Consolidating Debt Into Mortgage or HELOC in Canada

What You Should Know

- Debt consolidation is the process of paying off multiple high-interest rate debts with a low-interest rate loan.

- It saves you money in the long term because you spend less money on interest payments. However, there may be some initial administrative fees.

- A debt consolidation mortgage or home equity line of credit (HELOC) are great tools to do this.

- You must have sufficient home equity which is the difference in your property value and mortgage balance.

Using a mortgage or HELOC for debt consolidation can save you money in the long term since you pay less interest.

Consolidating Debt Into a Mortgage or HELOC in Canada

It's challenging to handle your finances when you owe multiple high-rate debts such as credit cards or loans. However, if you're a homeowner, you may use the equity in your house to your advantage.

Paying off debt with a consolidation mortgage or home equity line of credit (HELOC) will generally help lower the interest paid. However, there are sometimes hidden fees or circumstances where consolidation does not make sense. This article will provide an in-depth overview of debt consolidation.

What is debt consolidation?

Statistics show that the average household annual debt interest payment per household increased by about 75% from 2022 to 2024. One way households can reduce the interest is through debt consolidation. Debt consolidation is the process of combining several high-interest rate debts into one low rate loan. High-interest rate debt includes things such as credit cards, payday loans, and other non-mortgage balances. In general, these debts have an interest rate of around 20%, meaning a $10,000 balance would cost $2000 of interest every year. By shifting the high-interest debt to a low-interest loan (such as a mortgage or HELOC), borrowers can refinance to the low rates seen below.

The interest rates are lower for a HELOC or mortgage because your property secures them. This means you must have sufficient home equity to qualify. The following section explains the process in detail.

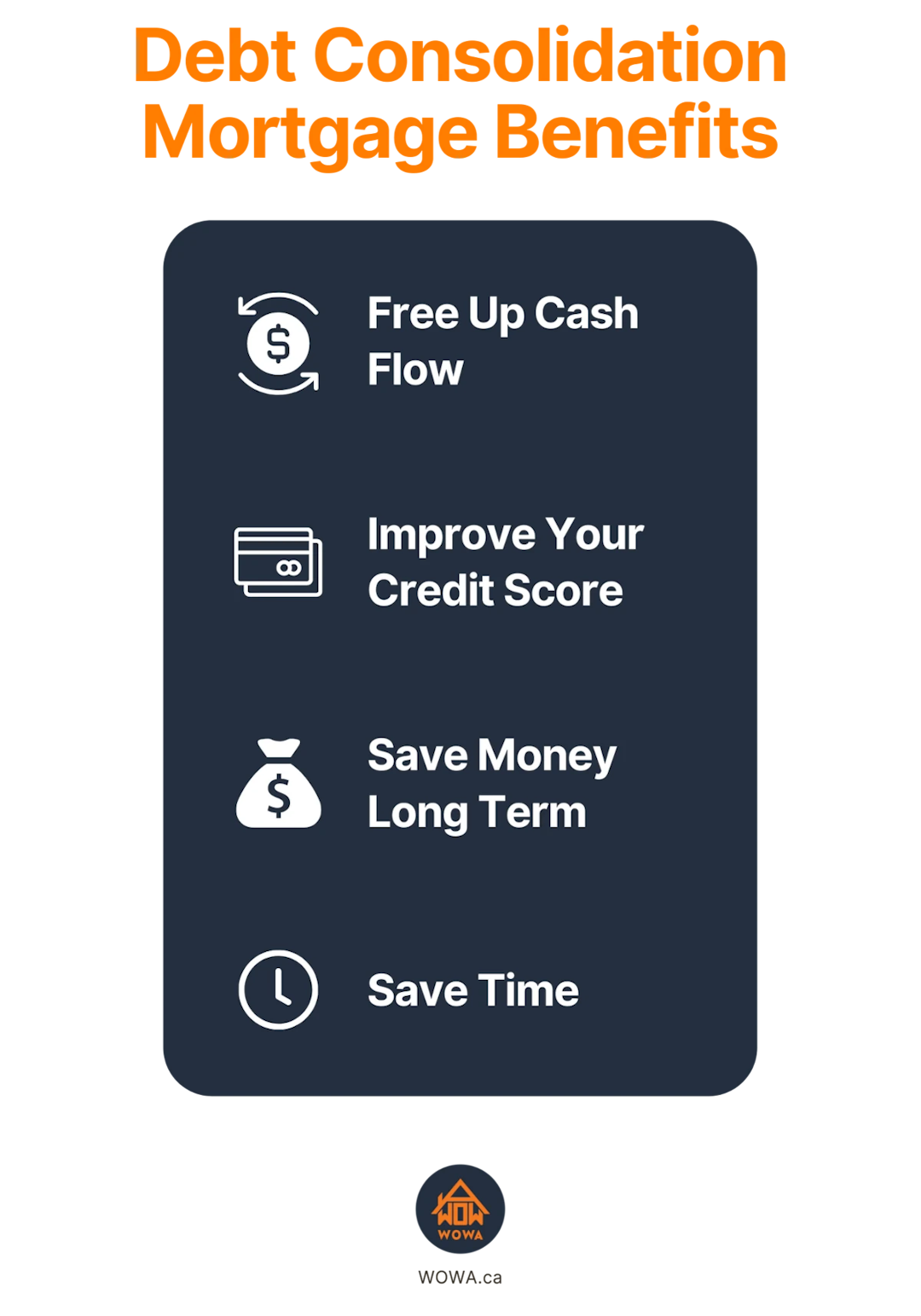

Benefits of debt consolidation

- Free up cash flow: Lower interest rates could decrease your payment sizes. This frees up money in your monthly budget, which you may use for household costs, savings, or simply paying off your mortgage sooner.

