Debt Relief Canada

What You Should Know

- The government of Canada does not offer grants for debt relief directly.

- The government regulates debt relief programs that can help with debt management.

- The two insolvency proceedings regulated by the government are consumer proposals and bankruptcy.

- Other debt solutions are debt consolidation, debt management plan, and debt settlement.

You may have seen advertisements for Canada debt relief programs on social media; however, you should be aware that the government of Canada doesn’t directly offer these programs. Some companies may misrepresent their services as part of a government program. Therefore, you should carefully investigate a debt settlement company and verify its legitimacy before signing up for its program. Read below to find out about the debt relief solutions regulated by the federal government and those that are not.

Canadian Debt Relief Programs

The Canadian government does not give any grants for debt relief directly. However, the federal government’s Bankruptcy and Insolvency Act (BIA) regulates and monitors many debt relief services and their fees.

There are federally regulated professionals known as Licensed Insolvency Trustees (LITs) in Canada. LITs can provide financial advice to businesses and individuals with debt issues and are authorized to administer government-regulated insolvency proceedings. The two insolvency proceedings regulated by the government are consumer proposals and bankruptcy.

Licensed Insolvency Trustees

Licensed Insolvency Trustees (LITs) are federally regulated professionals who are authorized to administer consumer proposals and bankruptcies. LITs are licensed by the Office of the Superintendent of Bankruptcy (OSB) and are required to adhere to federal standards of practice. Their fees are also regulated by the federal government. You can find LITs through the Licensed Insolvency Trustee registry.

List of Top Rated Licensed Insolvency Trustees

| Name | Locations | Website |

|---|---|---|

| SPERGEL | AB, BC, ON, QC, MB, NS, SK | https://www.spergel.ca/ |

| MNP Debt | AB, BC, MB, NB, NL, NS, ON, PE, QC, SK, YT, NT | https://mnpdebt.ca/en |

| Grant Thornton Limited | AB, BC, MB, ON, NB, NL, NS, ON, PE, SK | https://gtdebtsolutions.com/ |

| Hoyes, Michalos & Associates | ON | https://www.hoyes.com/ |

Consumer Proposal

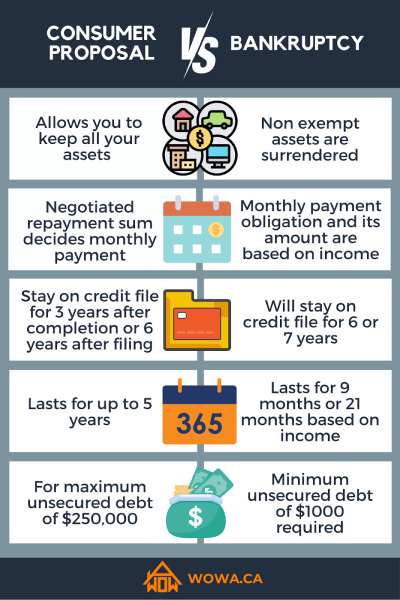

A consumer proposal is a legally binding debt settlement process in which a Licensed Insolvency Trustee (LIT) prepares a proposal on your behalf that offers your creditors to pay a percentage of what you owe, extend the repayment period, or both. The settlement amount is negotiated based on your income and assets. While you are likely to lose some of your assets in bankruptcy, a consumer proposal can reduce your overall debt and help avoid bankruptcy.

Once a proposal is filed with the Office of the Superintendent of Bankruptcy (OSB), you must stop paying your unsecured creditors directly. Meanwhile, any collection actions against you also stop, and no further interest is accumulated. The proposal is sent to your creditors, who get 45 days to accept or reject it. If the proposal is accepted, you must make a lump-sum payment or periodic payments to the LIT, which are used to pay your creditors and cover the fees related to the consumer proposal. Once the conditions of the proposal are met in full, you will receive a Certificate of Full Performance and be released from the debts in the proposal.

Consumer proposals can be administered when your total debt, excluding secured debt such as a mortgage, does not exceed $250,000. Consumer proposals have a maximum time duration of five years. Listed below are some of the advantages and disadvantages of a consumer proposal.

Advantages of Consumer Proposal

- Unlike in a bankruptcy, your assets will remain protected.

