How to Buy a House in Quebec in 2026?

What You Should Know

- You need a financial foundation before buying a home in Quebec.

- Make sure to also budget for closing costs on top of your down payment.

- Get a mortgage pre-approval before working with a real estate agent.

- Expect to make many offers on homes in Quebec. Don’t get discouraged.

How to Buy a House in Quebec in 2026

Buying a house in Quebec has been made easier and more accessible. This is due to the changes that have recently occurred, such as the new mortgage rules for first-time buyers, which will be discussed later in this article.

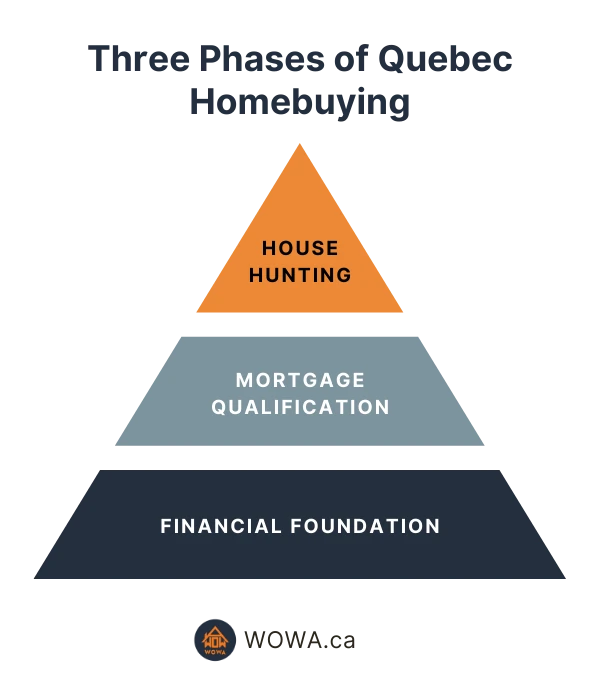

If you are ready to begin your journey to buying a home in Quebec, this article will provide you with step-by-step instructions. However, before you shop for homes, you'll need to build a solid financial foundation. The first three steps are focused on determining your financial situation and how much home you can afford.

Step One: Save For a Down Payment & Closing Costs

The average home price in the province of Quebec for June 2026 was $568,942. You can have a down payment of less than 20% with this purchase price if you get an insured mortgage. This means if you wanted to buy a home in Quebec at the current average price, you would only need a down payment of $113,788. Depending on the region you want to buy a home, your purchase price will change. Take a look at the table below to get an estimate of how much savings you'll need.

| Average Price (June 2026) | Estimated Down Payment | Total Savings Required (Including Closing Costs) | |

|---|---|---|---|

| Province of Quebec | $568,942 | $31,894 | $48,962 |

| Montreal | No data available | ||

To be able to make a down payment of less than 20%, you'll need mortgage default insurance. As a result, you'll need to meet all the CMHC mortgage insurance rules. You'll also need to pay for closing costs when finalizing a property purchase. Although this is explained more in step five, an estimate is included in the table above for reference.

Montreal Home Ownership Program

Montreal offers a lump-sum payment of up to $10,000 for eligible home buyers in the city. The lump-sum increases to $15,000 if you purchase property in a downtown Montreal region. However, the property will need to be newly built or renovated to receive the most significant payments. The program is known as the Montreal Home Ownership program and has a complete section in our Quebec Welcome Tax Article.

Step Two: Build Credit Score & Income Stability

Aside from the down payment, Quebec mortgage lenders also assess your risk profile as a lender. Two factors they look at are your credit score and income stability. A good credit score will provide you with more lending options and lower mortgage interest rates. At a minimum, your credit score needs to be above 600. However, the best rates are reserved for scores over 680.

Buying a House After Bankruptcy in Quebec

If you have declared bankruptcy in the past six years, don't worry. You may still be able to get a mortgage if you prove you have made significant strides to improve your credit score or have stable employment. However, if you don't want to wait the full six years for the bankruptcy to be removed from your credit report, you may be limited to B-lender mortgages in Canada.

Mortgage lenders also like to see that you have a stable income because it shows that you can afford your monthly mortgage payments. Lenders will also look at your debt service ratio, which is the amount of your monthly homeownership costs divided by your monthly gross income. If your debt-to-income ratio is too high, you may not be approved for a mortgage. If you're self-employed or a business owner, mortgage options are still available for you. You will have to learn more about self-employed mortgages.

Step Three: Check your Affordability

If you want to afford a more expensive home, the best options are increasing your income or decreasing your mortgage interest rate. To determine your maximum home affordability, Quebec mortgage lenders review your income compared to property taxes, mortgage payments, and home insurance. You can use a mortgage affordability calculator to estimate your maximum home purchase price.

