TFSA Contribution Room Calculator 2026

Calculate how much you can contribute to your TFSA:

TFSA Contribution Room 2024

The TFSA contribution limit for 2024 is $7,000. For 2023, the contribution limit was $6,500. If you were born in or before 1991, you can contribute up to a total of $95,000 to your TFSA. Those born after 1991 will have a smaller total contribution limit. Unused TFSA contribution room rolls over from one year into the following year.

A Tax-Free Savings Account (TFSA) is a registered investment account first introduced in Canada in 2009. TFSA lets individuals 18 years or older with valid social insurance numbers (SIN) invest up to a certain amount each year, without having to pay taxes on the earnings on those investments. Through this account, you can invest in stocks, bonds, exchange-traded funds (ETFs), mutual funds, and more.

TFSA Contribution Limits 2009 - 2024

| Year You Turned 18 | Annual Contribution Limit | Cumulative Contribution Limit |

|---|---|---|

| 2025 | Unconfirmed: $7,000 | |

| 2024 | $7,000 | $7,000 |

| 2023 | $6,500 | $13,500 |

| 2022 | $6,000 | $19,500 |

| 2021 | $6,000 | $25,500 |

| 2020 | $6,000 | $31,500 |

| 2019 | $6,000 | $37,500 |

| 2018 | $5,500 | $43,000 |

| 2017 | $5,500 | $48,500 |

| 2016 | $5,500 | $54,000 |

| 2015 | $10,000 | $64,000 |

| 2014 | $5,500 | $69,500 |

| 2013 | $5,500 | $75,000 |

| 2012 | $5,000 | $80,000 |

| 2011 | $5,000 | $85,000 |

| 2010 | $5,000 | $90,000 |

| 2009 or Earlier | $5,000 | $95,000 |

How to Check TFSA Contribution Room?

Each year, you can contribute up to a fixed amount to your TFSA. This limit is commonly called the annual contribution room or contribution limit. If you don't contribute the maximum amount for that year, you need not worry because your TFSA contribution room is cumulative. Your leftover contribution room will be carried forward to the next year. You can deposit up to your lifetime contribution limit or withdraw as much as you like, and your total contribution room will stay the same.

You can check the CRA's website or manually calculate your TFSA contribution room. If you are using the CRA’s website, follow the steps below:

- Login using the CRA's login portal.

- Scroll down to the "RRSP and TFSA" section and click "Go to RRSP and TFSA details.”

- Your contribution room for the current year will be displayed, and you can view additional information using the "View TFSA details" link. Note that the contribution room listed here does not account for any transactions made this year. To find your updated remaining contribution room, you can call the CRA directly or perform a manual calculation.

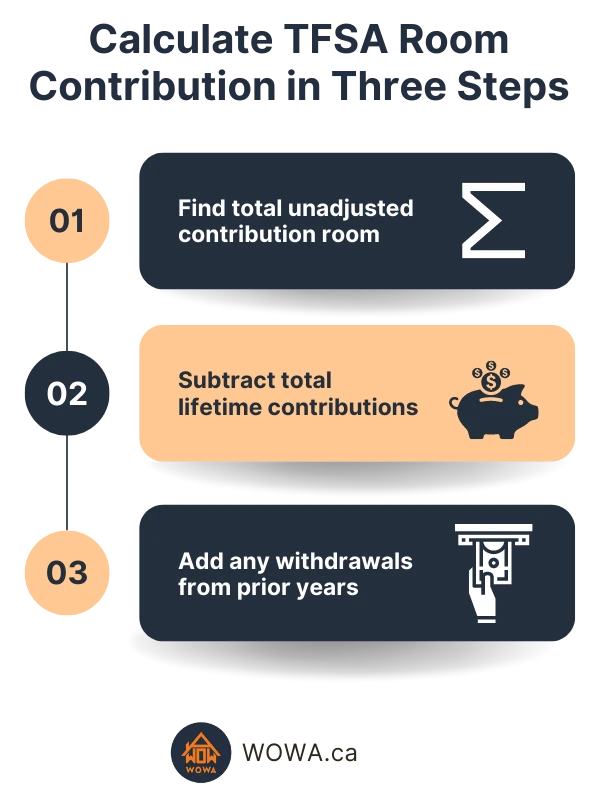

How to Calculate TFSA Contribution Room?

