12.5%, and a family discount of 5% is given if you have a family member with an existing CAA insurance policy.

Insurance

Sample Quote: $68.00/month

Co-operators is a Canadian insurance company that was founded in 1945 by a group of Canadian farmers who wanted to pool their resources. The Co-operators is now one of the largest insurers in Canada, offering home, auto, life, farm, business, travel, and group insurance products.

The sample quote of $68.00 per month for Co-operator’s tenant insurance is based on:

- $1,000 deductible

- $1 million personal liability limit

- $40,000 personal property limit

Co-operators Tenant Insurance Discounts

The Co-operators offer four different discounts. The first is a multiproduct discount for having another insurance policy with Co-operators, and takes off $1 from your monthly premium. Having a monitored alarm system, and fire sprinklers, and/or being LEED certified would take off around $6 per month each.

Insurance

Sample Quote: $17.96/month

Duuo is a digital insurance company that is owned by Co-operators. Duuo offers unique insurance products, such as event insurance, vendor insurance, and short-term rental insurance, as well as tenant insurance. Duuo's tenant insurance is flexible in terms of it being a month-to-month insurance plan. You can cancel at any time, and you will receive a prorated refund for unused portions of a month.

The sample quote of $17.96 per month for Duuo’s tenant insurance is based on:

- $1,000 deductible

- $1 million personal liability limit

- $25,000 personal property limit

Increasing the personal property limit to $50,000 will increase the sample quote to $21.55 per month. Increasing the personal liability limit to $2 million as well as a $50,000 personal property limit will cost $26.49 per month.

Insurance

Sample Quote: $38.88/month

While Aviva is the underwriter for RBC's tenant insurance products, Aviva Canada also distributes its own tenant insurance underwritten by S&Y Insurance. S&Y Insurance is wholly-owned by Aviva.

The sample quote of $38.88 per month for Aviva’s tenant insurance is based on:

- $1,000 deductible

- $1 million personal liability limit

- $35,000 personal property limit

- $14,000 additional living expenses

- $5,000 voluntary medical payments

- $1,000 voluntary property damage

- $20,000 sewer backup coverage

Insurance

Sample Quote: $51.66/month

National Bank only offers tenant insurance in Ontario and Quebec. National Bank's tenant insurance includes the usual personal property, liability, and living expenses coverage. For additional living expenses, you're covered for up to 30% of the total value of your belongings. For medical expenses, you may be covered for up to $5,000. An 8% tax applies to National Bank's yearly insurance premium.

Is Tenant Insurance Mandatory in Canada?

Tenant insurance is not mandatory in Canada. It's also not required by law in any province. Since tenant insurance is optional, in light of high rents in rental markets across the country, some tenants might choose to save money by not getting tenant insurance. Others might feel that tenant insurance isn't needed. However, it's still highly recommended to get tenant insurance. Landlords may also require tenants to have tenant insurance as a condition of their lease. It’s similar to how mortgage lenders can require borrowers to have home insurance in order to be approved for a mortgage.

Landlord insurance covers the building and the property of the landlord, but not the contents inside the building that belongs to tenants. As a tenant, you are responsible for your own belongings and any damage you may cause to the rental unit or building. If you don't have insurance, you could be on the hook for thousands of dollars in repairs or replacements. Having tenant insurance is a way to protect yourself financially in case something goes wrong.

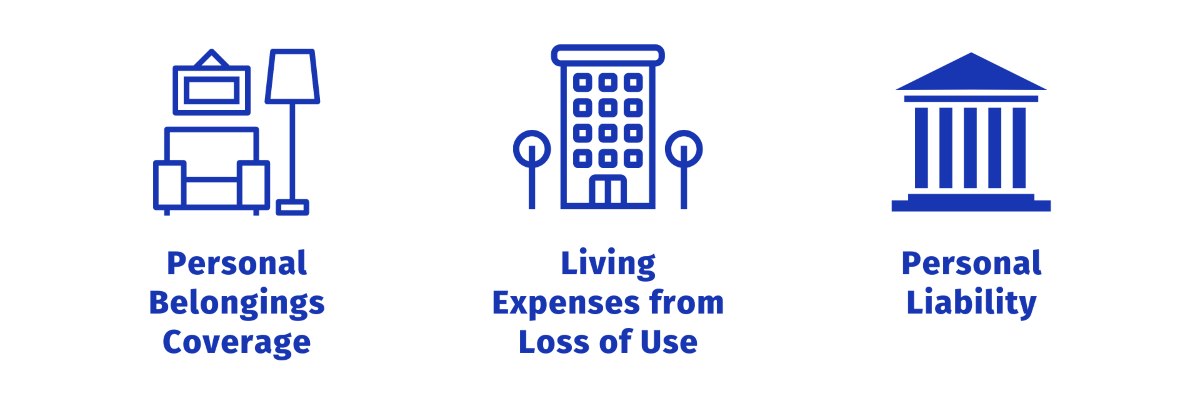

What Does Tenant Insurance Cover?

Most tenant insurance policies will cover the following:

- Theft or damage to personal belongings: This can include furniture, clothing, electronics, and other items that are stolen, or items that are damaged or destroyed by flood or fire.

- Loss of use: If the tenant's home becomes uninhabitable due to damage covered by the tenant insurance policy, the tenant may be reimbursed for living expenses incurred while the home is being repaired. This might include the cost of temporary housing, such as a hotel room, and the cost of transportation and food.

- Personal liability: If the tenant is sued for damages arising from an injury that occurred on the premises or for damage caused by the tenant's negligence, the tenant insurance policy may cover legal expenses and any resulting judgments or settlements.

What Is Not Covered by Tenant Insurance?

Tenant insurance does not cover the structure of the rental unit itself, such as the walls, floors, ceilings, or fixtures. This is the landlord's responsibility, which they might insure by purchasing landlord insurance. Tenant insurance also does not cover damage caused by normal wear and tear, such as faded wall paint that needs touching up or worn out stairs. Intentional damage is also not covered. Examples of intentional damage include putting a hole in the wall or smashing a window on purpose. On the other hand, if you accidentally break something, your tenant insurance may cover it depending on your policy.

Lastly, most policies have limits on how much they will pay for certain items, such as jewelry or collectibles. Certain high-value items, such as jewelry, collectibles, and artwork, may require an add-on to your insurance policy to cover them specifically. This is known as an insurance floater.

When comparing tenant insurance providers, tenants should check their policy to see what is covered and what is not. It is important to check to make sure that you are getting the coverage that you need. You don't want to find out too late that something isn't covered and then have to pay for it out of your own pocket!

Does Tenant Insurance Cover Accidental Damage to Landlord’s Property?

Yes, tenant’s insurance covers accidental damage to your landlord's property. For example, leaving the stove on and starting a fire or causing smoke damage, or flooding from a sink, can not only damage your unit but neighbouring units as well. Tenant insurance will cover the cost of repairs and damages for the belongings in your unit, through your contents coverage, and you'll be covered for damages to neighbouring units if you're held liable with your personal liability coverage.

What Affects the Cost of Tenant Insurance?

There are a variety of factors that affect the cost of tenant insurance rates. The most important factor is the type and amount of coverage you need. The second most important factor is the location of your rental property. Other factors include the value of your personal belongings, if you need any special coverage for high-value items, the property type, your insurance claims history, and your tenant insurance deductible.

The type of coverage you need will have the biggest impact on your tenant insurance rates. Basic coverage usually includes liability protection, which covers you if someone is injured while on your property or if you damage someone else's property. You may also want to add additional coverage for your high-value personal belongings, such as electronics or jewelry. The amount of coverage will affect your rate. Most cover up to $1 million, while you may choose to buy tenant insurance that covers up to $2 million or more.

The location of your rental property can affect your tenant insurance rates. If you live in a high-crime area, you may pay more for coverage than someone who lives in a low-crime area.

Finally, if you have any special coverage needs, such as for high-value items, you may need to purchase additional insurance to protect these items. Special coverage typically costs more than basic coverage, but it can give you peace of mind knowing that your valuable possessions are protected.

Can My Credit Score Affect My Tenant Insurance Rate?

Yes, your credit score can affect your tenant insurance rate in most provinces. If you have a poor credit score, you may be seen as a higher risk to the insurer and could be charged a higher premium. If you have a good credit score, you may be seen as a lower risk and could be charged a lower premium. Insurance companies typically use credit scores as one factor in determining rates, so it's important to keep your credit in good standing if you want to get the best rates on your tenant insurance.

Some provinces prohibit insurance companies from using your credit information. For example, Newfoundland and Labrador's Insurance Prohibited Underwriting Regulations under the Insurance Companies Act prevents personal insurance companies in the province from using credit information to decline or terminate someone's coverage. This prevents them from using your credit score or credit report.

Other provinces, such as Ontario and Alberta, only prohibit credit score information from being used for car insurance decisions. This means that your credit score can still affect your tenant insurance premiums in Ontario and Alberta. Some insurers provide a discount for allowing a credit check. This discount may even be as high as 20% off your premiums!

If I’m a Student, Do I Need Tenant Insurance?

Full-time students might not need to get tenant insurance if your parents have home insurance that covers you. This might be the case if you are considered to be a dependent, such as if you are under the age of 21, or if you are under the age of 25 and attending college or university as a full-time student. Your parents will need to inform their insurer about your status.

However, even if you are covered by your parents' home insurance policy, you may still get tenant insurance to cover your personal belongings. Home insurance policies often have limits on the amount they will pay out for your personal belongings.

How Do I Buy Tenant Insurance?

The first step is to find an insurance company that offers renters insurance. You can do this by searching online or asking around for recommendations. This page also has a list of some of the best tenant insurance companies in Canada, sample quotes, and coverage options. Once you've found a few potential insurers, compare their rates and coverage options to find the best policy for your needs.

After you have chosen an insurer, you'll need to purchase a policy. This can usually be done online or over the phone. Quotes that you receive might only be valid for a certain period of time, such as 30 days, which means that waiting too long may result in a different rate. Your actual rate might also vary from your quote.

When getting a quote, you’ll be asked for the date that you want your tenant insurance to be effective. Your renter's insurance policy might start as soon as you pay the premium. However, some policies may have a waiting period before they go into effect. Be sure to check with your insurer to find out when your policy will start.

Now that you have a renter's insurance policy, be sure to keep it up to date. If you move to a new rental property, be sure to let your insurer know so they can update your policy. If you make any changes to your belongings or the way you use your rental unit, such as if you are now running a home business or if you’re getting a pet, be sure to notify your insurer so they can adjust your coverage accordingly. Failing to inform your insurer may result in denied claims and could even void your insurance coverage. This can also cause negative implications when you try to buy insurance from another insurer.

Tips for Cheap Tenant Insurance

Looking to get cheap tenant insurance rates? You may be able to get a discount if you bundle your tenants insurance with other types of insurance, such as car insurance. Ask your insurance broker or agent about bundling discounts. You may also be able to get a discount if you have a security system installed in your rental unit. You can also save money on your tenants insurance by choosing a higher deductible. A higher deductible means you will have to pay more out of pocket if you make a claim, but it will also lower your insurance premiums.

Check for discounts that your insurer might offer. You might be eligible for alumni rates, for instance, or even discounts for buying your tenants insurance online. For example, RBC offers a Buy Online Discount of 5% for your first year if you buy insurance online on their website, rather than with an RBC insurance advisor.

The best way to find affordable tenant insurance is to compare quotes from multiple insurers. Be sure to get quotes for the same type and amount of coverage, so you can accurately compare costs. You can use an online quote comparison tool or work with an insurance agent to get started. Keep in mind that the cheapest option may not always be the best, so be sure to read the fine print.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.