- Any ongoing collection actions against you, such as salary garnishment and lawsuits, will stop when the proposal is filed.

- Consumer proposals can help reduce debt, making monthly payments more affordable.

- You have to make only one monthly payment to the LIT instead of separate payments to your creditors.

- The monthly payment amount is fixed and will not increase even if your financial situation improves.

- Your debt will be repaid in 60 monthly payments or less.

- The effect on your credit score would not be as severe as bankruptcy.

Disadvantages of Consumer Proposal

- Your credit score will be hit, and the consumer proposal will stay on your credit file for a few years.

- There is a possibility that your creditors will not accept the proposal.

- Your credit cards carrying any balance will be cancelled.

- If you miss three consecutive payments, the consumer proposal will be annulled, and your creditors can take action against you.

Bankruptcy

Bankruptcy proceedings are usually the last resort and are used to provide debt relief to those who have no other way left to get out of debt. Similar to a consumer proposal, bankruptcies are legal proceedings facilitated by LITs. To file for bankruptcy, you must approach a LIT and fill out the required forms. Once the documents are filed with the OSB, you are declared bankrupt.

After you are declared bankrupt, you do not have to deal with your creditors directly, and the LIT deals with them on your behalf. Some key factors to note about bankruptcy are:

- The LIT sells your assets, and the proceedings from the sales are held in a trust by the LIT and used to pay your creditors. This means that you might lose some of your assets, such as real estate, jewelry, automobiles, and other possessions.

- During bankruptcy, you are required to report your income to the LIT every month and submit a copy of your paystubs and proof of income from other sources. You will have to make additional payments to the LIT every month if your income exceeds the threshold set by the OSB.

- All your credit accounts will be frozen during the bankruptcy proceedings.

- A first bankruptcy lasts for nine months when there is no surplus payment obligation and 21 months when there is a surplus payment obligation.

- Bankruptcy lasts on your credit file for six or seven years after being discharged from bankruptcy.

Emergency Debt Relief Programs in Canada

While you may have seen advertisements for emergency debt relief programs, there are no such programs offered by the government of Canada as of now. Such advertisements are often misleading and can also be linked to a scam. It is advisable to stay clear of any programs claiming to be government programs and promising you to provide debt relief quickly. You can verify the legitimacy of a company by directly contacting the government department responsible for running such programs.

Other Debt Management Solutions

Every person’s debt situation is different, and there are various debt relief solutions that may be suitable for different scenarios. You may be able to reduce some debt and manage it better using these solutions.

1. Debt Consolidation:

Debt consolidation is often the recommended first step in dealing with multiple debts. This process involves combining smaller debts into one large loan, often a personal loan with a lower interest rate.

This can be very helpful for individuals with multiple small debts with high interest rates, such as credit card debts and payday loans. You can combine these debts into a debt consolidation loan at a much lower interest rate. The total owed amount will remain the same, but your interest payments will significantly reduce. This will help you decrease the total amount to be paid in the long run and make it easier to manage all your debt.

2. Debt Management Plan (DMP):

A credit counselling agency can administer a debt management plan for you to pay off all your debt through a payment plan. The management plan involves an arrangement between you, your creditors, and the credit counselling agency where you pay a single monthly payment to the agency, which they then distribute to your creditors. There are several not-for-profit credit counselling agencies in Canada, and you can also contact a Licensed Insolvency Trustee for counselling. The following steps are involved in a DMP:

- Credit counsellors review your debt and decide whether a DMP is suitable for you.

- They then come up with an affordable monthly payment plan for you.

- The counsellors will contact your creditors on your behalf and ask them if they can reduce or eliminate the interest rate or fees on your debt and extend the repayment period.

- The plan starts once all the creditors have agreed.

It should be noted that credit counselling agencies generally don’t charge a fee for an initial consultation. However, they will likely charge you a fee for administering the DMP. A monthly administration fee is usually included in your monthly payments to cover the agency’s administrative costs. You may also have to pay other fees, such as an initial set-up fee, application fee, and membership fee. Typically, a debt management plan lasts 1 to 5 years.

Some creditors may not agree to a debt management plan. In such a case, those creditors will be left out of the debt management plan, and you will have to deal with them separately.

