Canada 10-Year Bond Yield

What You Should Know

- Bond yield is the return a bondholder should receive if they hold the bond until maturity.

- Canada 10-year bond yield is used as a basis for 10-year loan term interest rates.

- Interest rates are usually higher than government bond yields for the respective term because Government bonds, including Canada 5-year bonds and Canada Savings Bonds, are considered risk-free.

Recent Canada 10-Year Bond Yield:

3.58%

Canada 10-Year Bond Yield Overview

Canada 10-Year Bond Yield Historical Data

Current 10-Year Bond Yield has been highlighted.

| Date | Value |

|---|---|

2026-07-29 | 3.58 |

2026-07-28 | 3.53 |

2026-07-27 | 3.56 |

2026-07-24 | 3.6 |

2026-07-23 | 3.65 |

2026-07-22 | 3.6 |

2026-07-21 | 3.56 |

2026-07-20 | 3.57 |

2026-07-17 | 3.56 |

2026-07-16 | 3.53 |

What are Bond Yields?

Bond yield is the return when purchasing a bond. Any type of bond, including government and corporate, has a certain yield or return. Government of Canada bonds and Canada Mortgage Bonds (CMBs) are considered risk-free bonds because they are issued by the government and are denominated in domestic currency. These bonds will always be paid back since the government has the power of taxation and other sources of income for the currency bonds are denominated. When it comes to Canadian bonds, the Bank of Canada can loan funds to the Canadian government to cover the bond payments. Even risk-free bonds usually have a positive yield, which means a holder of that bond is able to get a return on it.

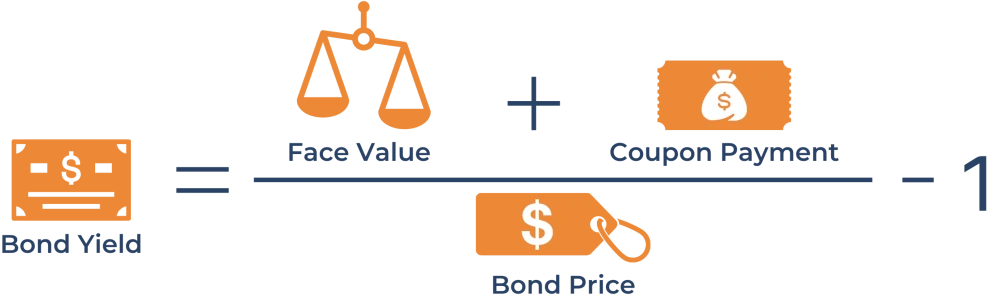

Depending on the coupon structure, the yield on a bond may be calculated differently. The simplest formula for finding a bond yield is as follows:

The yield calculated in this way is called a current yield. You could also divide the coupon payment by the face value of the bond in order to drive the coupon yield. When it comes to government bonds, also known as sovereign bonds, their bond yields usually indicate the expected inflation rate among investors. It is important to note that the bond's price affects the bond yield. This means that if the price of the bond increases, the buyer will have to pay more to get the same payout, which leads to a lower bond yield.

Bond maturities usually range between 1 and 30 years. Government debt securities that mature in less than a year are called treasury bills or t-bills. The 10-year bond yield is often used as a benchmark for setting interest rates on 10-year loans. In addition to that, investors and analysts may use 10-year bond yields in conjunction with bond yields of other maturities to assess the state of the economy. More specifically, they look at the yield curve that represents different yields for bonds of different maturities. Since the yields are affected by the sentiment of buyers, the yield curve can provide an insight into the investor's economic expectations. Usually, the yield curve has a positive slope. When the slope of the yield curve is negative, it means that the yield on short-term bonds is higher than the yield on long-term bonds. Many investors see a negatively sloped yield curve as a sign of an upcoming recession.

Positively Sloped Yield Curve

Negatively Sloped Yield Curve

How Do Bond Yields Affect Interest Rates?

Interest rates on most financial lending products are higher than bond yields for the respective term length. When creditors and lenders sell you a mortgage, car loan at various car loan rates, or some other product, they take on a certain amount of risk because you could default on your mortgage or you could end up repaying the mortgage early.

By lending you money, they give up the option of buying risk-free bonds which would have been default-free. Creditors and lenders will add a risk premium to compensate them for the risks associated with lending you money.