Calculating your TFSA contribution room yourself is simple. The most challenging part is gathering your past contributions and past withdrawals. You can calculate the TFSA contribution room manually using the steps below.

Step 1: Find your total unadjusted contribution room by using the annual contribution limits table to add up the annual limits for each year you were at least 18 years old.

Step 2: Subtract any contributions you have ever made to your account. Even if you later withdrew the money, adding them all here will simplify the calculation.

Step 3: Add any TFSA withdrawals you have made before 2024. You cannot add any withdrawals made in 2024, as you cannot recontribute this amount this year.

The final amount you get from the above calculation is your available contribution room for 2024.

TFSA Withdrawal Rules

While making a withdrawal from your TFSA, keep the following in mind:

- As long as you maintain a positive balance, you can withdraw any amount from your TFSA without penalties or taxes.

- The amount withdrawn in a year can only be re-contributed in the following years.

- Any additional contributions can only be made using up to the total contribution room available before the withdrawal. You shouldn’t consider withdrawals made this year in this year's total contribution limit, or you may end up over-contributing.

- If you earn any investment income or capital gains, you can withdraw this amount without affecting your total contribution room.

For example, assume your total contribution limit is $6,000, and your TFSA account has $2,000 in it. Your available contribution room for this year would be $4,000 ($6,000 - $2,000). Let's say you withdraw $1,000. Then, your available contribution room for this year would still be $4,000, and not $5,000. If you decide to re-contribute $1,000 this year, your remaining contribution room will be $3,000 ($6,000 - $2,000 - $1,000).

Example of Withdrawing TFSA Earnings

Suppose you have an available contribution room of $4,000, and you have earned $500 on the investments already in your TFSA. If you do not withdraw this $500, your contribution room remains $4,000. If you decide to withdraw this $500, your contribution room remains at $4,000, but you can contribute an additional $500 next year.

TFSA vs. RRSP Contributions

While both TFSA and RRSP give you tax benefits, you still need to pay tax with both types of accounts. Just the timing of when the taxes are paid will be different.

TFSA: With the TFSA, you contribute your after-tax earnings to the account. However, you will not need to pay tax when you withdraw your profits. With a TFSA, you pay income tax in the present, so you don't have to pay tax in the future.

RRSP: An RRSP is the opposite; you don't pay tax in the present, so you will need to pay it in the future. Contributions to your RRSP are deductible from your income tax, so you can think of it as your pre-tax income. However, when you need to withdraw from your RRSP, you must pay tax. This is unless you are a first-time homebuyer using the RRSP Home buyers' Plan (HBP). The HBP allows first-time homebuyers to withdraw up to $60,000 tax-free from their RRSP to fund a down payment, which must be re-contributed to their RRSP within 17 years.

The newly proposed First Home Savings Account (FHSA) combines the best of a TFSA and RRSP. You receive an income tax deduction on contributions, and withdrawals are tax-free if used to purchase a home.

Should You Contribute to TFSA or RRSP?

Generally, it's advisable for younger people to focus contributions on their TFSA. This is because their income is expected to increase over time. By paying taxes when their income is lower, they will not need to pay taxes on withdrawals when their income is higher.

RRSP focus is generally advised for those in the peak earnings of their career. The deductions offset their income taxes, and they can withdraw the profits when they are typically in a lower income tax bracket after retirement. However, with the RRSP Home Buyers' Plan, contributions are also great for younger people looking to buy a home. You don't pay tax on contributions or withdrawals to finance your down payment with this program.

TFSA Over-Contribution Penalty

If you end up contributing more than your total contribution room, the Canada Revenue Agency (CRA) will charge you a monthly fee of 1% on the highest excess TFSA amount for that month. A 1% fee may sound small, but this is equivalent to 12% each year, which is massive! For example, a $10,000 over-contribution would cost you $1,200 per year.

