Budget Calculator for Canadians

Monthly Income vs. Expenditure

You are within budget! Your income is more than your allocated expenses and savings.

Breakdown of Expenses

About this Calculator:

- This budget calculator is designed to help you devise a monthly budget based on your current gross income, your expenses across 11 different categories, and your savings and investments.

- The calculator evaluates how your income compares with your expenses, and calculates the surplus or deficit in income in relation to your expenses.

- You can also review the percentage breakdown of your expenditure in the results section. This can help you make adjustments in your expenditure in order to reach your financial goals.

What Is a Budget?

A budget is a spending plan created on the basis of an approximation of income and expenditure over a certain period of time. A budget is used not only by individuals and families, but also by companies, organizations and governments.

According to the Bank of Canada’s Survey of Consumer Expectations in Q4 - 2023, Canadians are cutting their spending in response to high inflation and interest rates. Meanwhile, monthly mortgage payments are set to increase for many mortgages that are coming up for renewal, and further spending adjustments will likely be required. This makes keeping a tab of where your money comes from and where it goes all the more important.

Individuals and families can create a monthly budget to keep a track of their expenses and ensure they are not spending more than they are earning. Having a budget can also be helpful in meeting short-term and long-term financial goals, building an emergency fund, saving for retirement or even paying off debt.

How to Budget?

The basic requirements for creating a budget are knowing your after-tax income and knowing where and how much of your money goes. There are several popular budgeting methods that can be used to create a budget template. You can select the method that is most suitable for your situation. You can also use these methods as a baseline and create your own budgeting method to suit your needs.