For example, let’s say you want to borrow $500,000 to buy a new house, so you ask the bank for a 10-year mortgage loan. The bank could either give you $500,000 or they could buy $500,000 worth of government bonds. Since government bonds are risk-free, all else equal, banks will prefer to buy risk-free bonds rather than lend you money. Most Canadian mortgages have prepayment privileges ranging from 10% to 20% of the mortgage principal per year. Borrowers can make prepayments less than their prepayment privilege without paying a mortgage prepayment penalty. Generally, prepayments increase when interest rates fall, so the lender cannot get the same interest payments as before. So to compensate the lender for this risk, you will be charged a higher interest rate.

The BoC auctions government bonds to the financial market distributors and dealers on behalf of the Government of Canada. This initial auction is the primary market for government securities. These distributors and dealers would sell these securities to their clients over the counter (OTC). These over-the-counter trades constitute the secondary market for government bonds.

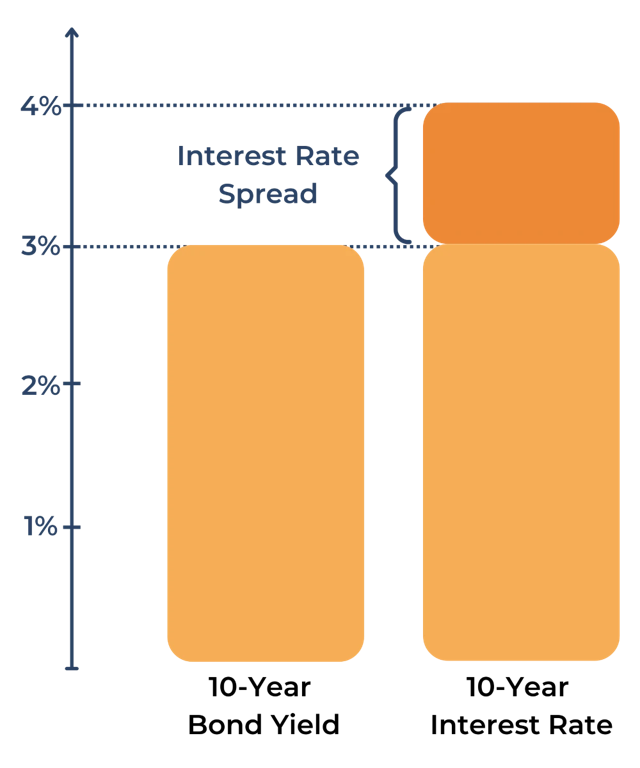

Since interest rates on financial products are directly tied to bond yields, if a 10-year bond yield increases, 10-year loan interest rates increase as well. There are also personal risk factors that may affect a personal interest rate quote. For example, a person with a lower credit score will likely receive a higher interest rate than someone with a higher credit on the same loan. The difference between the 10-year government bond and interest rate is called the interest rate spread. Creditors and lenders are typically inclined to increase interest rates faster when bond yields rise to lower their exposure to the volatility of bond yields, which means that interest rate spread increases during uncertain times.

Interest Rate Spread

The interest rate for any financial product usually follows the bond yields. This means that when bond yields increase, the interest rate tends to increase while a decrease in the bond yields usually leads to a decrease in the interest rate. Generally, this spread is within the range of 1% and 3%, and it represents the risk premium. Since this spread is based on the risk premium, it can increase during times of uncertainty.

For example, at the beginning of the Coronavirus pandemic, lenders briefly increased interest rates because default risk increased. A low interest-rate spread can be usually seen during stable times when an economy is growing and bond yields are low. As the bond yields increase, the spread may increase and stay increased for some time.

For reference, the table below shows the recent 10-year fixed mortgage rate spread that experiences an increase as the 10-year bond yield increases.

| Last Seen | 10-Year Canada Bond Yield | 10-Year Mortgage Rate Estimate | Spread |

|---|---|---|---|

| January 2022 | 1.7800% | 3.84% | 2.0600% |

| January 2021 | .8055% | 2.14% | 1.3345% |

| January 2020 | 1.4923% | 2.99% | 1.4977% |

10-Year Bond Yield Forecast

The most important interest rate in the Canadian economy is the overnight interest rate. Lending in the overnight market is collateralized with government bonds. Thus overnight lending is almost as secure as purchasing government bonds.