Excess TFSA Amount = Total TFSA Contributions - TFSA Contribution Room

Since the TFSA uses the highest excess TFSA amount, you will have to pay the full 1% fee even if you are over-contributed for just one day.

Avoiding the Over-Contribution Penalty

Keep track of any contributions and withdrawals you make and keep a record to ensure you do not over-contribute. If, at any point, you are unsure about how much contribution room you have, call the CRA directly to receive your exact contribution room. The CRA's website does not include contributions made this year to calculate your total contribution room.

What to do with an Over-Contribution Penalty?

If you over-contribute to your TFSA, the CRA will eventually send you an "Excess Amount Letter," but this can happen several months after you over-contribute, so it is essential to check this yourself regularly. If you receive this letter, follow these steps:

Step 1: Immediately withdraw the excess amount to avoid additional over-contribution fees. This helps show that you over-contributed by accident, and the fee will not be applied next month.

Step 2: Pay the total penalty and submit a TFSA Over Contribution form. You will only have a limited amount of time to pay the fine before incurring extra fees.

Step 3: Once you have handled these urgent issues, send the CRA a letter describing that you over-contributed by accident and request they refund this fee. The CRA will refund this amount if you can reasonably prove that you didn't know and that you were not notified regarding the over-contribution on time.

The Bottom Line

A TFSA is one of the best tools for saving and investing for your future, such as retirement, a mortgage down payment, or even just saving for a rainy day. The TFSA offers benefits such as tax-free growth on investments and tax-free withdrawals for any purpose. Be sure to avoid over-contributing by tracking your contributions and withdrawals closely.

FAQ

What type of investments can you hold in a TFSA?

There are several investment options available with a TFSA. This includes

- Cash, such as in High-Interest Savings Accounts,

- Securities such as stocks and ETFs,

- Guaranteed investment certificates (GICs)

- Mutual funds

- Bonds

- Gold, silver and some other precious metals

Unfortunately, you can't invest directly in cryptocurrency through your TFSA; however, there is a workaround. In Canada, there are multiple cryptocurrency ETFs that track the return of Bitcoin. You can hold these ETFs in your TFSA.

Investing in high-return investment options through your TFSA can provide the most benefits, as the returns earned are tax-free.

Can you have more than one TFSA?

Yes, you can have multiple TFSA accounts. The only limit is your total contribution room which is a fixed amount per individual. This means opening multiple TFSA accounts will not increase your contribution limit. Instead, having multiple accounts can expose you to the following risks:

- Risk of paying more fees: If you have multiple accounts that charge fees, you could end up paying more than only having one account.

- Risk of overcontribution:Having multiple accounts means there is more to manage. You may accidentally over-contribute and need to pay the penalty. As mentioned previously, the penalty is 1% per month on the over-contributed amount.

Are TFSA contributions deductible on your tax return?

TFSA contributions are not tax-deductible. You contribute to the account with after-tax money. However, the withdrawals are tax-free.

This is the opposite of an RRSP, which allows you to deduct contributions from your income tax. However, you must pay taxes when you withdraw the money with an RRSP.

Can you use a TFSA as an emergency fund?

Yes, although it's generally not recommended to invest money that you may need in the next 5-10 years. However, you can withdraw tax-free without penalties if you need the money. The amount you withdraw will be added to your contribution room in the next calendar year.

If you are saving for an emergency, you should ensure that your investment is not locked in, such as in the case of non-redeemable GICs, which can be redeemed only at the end of the GIC term. A home equity line of credit (HELOC) is another option for emergency cash for existing homeowners.

Can you name your spouse as a successor or beneficiary?

Yes, you may name your spouse as your TFSA successor or beneficiary.

- Successor: Your investments continue to grow and will be tax-free when withdrawn by your spouse.

- Beneficiary: At death, the adjusted cost basis of your investments is changed to the current market value. Any future increases are taxable when withdrawn. However, the surviving spouse may transfer their deceased spouse's TFSA value to theirs without affecting the unused contribution limit. This is done through Form RC240, which must be filed within 30 days after the transfer.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.