3-Year Variable Mortgage Rates

| Lender | Rates |

|---|---|

3-Year Variable Mortgage in Canada: Full Guide

This Page's Content Was Last Updated: 2022-06-01

What You Should Know

- 3-Year terms have a lower interest rate than 5-year terms.

- More Canadians started choosing variable-rate mortgages in Q1 2021.

- Short terms provide you flexibility, but you may need to renew at higher market interest rates.

- The best interest rates change by province, depending on local economics and regulation.

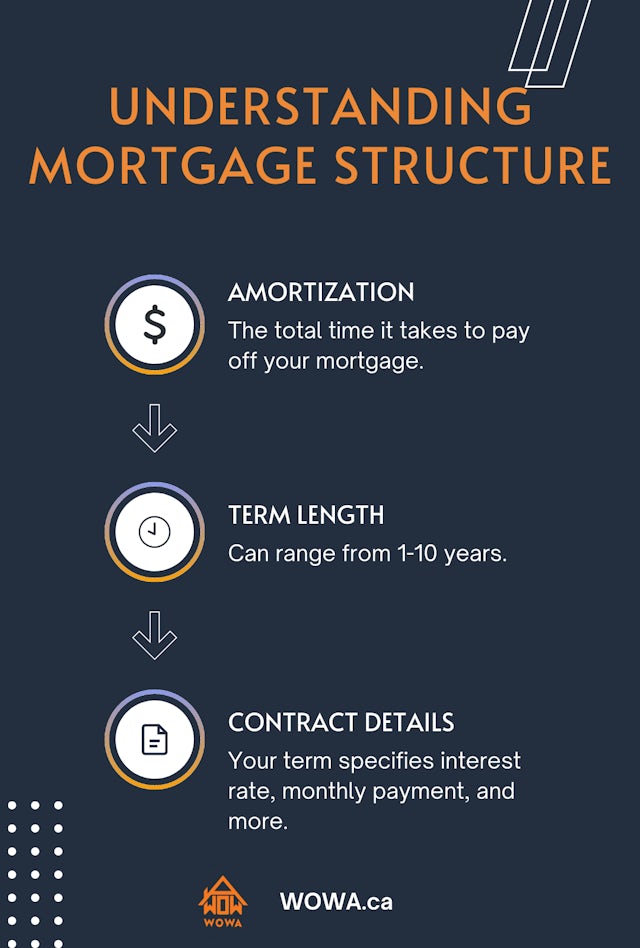

Your mortgage term is the amount of time you are guaranteed an interest rate, mortgage payment amount, and prepayment abilities. You can think of it as a sub-contract with your mortgage lender that details specific characteristics of your mortgage.

These characteristics are bound throughout your term life, and there are significant penalties for trying to change these characteristics by breaking your mortgage early.

At the end of your term, you must renew your mortgage. When renewing your mortgage, you have the opportunity to renegotiate these characteristics and lock them in with another term. Your term length dictates how long you are bound to these characteristics throughout your mortgage amortization.

Your mortgage amortization is different from your mortgage term. Amortization is the total amount of years you are expected to pay off your mortgage. It is the initial roadmap of when you'll be debt-free but can be extended through refinances, HELOCs and more.

You can think of your amortization as the outer shell which houses multiple terms throughout its lifespan. It is the terms that contain the finer details of your mortgage contract.

This article will show you the best mortgage rates and help you understand why you may want a 3-year term over the standard 5-year term. Additionally, it will compare fixed and variable terms to help you find the best mortgage solution.

3 or 5-Year Variable Mortgage

Residential Mortgage Funds Advanced (Fixed vs. Variable Rate)

In Millions, Uninsured Mortgages

Data taken from: Government of Canada Statistics

5-year mortgage terms are the standard length in Canada. They offer predictable payments and protection against rising interest rates for the first five years of your term. After the five years are up, your mortgage will be up for renewal, and the interest rate will be renegotiated.

The main advantage of a 3-year variable mortgage is the lower interest rate. The lender has less risk involved as the mortgage will be up for renewal sooner. Due to the short-term length, lenders are willing to offer a lower interest rate than a 5-year mortgage. As a rule of thumb, shorter mortgage terms tend to have lower interest rates. However, term lengths less than 1-year tend to have the highest rate.

The other reason Canadians choose a 3-year mortgage term is for flexibility. If you plan to pay off your mortgage or renew soon, then a 3-year fixed term may be better. As mentioned previously, there are penalties for breaking your mortgage term early. The penalties typically cost three months of interest, usually a few thousand dollars. Selecting a 3-year term will allow you to make significant changes to your mortgage sooner instead of waiting through a 5-year term.

However, the downsides of a shorter mortgage term include more frequent renewals and the possibility of renewing at higher interest rates. It's best to shop around at the end of your term to get the best interest rates. As a result, renewing more frequently means spending more time focused on your mortgage.

3-Year Variable or Fixed Rate Mortgage

| Variable Rate | Fixed Rate | |

|---|---|---|

| Pros |

|

|

| Cons |

|

|

A fixed-rate mortgage guarantees your interest rate throughout your mortgage term, while a variable rate fluctuates with the Bank of Canada interest rate. Variable interest rates are calculated as a surplus to your mortgage lender's prime rate. For example, if your lender's prime rate is 1.00%, they will add 0.50% to calculate your variable interest rate.

If the prime rate increases to 1.50%, your new mortgage rate will be 2.00%. This surplus is known as the spread and is negotiated based on your credit worthiness. Your spread will stay constant throughout your mortgage term even though the prime rate may change.

A common misconception with variable rate mortgages is that your monthly mortgage payment will change with the prime rate. This is not true. While your interest rate may change, your payment amount will remain fixed. When rates vary, it affects the percentage of each mortgage payment going towards the principal and interest.

For example, if your variable rate increases within your term, more of each payment will go towards interest. A lower percentage of each payment will be directed to your mortgage principal. As a result, you'll be behind your mortgage amortization schedule and may need to increase your mortgage payments in the next term to make up for the difference.

In an environment where interest rates are expected to increase, lenders will offer lower interest rates for variable mortgages. However, if rates increase, you'll pay more interest throughout your term. The choice between a fixed or variable-rate mortgage depends on your preference for stability or the allure of a seemingly lower rate.

Historical 3-Year Variable Mortgage Rates vs Fixed Rates

Historical Average Interest Rates (By Term Length)

For Newly Advanced, Uninsured Mortgages

Data taken from: Government of Canada Statistics

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.