- Improve your credit score: Paying off high-interest consumer debt will reduce your credit utilization ratio, which is one way to increase your credit score. Mortgage debt has a lower effect on your credit score than consumer debt. By paying off your credit debt with mortgage debt, your credit score should rise.

- Save money long-term: Credit cards and other consumer debts have significantly higher interest rates than a typical mortgage. Making minimum payments will result in you paying substantially more interest. If you combine your debt into your mortgage or HELOC, you can pay off the loan faster and save money in the long run.

- Save Time: You only need to worry about making one payment instead of many. You'll no longer need to check multiple bills to determine the balance owed on each.

How to consolidate debt into a mortgage?

To qualify for a debt consolidation loan, you must have home equity. Equity is the difference between the value of the home and what is owed on the mortgage.

Let's say your property is worth $200,000, and you owe only $125,000 on your mortgage. As a result, you have $75,000 in equity. Your home equity continues to rise as the property value increases, and you pay off your mortgage debt.

Consolidating debt into a mortgage means refinancing your existing mortgage and rolling high-interest debts into a new mortgage with a lower interest rate. A popular way to do this is using a readvanceable mortgage.

Typically, you can only refinance up to 80% of the property value, which would be $160,000 ($200,000*80%) in our scenario. This would provide the borrower with an additional $35,000 (160,000-125,000) of cash to pay off high-interest debt. As a result, the borrower has effectively switched multiple high-interest debts into one low-interest debt.

However, there are fees associated with refinancing, such as the cost of breaking the old mortgage along with administrative expenses. The upside is that you will be saving the money that otherwise would've been spent on high-interest rate debt.

Comparing a HELOC with debt consolidation mortgages

A home equity line of credit or HELOC, is comparable to a mortgage in most respects. It's registered against the title of your property and is secured by its equity, just like any other mortgage. The primary distinction is that it's a revolving line of credit.

Instead of receiving a set amount of money, home equity loans allow you to withdraw cash as needed. You may also pay it down as quickly as you like.

For example, you might use your HELOC to pay off your other debts and consolidate them into the line of credit. However, instead of making lower payments as you would on a regular mortgage, you may make larger monthly payments and pay off the debt faster. Most loans have early repayment penalties; therefore, it isn't always an option in those instances.

Factors to consider when consolidating debt

There are many factors to consider when determining if a debt consolidation mortgage is right for you. Some of the primary parts include:

- Qualifying for a new mortgage: Regulations like debt service ratios and the stress test make it more challenging to receive a mortgage. Under today's standards, some borrowers will need to question whether they are even qualified for a new mortgage to combine their existing debt.

- New interest rate: Given that borrowers need to receive a new mortgage, they will likely receive a new rate. If the new mortgage rate is higher, it's essential to understand if the higher rate outweighs the high-interest debt they will be saving on. However, with the decreasing mortgage rates in Canada, consolidating is likely a good idea.

- Administrative fees: These are the one-time fees that happen as you change mortgages. This accounts for things such as the cost of breaking your current mortgage and any legal fees involved. Furthermore, your home may need to be assessed, which will cost you money.

You'll want to consider these things, as well as any other circumstances that might come up to honestly know if refinancing your mortgage and reducing your de bt is the best option for you. If you want to know precisely how combining your debt with payments on your mortgage will affect you, you should consult with your bank or credit union first.

How to get approved for a debt consolidation loan

The big banks in Canada have the strictest lending criteria. They'll look at your credit score, income, monthly cash flow, and a variety of other variables when qualifying you for a loan.

Some lenders may be more flexible when assessing you for a HELOC. This is because many HELOCs only require interest payments every month. This decreases your monthly payments, which gives the lender more flexibility when analyzing your risk profile.

If you have bad credit, you'll have the best chance of being accepted for a second mortgage. Many private second mortgage lenders focus on customers with poor credit histories and lower credit scores. The downside is you’ll likely be charged a higher interest rate than a typical mortgage refinance.

However, there is no guarantee you'll qualify for a consolidation mortgage. Lenders assess many variables to determine your eligibility. This includes the appraised value of the property, how much debt you're seeking to combine into your mortgage, the amount of equity in the house, and your credit score.

Two downsides of consolidating debt Into a mortgage

There are several advantages to consolidating your unsecured, high-interest debt into your mortgage. This could reduce your monthly bills by a few hundred dollars throughout your loan.

It also has disadvantages, such as:

- You may run out of equity: Some folks perceive their home as a resource that they may draw on at any time. They'll begin treating their home as an ATM and withdraw equity for unessential things like a vacation. However, home equity isn't limitless. If you spend your equity, you can't access it when you need it.

- It does not fix the root problem: Some may not improve the financial habits that spiralled into high-interest debt. To get the best results from debt consolidation, you must make an effort to avoid racking up credit card debt again.

The Bottom Line

Debt consolidation is debt relief that consolidates debt into one monthly payment. Debt consolidation may be a great option for you because debt payments can be set up to be consistent and predictable. You also make one lower monthly debt payment instead of many like before. Additionally, you can also save money on interest!

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.