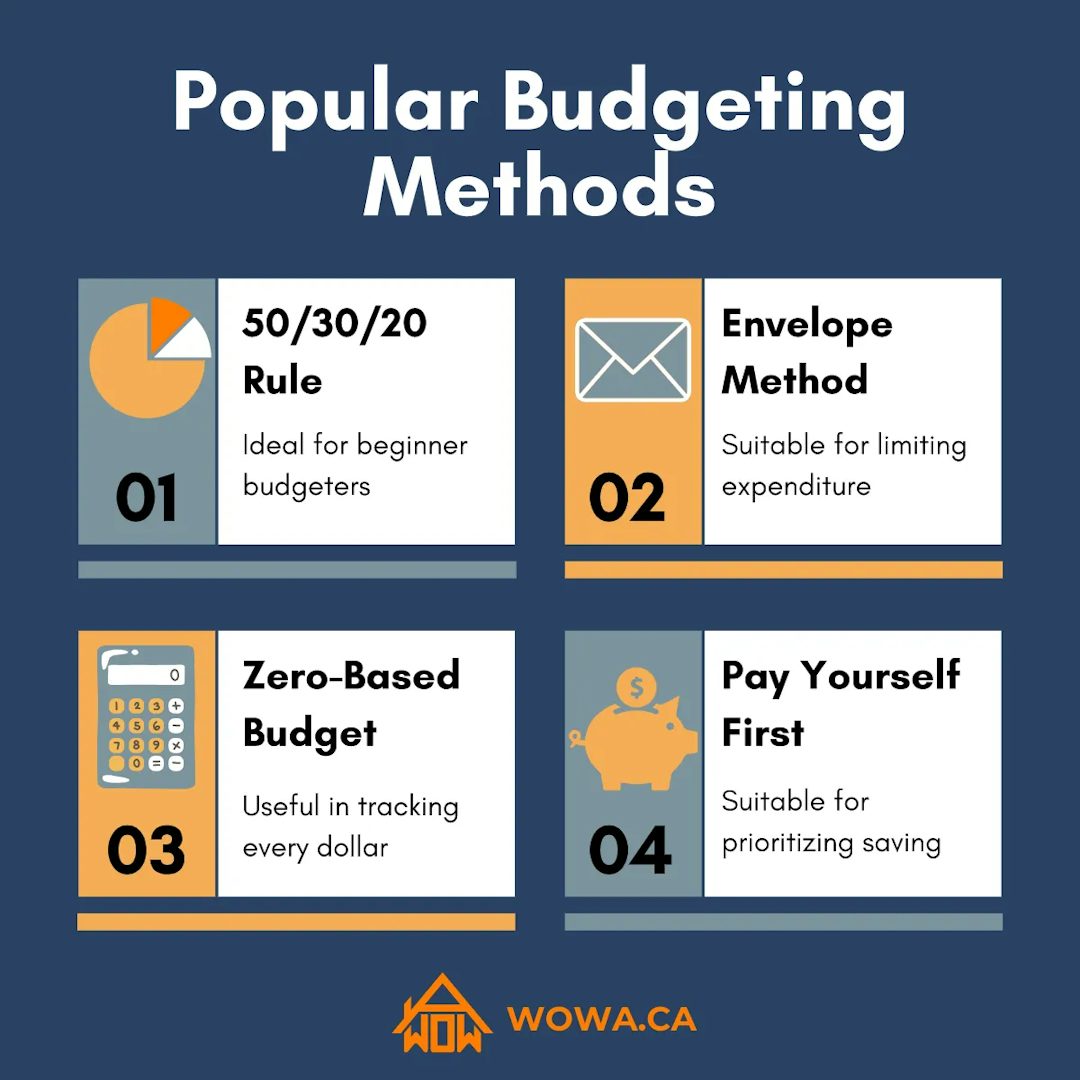

Listed below are four of the most commonly used budgeting techniques that you could use to create a budget for yourself and your family.

- 1. 50/30/20 Rule - Good for beginners

The 50/30/20 budget rule suggests breaking down your income into three categories – needs, wants and savings. It recommends allocating 50% of your income for your essential expenses (needs) such as mortgage or rent, groceries, transit expenses, insurance and utility bills. 30% of your income is suggested to be allocated for non-essential expenses (wants) such as eating out, going to movies and vacations. 20% of the income is recommended to be allocated for savings, such as in RRSP (Registered Retirement Savings Plan) or TFSA (Tax-Free Savings Account), investments and paying off debts.

This is a very simple and straightforward budgeting method that even beginners can use. You can easily divide your expenses in the three categories, which can make it easy to track them. This rule can also be used as a baseline to create your own budget method, especially if you live in a city with a high cost of living, such as Toronto or Vancouver, where the housing cost alone can account for almost 40% - 45% of your budget.

- 2. Envelope Budgeting - Good for setting a spending limit

This is a cash based system of budgeting that can help you limit your spending. For this method, you need to take a bunch of envelopes and label them as per spending categories including essential expenses such as gas and groceries, and non-essential expenses such as shopping, dining-out etc. Along with these, you should also make separate envelopes for savings such as an emergency fund and retirement savings.

Once you have all the envelopes, you must allocate a percentage of your take-home pay into them at the beginning of the month. Every time you need to buy something, you must withdraw cash from the respective envelope only. Anything that’s left in the envelopes can either be added to savings or rolled -over to the following month. This method is a great way to curb overspending and can work well for individuals who struggle to save.

In today’s day and age where payments have become cashless, the envelope method might sound outdated. However, you could try replicating the envelope method digitally by having separate bank accounts for different spending categories.

- 3. Zero-Based Budgeting - Good for tracking every single dollar that you spend

To make a zero-based budget, you need to make a budget for the upcoming month based on the expenses of the past few months, and then adjust the budget in a way that your income minus the budget amount equals zero.

To get started, you can list out all the expenses such as rent, groceries, utilities, dining-out, etc in order of priority. Be sure to add savings to this list. Once you have the list, start putting a number next to each item that you expect to spend in the upcoming month. This should be fairly straightforward for fixed expenses such as rent and some bills; however, for others, you may need to make estimates based on your past spending. Now you must subtract all these expenses from the pay you expect to receive in the next month after deducting the income tax. The result should be zero. If it isn't, go back and make some adjustments to your expenses so that you get zero as a result.

This method can be time consuming, but can help you track your expenses down to every dollar. As you start doing this at the beginning of each month, your estimates will get better. Use our budget calculator to save time and track your expenses accurately.

- 4. Pay Yourself First - Good for growing your savings

This method prioritizes savings over everything else. The first thing you do is decide how much of your monthly after-tax income you want to save every month (experts recommend at least 20%). When you receive your paycheck every month, set aside the predetermined amount for savings first, then use the remaining money to take care of your basic expenses such as rent and utilities. Whatever is left after that is what you can spend as per your wish.

Setting up an auto-pay on the day that you receive your pay in your bank account can be an easy way of doing this. You could save in a high-interest savings account or invest in government bonds, bank stocks, dividend stocks, GICs (Guaranteed-Investment Certificates), ETFs (Exchange-Traded Funds), mutual funds, and more. If your priority is to save or to grow your net worth, but you do not have time or patience to sit and make a detailed budget, this is the method that you could follow. It is fairly simple and straightforward and takes care of your savings and essential expenditures.

Bottom Line

Being on a budget does not mean depriving yourself of enjoyment and all the good things in life. It simply means having a better understanding of your expenses and keeping a track of them. You don’t need to be good at math to be a proficient budgeter, all you need is to be aware of where your money comes from and where it goes. You could get budgeting with one of the techniques listed above or invent a budgeting method of your own to suit your needs.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.