Mortgage Renewal Tips

5 Tips for Renewing Your Mortgage

What You Should Know

- At the end of a mortgage term, homeowners can either accept their lender's renewal offer, negotiate for better terms or switch to a new lender.

- Starting the mortgage renewal process early gives you time to explore your options and lock in a rate before it rises.

- Make extra payments towards your mortgage at renewal to reduce your interest costs and save money over the long term.

- It may be worth switching lenders if you can find a better deal, though it is important to consider possible fees.

Renewing Your Mortgage

A mortgage renewal is done at the end of your mortgage term when you haven't fully paid off your mortgage. Data from major financial institutions show that as of July 31, 2024, approximately 1.4% of all mortgages are renewed every month. Your mortgage contract will be renewed with possible term and interest rate changes. When your mortgage is up for renewal, you might want to consider taking advantage of any features that your mortgage lender offers, such as mortgage prepayment allowances.

You might also negotiate your mortgage renewal rate or shop around with other lenders for a better mortgage rate. However, before making any decisions, it's important to do your research and understand the renewal process. This page will take a look at the top 5 tips for renewing your mortgage.

What to Expect During a Mortgage Renewal 💡

During a mortgage renewal, you can expect your lender to send you a mortgage renewal notice at least 21 days before your current term expires. This notice will outline any changes to your mortgage terms and conditions, including the new interest rate and mortgage payment amounts.

At this point, you have three options: accept the renewal offer from your current lender, negotiate with your lender for better terms, or switch to a new lender.

Tips for a Successful Mortgage Renewal

Here are some tips to help ensure a successful mortgage renewal:

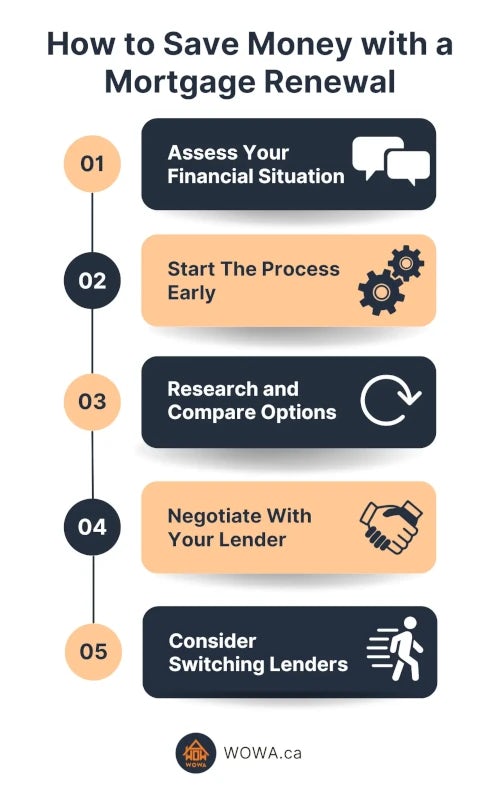

Assessing Your Current Financial Situation

Before deciding on a mortgage renewal, take the time to assess your current financial situation. Has anything changed since you first took out your mortgage? How long do you plan on staying in the home? Are you earning more income or do you have any additional debts? Are you able to increase your mortgage payments and pay off your mortgage faster, or do you need to extend your amortization to lower payments?

These considerations will determine whether you will need to renew or refinance your mortgage, and if you’ll be making any prepayments at the time of renewal.

Set financial goals for your renewal

Think about what you want to achieve during your next mortgage term and set financial goals accordingly. For example, do you want to pay off more of your mortgage? When renewing your mortgage, you’ll be able to increase your regular mortgage payments, change your mortgage payment frequency to accelerated bi-weekly or weekly payments, and make a lump-sum prepayment. These will all reduce the amount of interest that you’ll pay on your mortgage.

If you're tight on cash, you can also choose to lower your regular mortgage payments, but keep in mind that this will extend the length of your mortgage and increase the overall interest paid.

Start the process early

It's important to start the mortgage renewal process early, ideally at least four months before your current term expires. This will give you enough time to research and compare rates from different lenders, negotiate with your current lender, and gather all necessary documents for a smooth renewal process. It also gives you time to consider your options, such as whether you need to switch lenders or borrow more money by refinancing your mortgage.

Early mortgage renewals 💡

Many banks and lenders allow for early mortgage renewals ranging from three to six months before your term ends. You can take advantage of this by locking-in a rate today if you think rates will rise closer to your renewal date.

Research and compare options

Do your research and compare different mortgage options before deciding on a renewal. This includes comparing interest rates, payment frequencies, prepayment options, and penalties for breaking the mortgage early.

Online tools like mortgage payment calculators and rate comparison calculators can help you crunch the numbers and see how different factors will impact your overall mortgage costs.

Negotiate for better terms

Don't be afraid to negotiate with your current lender for better rates or terms during the renewal process. If you have a good credit score and a strong history of making mortgage payments on time, your lender may be willing to offer you a lower interest rate or better terms to keep your business.

However, also shop around with other lenders or use a mortgage broker to see if you can find a better renewal deal. This will give you leverage during negotiations and ensure that you are getting the best possible renewal offer.

Utilize prepayments to reduce your interest costs 💡

Making extra payments towards your mortgage principal can save you thousands of dollars in interest over the long term. Take advantage of your mortgage features and consider using any extra funds, such as bonuses or tax refunds, to make lump-sum prepayments during your renewal. There’s no limit to the amount you can prepay at renewal, unlike during a closed mortgage term, so take advantage of this opportunity to reduce your overall interest costs.

Consider switching lenders

If you are not satisfied with the renewal offer from your current lender, or if you have found a better deal elsewhere, don't be afraid to switch lenders. Keep in mind that there may be fees involved, such as discharge fees and legal fees, so be sure to factor these into your decision.

Avoiding Common Mistakes During Mortgage Renewal

While going through the mortgage renewal process, avoid some common mistakes that could end up costing you money or causing unnecessary stress.

Not shopping around for better rates

Don’t assume your current lender has the best offer. It's always a good idea to shop around and compare rates from different lenders before deciding on a renewal offer. Not taking the time to shop around could result in missing out on better rates and terms that could save you money in the long run.

Not checking your credit report before applying

Mortgage renewals aren't guaranteed, and your credit score plays a role in the interest rate you are offered. Before applying for a renewal, check your credit report and address any errors or issues that could affect your score, while trying to improve your credit score. This can potentially save you money by improving your chances of getting a better offer. If not, a better credit score keeps doors open when considering other lenders.

Overlooking important details

Don't just focus on the interest rate when comparing mortgage options. Be sure to carefully review all the terms and conditions of your renewal before signing any documents. Some important details to look out for include prepayment penalties, payment frequencies, and any fees associated with the mortgage.

Not considering how long you'll stay in the home

A difficult decision that borrowers face is what term to choose. If you don’t plan on staying in your home for very long, such as if you’re planning on selling or moving, then it might not be a great idea to choose a long mortgage term. If you do, and you break your mortgage early, or try to refinance it before the end of your term, then there will be a mortgage prepayment penalty that you’ll have to pay. Planning ahead when choosing a term length can help you avoid significant penalties and fees.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.