Mortgage Qualifying Rate in Canada

What You Should Know

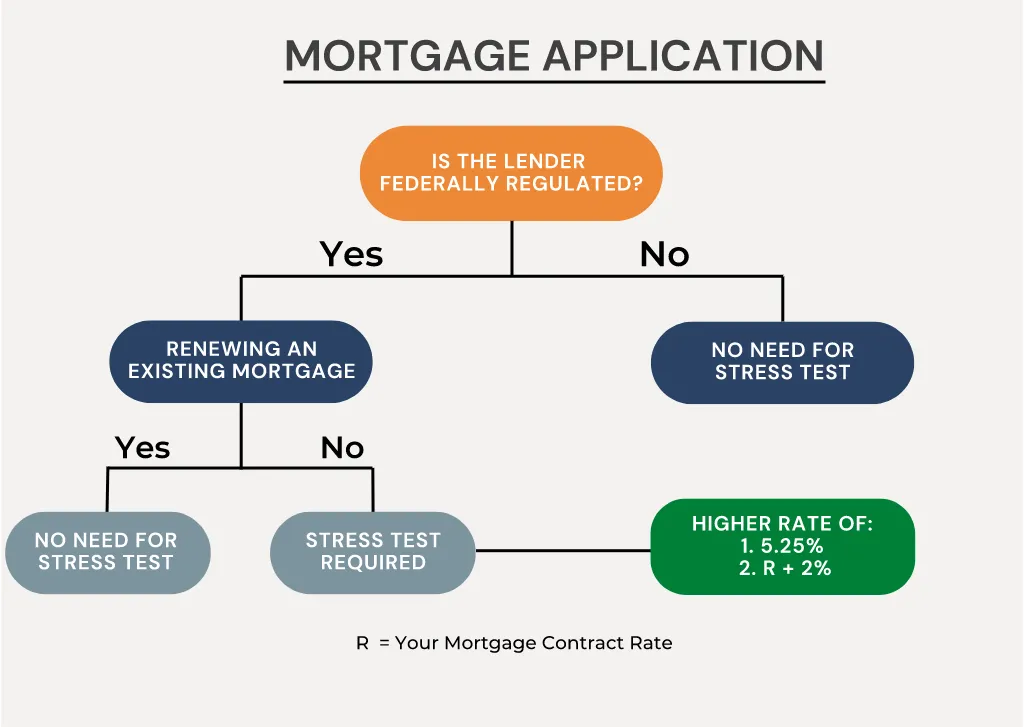

- Each Federally Regulated Financial Institution is mandated to perform a stress test before advancing a mortgage.

- Passing the stress test requires the ability to afford the mortgage at the mortgage qualifying rate (MQR).

- The mortgage qualifying rate is your contract interest rate plus a buffer of 2%, or a minimum of 5.25%.

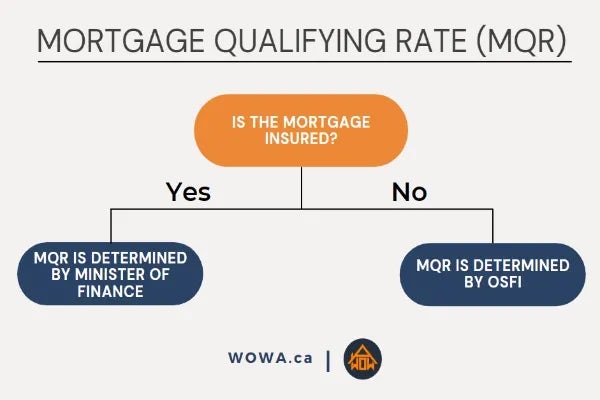

Mortgage Qualifying Rate

The mortgage qualifying rate (MQR) is the greater of a floor of 5.25% or your mortgage contract rate + a buffer of 2%. For example, if your mortgage contract rate is 4%, then your MQR would be the greater of 4% + 2% or 5.25%, which in this case would be 6%. This means that the lender would check if you could still afford your mortgage at a rate of 6%.

MQR is set by the Office of the Superintendent of Financial Institutions (OSFI) for uninsured mortgages and by the Department of Finance (DoF) for insured mortgages. Currently, both OSFI and the DoF have set the same MQR. This rate came into effect on June 1, 2021, and was reaffirmed in December 2021, December 2022 and December 2023. Before June 1, 2021, the floor for MQR was 4.79%. OSFI has a framework to review both the floor and the buffer of the MQR regularly. Such a review can occur at any time but would occur at least once a year in December. The finance minister often makes an announcement about MQR hours after a similar announcement by OSFI.

Note that only Federally Regulated Financial Institutions (FRFIs) are mandated to perform a stress test. The stress test is put in place to guarantee the stability of Canada’s financial system. Yet it is also good for borrowers. A borrower who borrows less than what they can afford will be able to absorb a negative shock without having to go through painful or traumatic adjustments like an eviction or foreclosure.

