3-Year Fixed Mortgage Rates

| Lender | Rates |

|---|---|

3-Year Fixed Mortgage in Canada: Full Guide

This Page's Content Was Last Updated: November 23rd, 2022

3-Year Fixed Mortgage

What You Should Know

- Canadians usually select a 3-year term when they expect rates to decrease in the future, but still want some protection from rising interest rates.

- Historically, shorter mortgage terms typically have a lower interest rate than longer terms, which was not the case in late 2022.

- You still need to pass the stress test using the higher of 5.25% and your mortgage rate + 2%.

- 30% of outstanding mortgages in Canada have a term length from three to less than five years.

Every mortgage has a combination of terms that will add up to your total amortization. You can think of a mortgage term as a sub-contract within your amortization that specifies your mortgage rate, prepayment penalties and more. The difference between mortgage term and amortization is that the latter is the total amount of time it will fully take to pay off your mortgage.

You'll have to renew your mortgage at the current market interest rate when your term is over. While a 5-year term is most popular, Canadians choose a 3-year term if they expect the mortgage prime rate to decrease or if they want to break their mortgage sooner. Continue reading to see the best 3-year fixed mortgage rates and when to get one.

Total Outstanding Balance of Fixed Rate Mortgages by Term Length

In Millions, Sourced August 2022, Only for Uninsured Mortgages

Data taken from: Government of Canada Statistics

Historical 3-Year Fixed Mortgage Rates

This chart of historical 3-year mortgage rates tracks the posted rates of Canada’s major banks: RBC, TD, BMO, Scotiabank, CIBC, and National Bank. Posted mortgage rates are used to calculate mortgage break penalties, which is the fee that you pay when you break your mortgage. It’s also used as the Qualifying Rate for the mortgage stress test by the CMHC.

Lenders often have discounted mortgage rates that are lower than their posted rates. Some lenders also offer cashback incentives, or offer promotional rates to new clients. However, these promotions are usually temporary, and they may only apply to prime borrowers.

3 or 5-Year Fixed Mortgage

As mentioned previously, your mortgage term is a sub-contract with your lender. It details your interest rate, monthly mortgage payment, prepayment abilities and more. You will be locked into this contract for your term duration.

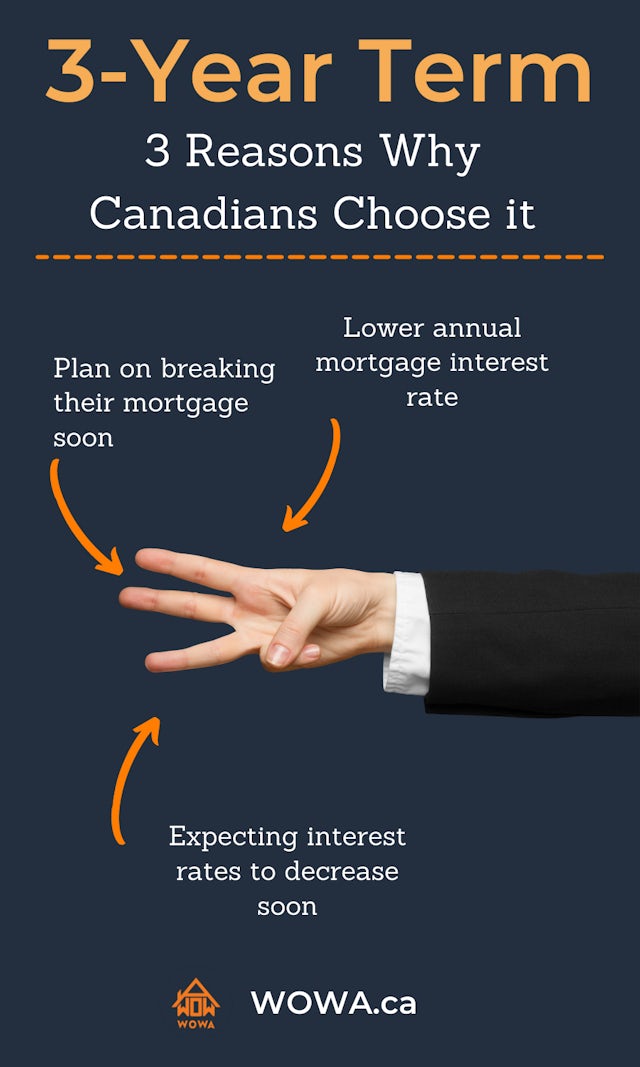

While you can break a mortgage in Canada, it comes with significant penalties. You can renegotiate the details with your lender when your term ends or switch to another lender altogether. There are three reasons Canadians choose a 3-year mortgage over the standard 5-year term.