Step Four: Determine Where to Buy

By now, you should have a rough estimate of the home purchase price you can afford and how much savings you'll need. Otherwise, ideally, you have a plan to reach this goal. Now that the foundation has been set, you can begin the exciting part of home hunting - deciding where to live! Below, we have a table to help you understand the differences between the top cities in Quebec.

| Montreal | Quebec City | |

|---|---|---|

| Description | Montréal is Quebec's largest city. It's located on an island and has many architectural styles,including Gothic revival, and French colonial. | Quebec City ages back to 1608. It's home to the famous Château Frontenac Hotel. You can find many boutiques and bistros along the Champlain district. |

| Population (5-year growth) | 4,277,000 (3.36%) | 836,007 (3.47%) |

| Property Tax Rate | 0.710320% | 0.998720% |

| Estimated Cost of Living (Monthly) | $2,400 | $1,933 |

| Walkability Score | Somewhat Walkable (65%) | Walker’s Paradise (94%) |

| Recommended Neighbourhoods |

|

|

Once you have a general idea of which city you like in Quebec, you can begin to narrow it down to some neighbourhoods. Some important factors that you should consider when selecting a neighbourhood include

- Commute Time

- Public Transit Accessibility

- Local Amenities (Groceries, Communities, Mall, Gym, etc.)

- Safety

- School Rankings

Also, remember Montreal offers the home ownership program. You can receive a lump-sum payment of up to $15,000 and a rebate on land transfer tax.

Step Five: Estimate Closing Costs

When you buy a home, you will have to pay additional costs to finalize the transaction. These are known as closing costs, which are due at closing and can't be included in your mortgage. Many people forget to calculate closing costs and are left in a bad situation. Make sure to budget around 3-5% of the property purchase price for these fees. Some of the closing costs include:

| Name | Description |

|---|---|

| Land Transfer Tax | Depending on where you buy a home in the province, you'll need to pay a tax ranging from a marginal tax rate of 0.5% to 4% of the home purchase price. Of course, Montreal offers a rebate on this cost through the home ownership program. You can use a calculator to estimate the cost. |

| Home Inspection Fee | In some cases, one or more inspections are required to ensure the property meets specific standards before closing. These home inspections range from $400 - $1200 depending on the amenities and location. |

| Surveying Fees | Surveying may be needed in cases of boundary uncertainty or older properties without recent surveys. |

| Mortgage Default Insurance | A small fee paid upfront by the buyer. This is required for down payments below 20% and protects the lender should buyers default on mortgage payments. |

| Title Search Fees | One-time search of public land registry to ensure there are no liens or encumbrances on the property. |

| Notary Fees | The notary is a lawyer who ensures that all legal aspects of the transaction are in order. |

| Appraisal Fee | A fee charged by an appraiser to estimate the market value of a property. |

| Legal Fees | Charged by the lawyer for drawing up the purchase contract and attending to all the legal formalities of the sale. |

These are some of the most common fees associated with a home purchase, but it's important to remember that each situation is unique. For a more detailed estimate, it's best to speak with a licensed Quebec mortgage lender.

Step Six: Mortgage Pre-approval

A mortgage pre-approval is when a lender agrees to give you a certain amount of money to buy a house. This shows that you are serious about buying a home and that the bank thinks you can afford it. It's essential to have this before meeting with a real estate agent because they will know that you are serious about buying, and they can start looking for houses within your price range.

Step Seven: Find a Good Real Estate Agent

Good ways to find a real estate agent are word-of-mouth, advertisements, active listings, and online platforms. Make sure to consider the following when talking to agents:

- Experience: Make sure the agent has experience in the market you are interested in.

- References: Ask for references from past clients and check them out.

- Negotiation Skills: The agent will be negotiating on your behalf, so make sure they have strong negotiation skills.

For a complete guide, you can visit our page on how to find a good real estate agent in Canada. The agent will then require purchasing criteria to find the best recommendations for you.

Step Eight: Determine your Purchasing Criteria

Now that you've determined your purchase price, neighbourhoods, and real estate agent, the next step is to figure out what you're looking for in a home. Be specific with your criteria. This will help your agent find the best home for your needs and avoid unproductive viewings. It's best to make a list of must-have and nice-to-have features. Some factors to consider include:

- Price

- Type and size of the house

- Bedrooms and bathrooms

- Age of the home

- Level of renovation needed

- Parking (driveway vs. garage)

Step Nine: Make Offers

When making conditional offers in competitive housing markets, including fewer terms is essential. For example, some buyers waive the need to inspect or appraise a property before buying. Other tactics to make a more competitive offer include:

- Increase the purchase price

- Increase the deposit

- Show proof of financing

- Attempt to close sooner

Don't be discouraged if your first offer isn't accepted. Expect to make many offers to finalize a deal. To learn more, you can read our guide on making an offer on a house.

Step Ten: Your Closing Date

Take a moment to appreciate the home buying journey! Congratulations on your significant purchase. Some considerations leading up to move-in day should be:

- Packing

- Moving truck rental or hiring a moving company

- Unpacking and organizing your new home

- Setting up utilities

- Changing your address with government institutions and other service providers

Making Friends in Quebec

Now that you've moved into a new home, an essential part of feeling comfortable is making local friends. There are many online resources to meet people with similar interests, including:

- Sports leagues

- Language exchange

- Local Facebook groups

- Meetup websites (such as meetup.com)

The Bottom Line

If you're looking to buy a home in Quebec, you must be well-prepared. In this article, we've provided some tips on what steps to take before meeting with your real estate agent and how they can help find the best house for your needs. Be specific about what criteria are most important for you, and make a list so that agents know exactly what type of property will work best for your situation. If all goes smoothly from there, then congratulations! You've found yourself a new place to call home!

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.