Still, if you understand the risks involved and the only thing standing between you and your future home is a stress test, you can use a provincially regulated financial institution. For example, credit unions are provincially regulated, so they do not have to perform a stress test.

Moreover, a stress test is only necessary if a mortgage needs to be funded. As a result, a mortgage renewal does not require a stress test, while a mortgage refinance requires a stress test.

Reasoning Behind Stress Test

The financial well-being of Federally Regulated Financial Institutions (FRFIs), like Canadian banks and Canadian insurance companies, is essential for the stability and health of the Canadian economy. Thus FRFIs are expected to ensure their mortgage borrowers can absorb some adverse shocks. A negative shock can come in the form of a higher mortgage rate, reduced income or an unexpected increase in expenses.

An FRFI performs a mortgage stress test before agreeing to a mortgage to ensure the borrower's ability to absorb a shock. A mortgage stress test assumes that your mortgage rate rises to the mortgage qualifying rate (MQR). A borrower passes the stress test if they can still afford the mortgage at the MQR. If they fail to pass the stress test at the MQR, the lender could offer them a smaller mortgage amount or ask them to make a bigger down payment.

Office of the Superintendent of Financial Institutions

In Canada, OSFI regulates banks, insurance companies, trust companies, loan companies and pension plans. OSFI is an independent federal agency which reports to the Minister of Finance. OSFI is mandated to protect depositors, policyholders, financial institution creditors, and pension plan members while allowing financial institutions to compete and take reasonable risks. Canada Deposit Insurance Corporation (CDIC) and the Bank of Canada (BoC) are other regulators of financial institutions in Canada.

History of OSFI

The “Financial Institutions and Deposit Insurance Amendment Act" and the “Office of the Superintendent of Financial Institutions Act” were enacted in 1987. As a result, the “Department of Insurance” and the “Office of the Inspector General of Banks” were combined, and the Office of the Superintendent of Financial Institutions (OSFI) was created. Since then, OSFI has supervised and regulated all federally regulated financial institutions.

In 1996, bill C-15 became law. Bill C-15 clarifies OSFI’s prime role in minimizing losses to depositors, policyholders and pension plan members. OSFI is also tasked with maintaining public confidence in the Canadian financial system.

Role of OSFI in the Mortgage Industry

Residential mortgages are the largest exposure for many Canadian financial institutions. As a result, OSFI pays special attention to regulating mortgages. Regulation of the mortgage industry became considerably more stringent after the 2008 financial crisis when the American mortgage industry almost destroyed the global financial system.

OSFI expects financial institutions to judge the borrower's ability to pay their loan over the amortization period before granting a mortgage. OSFI has issued guideline B-20, which outlines the standards to be followed when approving mortgages. This guideline governs the underwriting of any loan secured by residential property. Residential property is a dwelling (any type of home) with one to four units. So, in addition to mortgages, it regulates HELOCs and equity loans.

Mortgage Lending Principles

B-20 asks lenders to act based on five principles.

- The first principle is that the lender should have business objectives, strategy and oversight mechanisms in respect of residential mortgage underwriting and acquisition of residential mortgage assets.

- The second principle is to assess the borrower's identity and willingness to serve their debt on time.

- The third principle is to assess the borrower's ability to repay their debt in a timely manner.

- The fourth principle is to assess the value and management of the property underlying the mortgage.

- Principles 2 to 4 should be followed using a risk-based approach. The primary basis for credit decisions should be the borrower's willingness and ability to service their debt, and overreliance on the collateral should be avoided.

- The fifth principle asks for adequate credit and counterparty risk management, which might mean mortgage insurance.

Effect of Stress Test

Let us consider the purchase of a home for $630k, with the purchaser having saved $100k for their down payment. Further, assume that they are interested in a five-year fixed-rate mortgage and that they can get a rate of 4.6% for a mortgage with a 25-year amortization period.

Then,

- The monthly mortgage payment is $3,046, calculated using a mortgage payment calculator

- They would need a gross monthly income of $3,046/0.39 = 7,810 to afford this house, based on the recommended gross debt service (GDS) of 39%.

Now, let us consider the stress test scenario that requires us to consider a 2% safety margin. Meaning that our purchaser needs to afford his mortgage at an interest rate of 6.6%.

Then,

- The monthly mortgage installments increase to $3,683.

- For this installment to be affordable, the monthly income required is $9,444 based on the GDS ratio.

As you can see, in the absence of a stress test, a family earning $7,800 a month could afford the home. In the presence of the stress test, that same home is only affordable for families earning more than $9,400 each month. Thus, the stress test is there to encourage people to choose more affordable houses and reduce the risk that they might default in the future.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.