| 3-Year Term | 5-Year Term | |

|---|---|---|

| Pros |

|

|

| Cons |

|

|

- Lower mortgage interest rates

- Expecting interest rates to decrease soon

- Want to break their mortgage in three years

Over the past decade, 3-year mortgages have typically had a lower annual interest rate than 5-year terms. Typically, the rates are 0.2% to 0.4% lower. This gap has narrowed recently, and in late 2022, the relationship has even reversed itself, with lenders having 3-year rates that are higher than 5-year rates. Even so, during normal periods where 3-year rates are lower, the discount that you get with a 3-year mortgage term can still be significant enough that it could make a difference in your monthly mortgage payments.

For example, with a $500,000 mortgage opting for a 3-year term at a lower interest rate of 3.89% would result in a monthly payment of $2,713. However, with a higher 5-year interest rate of 4.19%, your monthly payment would be $2,800. This would equate to $1,044 after one year or $3,131 after three years. However, if rates increase, you'll have to renew into larger payments sooner.

If you expect interest rates to decrease shortly, choosing a shorter term could allow you to renew at lower market interest rates. However, if you miscalculate, you could be forced to renew at higher interest rates.

The general mortgage rule of thumb is to choose shorter terms when you expect rates to drop. The opposite is true when you expect rates to increase. With rising rates, it's generally advised to lock into today's lower interest rates for a longer 5-year fixed, 7-year fixed, or even 10-year term.

There are penalties for breaking your mortgage early. In many cases, the penalty is three months' worth of interest. This usually amounts to a few thousand dollars. If you plan to make significant mortgage payments or move to another country before your term ends, you'll have to pay the penalties.

However, if you time this with your term expiration, there will be no penalties. For example, if you expect to inherit money within the next few years, a 3-year term could be better for you. This is because you'd have the option to contribute the income to your mortgage without penalties.

If you selected a 5-year mortgage, you'd have to pay additional interest while waiting two years to avoid penalties. It is not necessary to time your term with moving homes within Canada because you have the option to port your mortgage.

Have Mortgage Rates Inverted?

In recent months, something strange has happened in the world of mortgage rates. The yield curve has actually inverted, with shorter-term mortgage rates now higher than longer-term ones. This is unusual because it goes against the usual trend. So what's causing this inversion?

Usually, shorter mortgage terms will have a lower interest rate compared to longer mortgage terms. If graphed as a line, this would be an upward-sloping curve. The same thing happens with government bonds. The yield of bonds usually increases the longer the time to maturity is. This happens because investors require a higher return to tie up their money for a longer period of time.

Average Mortgage Rates for All Lenders on WOWA.ca

| 1-Year | 2-Year | 3-Year | 4-Year | 5-Year | 6-Year | 7-Year | 10-Year | |

| Mortgage Rates | 5.95 | 5.89 | 5.69 | 5.69 | 5.52 | 6.16 | 6.23 | 6.68 |

| Bonds | 4.5 | 4.19 | 4.14 | 3.83 | 3.67 | - | 3.5 | 3.47 |

Note: Rates shown are the average mortgage rates from all lenders on WOWA.ca, for insured mortgages with a 25-year amortization. Yields shown are Government of Canada bond yields. Updated November 2022.

Mortgage rates follow bond yields. In 2022, Canada’s yield curve inverted, with short-term government bonds having a higher yield than long-term government bonds. This was also reflected partially in mortgage rates. The mortgage rate curve remains normal for terms longer than five years, even though it is inverted for terms between one and five years.

Average Mortgage Rates for Canada’s Six Major Banks

| 1-Year | 2-Year | 3-Year | 4-Year | 5-Year | 6-Year | 7-Year | 10-Year | |

| Mortgage Rates | 6.02 | 5.97 | 5.77 | 5.74 | 5.6 | 6.38 | 6.42 | 6.62 |

Note: Rates shown are the average mortgage rates for RBC, TD, CIBC, Scotiabank, BMO, and National Bank, if offered, for insured mortgages with a 25-year amortization. Yields shown are Government of Canada bond yields. Updated November 2022.

An inverted yield curve could be a sign for an impending recession. This may cause interest rates to fall in the future. With short-term mortgage rates being higher than 5-year fixed mortgage rates, it may point towards some expectation of rates falling in the next few years. However, it might also be due to intense competition among Canadian mortgage lenders to offer the best 5-year mortgage rates. That’s due to the popularity of 5-year mortgages in Canada.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.