You can find an accredited counsellor near you through national and provincial association websites, such as Credit Counselling Canada (CCC). Listed below are some not-for-profit credit counselling services available in Canada:

| Name of Agency | Locations | Website | Google Rating (As of July 2023) |

|---|---|---|---|

| Credit Counselling Society | ON, BC, AB, SK, MB, NL | https://nomoredebts.org/ | 4.9 / 5 (61 reviews in Toronto) |

| Credit Canada Debt Solutions | ON | https://www.creditcanada.com/ | 4.9 / 5 (307 reviews in Toronto) |

| Money Mentors | AB | https://moneymentors.ca/ | 4.2 / 5 (48 reviews in Calgary) |

| Solve Your Debts | NB, PEI, NS, NF | https://www.solveyourdebts.com/ | 4.2 / 5 (6 reviews in Halifax) |

3. Debt Settlement:

If you are unable to manage your debt, you can try to negotiate with your creditors to reduce your debt. This is known as debt settlement. Most creditors expect you to pay a lump sum to settle the debt. This option may be used if you have savings or funds to pay the lump sum.

You can start negotiating with your creditors yourself or enroll in a debt settlement program offered by a private, for-profit company. A debt settlement may pose a few risks, such as:

- There is no guarantee that a settlement will work.

- You may have to pay fees to the settlement company even if your creditors don’t agree to a settlement.

Investigating a debt settlement thoroughly and reading the contract carefully before getting it is always advisable. Some types of debt may not qualify for a settlement, such as student loans, child support, or alimony.

A debt settlement will affect your credit scores and be noted on your credit file. The more debt the creditors write off, the higher the impact on your credit score.

Repayment Assistance Plan (RAP) For Student Loans

Repayment Assistance Plan (RAP) is a program by the federal government to help those who are unable to repay their student loans. The repayment assistance program allows you to make reduced or no payments at all for six months on the federal part of your student loan, depending on your affordability. You must apply every six months to remain eligible for the program.

If you are approved for RAP, the federal government pays the interest on the federal part of your loan that your monthly payment cannot cover for the first 60 months or 10 years after finishing school (whichever comes first). After this period, the government starts paying the principal part that the monthly payments cannot cover. You can be in repayment for a maximum of 15 years.

Borrowers with a disability can apply for a RAP-D. The government pays both the principal and the interest that the monthly payments cannot cover for those who qualify for RAP-D. A person with a disability can be in repayment for a maximum of 10 years.

You can apply for a RAP by filling out an online application through your National Student Loan Service Centre account or by completing a paper application.

Student Loan Forgiveness Programs

There are several federal and provincial student loan forgiveness programs available in Canada, including Loan Forgiveness for Family Doctors & Nurses, British Columbia Student Loan Forgiveness, Quebec Loan Remission Program, Saskatchewan Loan Forgiveness for Nurses and Nurse Practitioners, PEI Debt Reduction Grant Program, and Nova Scotia Student Loan Forgiveness Program. These programs are available for government student loans, not for private loans. The programs may have different qualification criteria, conditions, and incentives.

Frequently Asked Questions

Is Debt Relief Canada Legitimate?

No Canadian government programs directly give you money to pay your debt. However, there are two legal processes regulated by the government that can help you get out of debt — consumer proposal and bankruptcy.

What Is Debt Forgiveness?

Your creditors may forgive all or some of your debt if you are unable to repay it. This is called debt forgiveness. You have your debt forgiven; you can try to negotiate with your creditors, involve a settlement company, or follow a legal procedure such as a consumer proposal or bankruptcy. Following a legal procedure poses a lower risk.

Does Debt Relief Hurt Your Credit?

Yes. Debt relief solutions affect your credit scores. How much the score is affected depends on the solution you use. Different relief solutions stay on your credit file for different time durations. For example, a bankruptcy stays on your credit file for six or seven years, but a consumer proposal stays on your credit file for three years after completion or six years after filing.

Is There a Canadian Debt Forgiveness Program?

The Canadian government does not offer any grants to pay off debt. However, the government regulates some debt relief programs with the Bankruptcy and Insolvency Act (BIA). The two legally binding debt relief proceedings are consumer proposals and bankruptcy.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.