In principle, investors are indifferent to lending money in the overnight market or purchasing 10-year government bonds. Thus the yield on 10-year government bonds should reflect the average yield in the overnight market over the next 10 years.

In the middle of June 2023, the overnight rate is 4.75%, and 10-year government bonds are yielding 3.4%. Normally bond yields are higher than overnight yields as they have a term premium. The term premium is the compensation that investors demand for bearing the risk that interest rates might rise while they are holding the bond.

The point that the overnight rate is higher than the bond rate means that the overnight rate is expected to come down and average significantly below their current level.

To estimate the long-term level of the 10-year bond yield, we can consider the Bank of Canada’s estimate of the real neutral rate between 0% and 1%. We can add the target inflation rate of 2% to this number and assume a term premium of 0.5%. This suggests we should expect the 10-year yield to settle between 2.5% and 3.5%.

The 10 year yield has been within this 2.5%-3.5% range since March 2022. Yet the 10 year yield was below this range between 2011 and 2022. The period between 2011 and 2022 is sometimes referred to as financial repression. It is referred to as financial repression because savers could hardly earn any interest on their savings. This was because of Western central banks' decision to print large quantities of money and set their policy rates very low.

There were some structural factors in the global economy that allowed Western central banks to keep rates so low. These factors included large quantities of savings, few investment opportunities and production overcapacity in the world economy and continuation of the peace dividend.

Changes in demography are reversing some of these factors, and the peace dividend is being substituted with a war tax.

After the dissolution of the Warsaw Pact and, the more importantly soviet union itself, most Nato members reduced their military spending. This money which was no more spent on the military, was called a peace dividend. But recently, Nato members' military spending has again risen to fight Russia in Ukraine and deter China in Taiwan. We might call this added spending a war tax.

Thus we view the past 15 years as an abnormal time in economic history. Over the coming years, we expect the 10 year yield to fluctuate around the 3.5% rate.

How Are Bond Yields Determined?

Bond yields are the annualized returns on Government of Canada bonds. This includes the coupon payments (the bond’s interest rate) and the returns you receive from any changes in the bond's market price.

The coupon rate listed on a government bond is not what the investor receives. Instead, this rate is divided by two and, every six months, the investor receives this as a semi-annual coupon payment. The coupon payment remains fixed throughout the lifetime of the bond, however, changes in the market price of the bond can also affect returns.

If the market price of the bond is greater than the face value, then the bond yield will be lower than the coupon rate, and if the market price is less than the face value, the bond yield will be higher than the coupon rate. The most simplistic formula for finding a bond yield assumes that the face value of the bond and the price of the bond are the same. Most of the time, the face value of a bond and its price are different, so you may need to use a more general formula that should work for most bonds.

Yield to maturity gives the rate of return for a fixed income instrument. Yield to maturity (YTM) is the rate of return that equates the present value of all cash flows from a bond to its current price. In other words, YTM satisfies the following formula:

P - the price of the bond.

t - stands for time, it takes on length of time intervals from now till each coupon payment and the principal payment.

Cash Flow the payment a bond makes at time t.

YTM - Yield to maturity.

This formula cannot be solved analytically for YTM. Instead it is quite straight forward to implement a numeric solution in an spreadsheet.

How are Government of Canada Bonds Issued?

Government of Canada bonds are issued during bond auctions, where large banks and financial institutions buy them. The bonds have fixed face values, terms, and coupon rates, which banks and financial institutions bid on.

Primary dealers or government securities distributors are institutions that are authorized to bid during Government of Canada bond auctions. Some examples of primary dealers are RBC, TD, Scotiabank, CIBC, BMO, HSBC, Desjardins, and National Bank. Once these institutions buy the bonds, they resell them to clients, so the prices you have to pay for government bonds are set by primary dealers.

If buyers on the primary market think the coupon rate on a bond is too low for current market conditions, they might only be willing to pay $99 for a bond with $100 face value. On the other hand, if the coupon payment is generous, they might be willing to pay $101 for it. This is where the bond prices come from that are used to calculate yields.

Primary dealers determine if the coupon rates on bonds are enough to compensate them for other opportunities. Just as the opportunity cost of lending is government bonds, the opportunity cost of government bonds is lending and investments. If markets are thriving, the banks and financial institutions will demand a higher coupon payment, or the price of the bond will drop.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.