What is the Canada Pension Plan?

What You Should Know

- The Canada Pension Plan (CPP) is one of Canada’s main public retirement programs, providing monthly retirement income to eligible workers.

- The original CPP was designed to replace up to 25% of a worker’s average pensionable earnings if they start CPP at age 65.

- CPP benefits are adjusted for inflation, helping protect retirees’ purchasing power over time.

- CPP enhancement is gradually increasing the maximum replacement rate from 25% to about 33% for workers who make enough contributions under the enhanced CPP.

Recent CPP Changes

2019 to 2023: higher contribution rates under the first additional CPP component.

2024 to 2025: Starting in 2024, CPP2 introduced a second earnings ceiling for higher earners.

2026: CPP contributions apply up to a YMPE of $74,600, and CPP2 applies on earnings between $74,600 and $85,000.

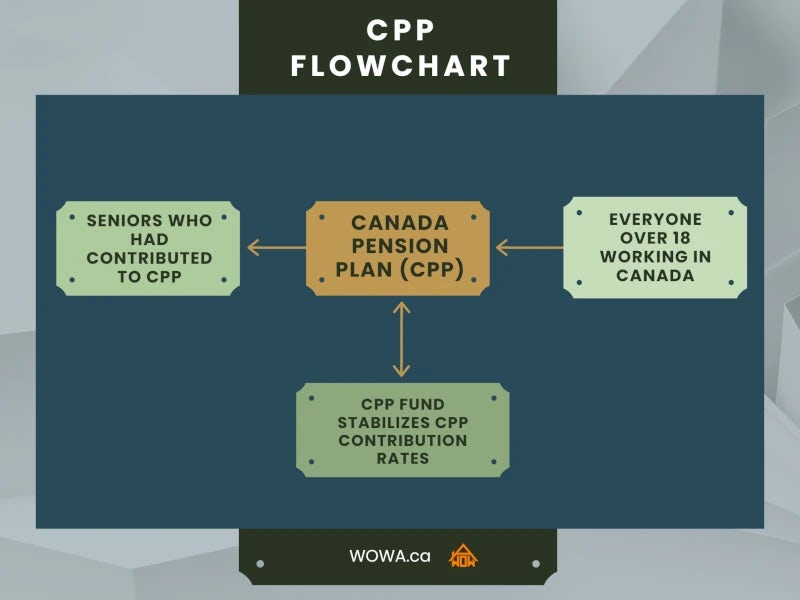

The Canada Pension Plan (CPP) is a social insurance program in Canada that provides financial assistance to eligible individuals during their retirement years. CPP is designed to provide a stable source of income to help Canadians maintain a basic standard of living after they stop working. The CPP is one of the pillars of Canada's retirement income system, along with Old Age Security (OAS) and personal savings. You can use a Canada Pension Plan (CPP) Calculator to approximate your CPP pension.

CPP was created in 1965 by Pearson’s government and belongs to all working Canadians except residents of Quebec. It is administered by Employment and Social Development Canada. The province of Quebec opted out of CPP in 1965 and created an equivalent plan called the Quebec Pension Plan. Any province may create a plan to substitute or complement CPP.

Canada’s constitution (section 94A) states that: “The Parliament of Canada may make laws in relation to old age pensions and supplementary benefits, including survivors’ and disability benefits irrespective of age, but no such law shall affect the operation of any law present or future of a provincial legislature in relation to any such matter.”

Thus, the constitution considers authority over pensions as shared between the federal and provincial governments. So, any significant change to CPP requires the approval of at least seven provinces, which contain at least two-thirds of Canada’s population.

CPP formula

CPP is based on your pensionable earnings, contribution history, and the age when you start receiving the pension. As a simplified way to think about the retirement pension at age 65:

CPP at 65 ≈ replacement rate × average adjusted pensionable earnings

The original CPP replacement rate was up to 25%. CPP enhancement gradually increases this toward one-third of covered earnings for workers with enough enhanced CPP contribution years. The final amount can also be affected by low-earning years, child-rearing provisions, disability periods, pension sharing, credit splitting, and early or late CPP start adjustments.

Key features of the Canada Pension Plan

| CPP benefit type | Average for new beneficiaries, April 2026 | Maximum monthly amount, 2026 |

|---|---|---|

| Retirement pension at age 65 | $877.01 | $1,507.65 |

| Post-retirement benefit at age 65 | $25.76 | $54.69 |

| Disability benefit | $1,234.68 | $1,741.20 |

| Survivor’s pension, under 65 | $549.62 | $803.54 |

| Survivor’s pension, 65+ | $339.36 | $904.59 |

| Death benefit | $2,606.18 average | $2,500 for pensioners, $5,000 for those who never got a pension or disability benefit |

Mandatory Participation:

With limited exceptions, workers over age 18 who work in Canada outside Quebec and earn more than $3,500 per year must contribute to CPP. Employees share CPP contributions with their employer. Self-employed workers pay both the employee and employer portions. CPP contributions generally continue until age 70, but workers aged 65 to 69 who are receiving a CPP or QPP retirement pension can elect to stop contributing.

Contributions:

Both employees and employers contribute a set percentage of the employee's earnings (up to a specified maximum) to the CPP. The contribution rates may change over time based on economic factors and government decisions. Employers are required to match the contribution of their employees to CPP. Self-employed individuals shall make contributions double the amount of employee contributions, i.e. both the employee and employer contributions.

Since 2024, CPP has included a second contribution layer called CPP2. Regular CPP contributions apply up to the Year’s Maximum Pensionable Earnings (YMPE). CPP2 applies only to pensionable earnings above the YMPE and up to the Year’s Additional Maximum Pensionable Earnings (YAMPE). In 2026, CPP2 applies on earnings between $74,600 and $85,000.

Canada Pension Plan (CPP)

Canada Pension Plan (CPP)

Canada Pension Plan (CPP)

Canada Pension Plan (CPP)

Canada Pension Plan (CPP)

Benefit Calculation:

The primary CPP benefit is the monthly retirement pension. Anyone over the age of 60 who has contributed to CPP is eligible to apply and receive the retirement pension. The amount of CPP benefits an individual can receive is based on their contributions to the plan during their working years. The CPP uses a formula to calculate the average earnings and then determines the monthly retirement benefit amount.

The monthly retirement pension is a quarter of the average pensionable earnings of the recipient in constant dollars if they start receiving a CPP pension at the age of 65. The sooner you start receiving your pension, the smaller your monthly benefit will be; the later you begin receiving your pension, the larger your monthly benefit will be.

Retirement Benefits:

CPP retirement benefits can start as early as age 60 or be delayed until age 70. The longer you wait to receive benefits, the higher your monthly payment will be. The standard age to begin receiving CPP retirement benefits is 65. Your benefit is reduced by 0.6% each month if you take your benefit earlier than the age of 65. Your benefit is increased by 0.7% each month you postpone receiving your benefit after the age of 65.

Changes in CPP benefits based on the age one starts receiving benefits

When you want to receive your retirement benefit, you need to apply well in advance. You can apply online through your MyServiceCanada account or fill out the Application for a Canada Pension Plan Retirement Pension and mail it to the nearest Service Canada Office. One can expect processing a complete application submitted online to take one month. In contrast, complete applications submitted by mail or at Service Canada locations can take four months to be processed.

| 2026 CPP Pension Payment Dates |

|---|

| January 28, 2026 |

| February 25, 2026 |

| March 27, 2026 |

| April 28, 2026 |

| May 27, 2026 |

| June 26, 2026 |

| July 29, 2026 |

| August 27, 2026 |

| September 25, 2026 |

| October 28, 2026 |

| November 26, 2026 |

| December 22, 2026 |

Survivor and Disability Benefits:

CPP also provides benefits in cases of death or disability. