Home Equity Loan:

How to Build and Use Home Equity

What You Should Know

- Home equity refers to the portion of your home that you actually own. It's calculated by subtracting any outstanding mortgage balances from the property's market value.

- Building home equity can be accomplished by reducing your mortgage balance (through regular mortgage payments) and increasing your property's value (through home improvements or real estate market growth).

- You can borrow against your home equity to finance your retirement, or if you need cash, such as with home equity loans as a second mortgage, cash-out refinance, HELOC, or reverse mortgage.

What Is a Home Equity Loan?

A home equity loan is a type of loan that allows homeowners to borrow money against the value of their home. You can have a standalone home equity loan or borrow it as an additional loan on top of your existing mortgage.

Home equity is the amount of your home that you own. In other words, it's the current market value of your property minus any debt or liens attached to it. There are multiple ways to gain home equity, such as paying off your mortgage, making home improvements that increase your home's value, or simply having your property appreciate over time.

How Does a Home Equity Loan Work?

Home equity loans are similar to traditional mortgages in that they use your home as collateral. For some types of home equity loans, the borrower receives a lump sum of money from the lender and makes monthly payments to repay the loan, typically over a fixed term. For other types, the borrower may be given access to a line of credit that can be withdrawn as needed.

The amount that can be borrowed through a home equity loan is based on the current appraised value of your home minus any outstanding mortgage balance or debt tied to the home. Your home equity is the difference between the two and is used as collateral for the loan. If you have paid off a significant portion of your mortgage and your home has increased in value, you may be able to borrow a larger amount.

How Home Equity Works 💡

How home equity works is that it is something that belongs to you as a homeowner, and can be used as an asset. If you purchase a home with a mortgage, the home will be used as collateral for the mortgage loan. The difference between your home’s value and the debt secured by your home is known as home equity. When you fully pay off your mortgage, your home equity will be the full value of your home.

For example, when buying a house with a conventional mortgage, you must make at least a 20% down payment. When you first buy the house, this 20% is your home equity. If we apply this scenario to a $100,000 home, your home equity is $20,000 (20%*100,000).

Initially, your home equity is the result of your down payment. As you make mortgage payments, your home equity grows. As the value of your home increases and you pay off more of your mortgage, your home equity continues to grow.

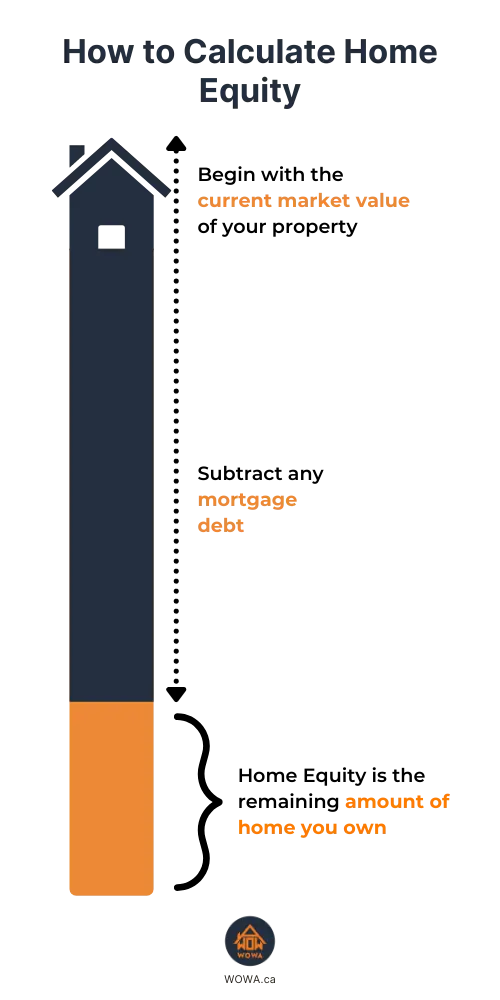

How to Calculate Home Equity

To calculate your home equity, you need to know two things: your home's current fair market value and the total balance of your mortgage and any other liens against your property. A lien can arise from a purchase loan, second mortgage, or any similar financial product that is secured by your home.

For example, if your home value is $500,000 and you currently have a $300,000 mortgage balance remaining, your home equity is $200,000.

A real estate agent can estimate the fair market value of your home through comparative market analysis. You subtract your mortgage balance from your home market value to find your home equity with this information.

Types of Home Equity Loans

There are three main types of loans using your home equity in Canada: home equity loans, HELOCs, and reverse mortgages. You can also use your home equity with a cash-out refinance. Each type of loan has its own set of benefits and drawbacks, so it's essential to understand them before deciding which one is right for you.

| Loan Type | Maximum Total LTV | Interest Rates | Access to Money |

|---|---|---|---|

| Cash-out Refinance | 80% | Fixed or Variable. Typically lowest interest rates. | One bulk sum deposited to your bank account. |

| Second Mortgage | 80% Total | Fixed or Variable. Typically higher than a primary mortgage. | One bulk sum delivered to your bank account. |

| HELOC | 65-80% Total | Variable. Changes with the prime rate. | Borrow as you need. |

| Reverse Mortgage | 55% Total | Fixed or Variable. Higher than a primary mortgage. | Either monthly installments or one lump sum. |

Home Equity Loans

A home equity loan, also known as a second mortgage when used in addition to your existing mortgage, is a lump sum loan that uses your home as collateral. The amount you can borrow is based on the difference between your home's current market value and the amount you owe on your mortgage. You receive the funds in one lump sum and make monthly payments with a fixed or variable interest rate until the loan is paid off.

HELOCs

A Home Equity Line of Credit (HELOC) is a revolving line of credit that uses your home as collateral. This means you can borrow money as needed up to a predetermined limit and pay it back at any time. HELOCs typically have variable interest rates based on the prime rate, so your monthly payments will vary based on how much you borrow and current interest rates.

Reverse Mortgages

A reverse mortgage is a loan for homeowners aged 55 or older that uses their home equity as collateral. Unlike traditional mortgages, you do not have to make monthly payments; instead, the loan must be repaid when the house is sold, if you move out, or when the homeowner dies. Interest accrues on the loan but your reverse mortgage balance will never exceed the value of your home, and it is typically paid off through the sale of the home at a later date. This type of loan is beneficial for retirees who may need extra income but do not want to sell their home.

Refinance Your Mortgage 💡

Another way to use your home equity is by refinancing your mortgage. This involves replacing your current mortgage with a new one, ideally at a lower interest rate. The difference between the new loan amount and the remaining balance on your old mortgage is paid out in cash, which can be used for various expenses.

Refinancing has its own set of advantages and may be a better option for some homeowners, depending on their financial situation. Some possible benefits of a cash-out refinance include:

- Access to cash: If you have a significant amount of equity in your home, refinancing can give you access to a large sum of money.

- Consolidating debt: You can use the cash from refinancing to pay off high-interest debts and consolidate them into one manageable payment with a lower interest rate. This can potentially save you money in the long run.

- Lower interest rates: Refinancing can potentially save you money by securing a lower interest rate than your current mortgage, if rates have decreased since you first took out your loan.

- Change in loan terms: If your financial situation has changed, refinancing can allow you to adjust your mortgage term or type to better suit your needs.

Using a Home Equity Loan

When considering a home equity loan, you’ll need to determine if it is the right financial decision for your specific situation. Typical uses for a home equity loan include access to cash or retirement income.

Access to Cash

Homeowners in need of cash have many options to borrow against their equity. There are multiple reasons to borrow against your home equity, including: starting a business, home renovations, consolidating your debt, buying a cottage, paying your child's tuition, and many more. Multiple products are available with slight nuances, and this section will help you differentiate them to decide the best ones for your situation.

- Home equity line of credit: A HELOC is the most popular way to borrow from your home equity due to its flexibility. It is a pay-as-you-go option that allows you only to pay for the money you borrow. If you do not withdraw from the account, then you don't have to pay anything. HELOC interest rates tend to be higher than a typical mortgage, although many lenders provide interest-only periods for payments. This means you only have to pay the interest amount on your HELOC, making it an affordable short-term option.

- Cash-out refinance: Cash-out refinances are a great option for debt consolidation or investors. This option lets you borrow a large lump sum of money at a lower interest rate than a HELOC. However, unlike a HELOC, there is less flexibility because you receive a large sum of money and immediately need to pay interest. Additionally, you will need to change mortgages, so there may be a penalty for switching before your term ends.

- Second mortgage: Unlike a cash-out refinance, a second mortgage will allow you to keep the same primary mortgage. As a result, there is no risk your primary mortgage interest rate will increase, and you won't need to pay any penalties for ending your primary mortgage early. You will receive a lump sum of money at a slightly higher interest rate than a conventional mortgage.

Retirement Income

Retirees can spend their golden years using their home equity to finance retirement. There are two main options: downsizing their home or using a reverse mortgage to stay in the same house.

- Downsizing: This is the traditional approach to retirement. Many retirees sell property and then buy a cheaper home. From there, they can use the cash received from selling to help fund retirement. However, you may not want to sell your home, and if you do, then you'll have to pay capital gains tax if it's not your primary residence.

- Reverse Mortgage: A reverse mortgage allows retirees to continue living in their homes and receive a monthly payment to help fund retirement. Eventually, when you sell the home, the bank will collect the amount of money owed. Additionally, the interest rates on reverse mortgages tend to be higher than regular mortgage rates.

How to Build Home Equity

Building home equity is a process that takes time and effort. Here are some ways to build home equity.

Higher initial down payment

This is the fastest way to build home equity. The more money you invest in your home, the higher home equity you receive. As mentioned before, if you put 20% down when purchasing a $100,000 home, your initial home equity is $20,000.

Additionally, paying a higher down payment upfront will cause you to pay less interest throughout your mortgage. As a result, you'll end up building home equity faster. A higher down payment may also help you get the best mortgage rates in Canada.

Property value appreciates

Your home equity builds as the value of your house rises. Your mortgage debt stays the same while your property appreciates in value. As a result, you benefit from the full property appreciation, and it goes straight to your home equity. A healthy and expanding real estate market will passively increase your equity and wealth.

However, it is worth clarifying that many down payment assistance programs (DPAPs) use a shared equity mortgage. If you have a shared equity mortgage (which isn't common), some appreciation is shared with your mortgage lender.

Another way to increase the value of your home is through renovations. If you add an extra room to your home, increase the livable space by converting a garage into a living space or change the paint and flooring of your property, then its value could rise.

Continue making mortgage payments

This one will take the longest to impact your home equity. This is because, in the first few years of paying off your mortgage, most of your payment is only paying off your loan's interest. As a result, they don’t significantly affect the bank's security interest in your property - otherwise known as the mortgage principal.

However, as your principal balance shrinks, more of your monthly mortgage payments will go towards paying off your principal balance. At this point, each payment will affect your home equity. You will see significant increases in the equity you own each year. Some homeowners prefer to make accelerated mortgage payments to pay off their mortgage and build home equity faster.

Making mortgage prepayments, which are additional payments towards your principal balance, will go to your home equity by directly paying down your mortgage principal. For instance, if your home is worth $300,000 and you have a mortgage of $250,000, you have $50,000 in home equity. If you make an extra payment of $10,000 towards your principal balance, your mortgage will now be $240,000, and your home equity will increase to $60,000.

Frequently Asked Questions

What is home equity?

Home equity is the value of your home minus any debt you owe that's directly tied to your home. You can think of home equity as the portion of your home that you own as you pay off your mortgage.

What are home equity loans?

A home equity loan is secured by your home equity. You borrow money from your home and receive it in cash. They are a great way to turn illiquid assets (your home) into something liquid (cash). Additionally, they tend to have low interest rates.

Am I eligible for a home equity loan?

To be eligible for a home equity loan, you must have more than 20% equity in your home. Additionally, you must have a good credit score to get the best interest rates. A HELOC is typically the most accessible home equity loan to get.

How much money can I borrow against my home?

In Canada, you can not borrow more than 65 to 80% of your total home value, depending on the home equity loan type. For example, imagine you have a $100,000 home with $50,000 of debt tied to the property. Given an 80% maximum loan to value (LTV) with a second mortgage, you would be able to borrow up to a total of $80,000 from your property. This means you can borrow an additional $30,000 (80,000-50,000) from your home equity with a second mortgage.

What are the best renovations to increase my home equity?

Some great ways to increase the value of your home include renovating your bathrooms and kitchen, installing new windows or a roof, and finishing your basement. However, these more expensive projects may require a home renovation loan.

If you are looking for smaller projects, then some items that have a significant impact on your home value include:

- Installing new lights

- Updating the curb appeal

- A fresh coat of paint

- Installing a new water heater

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.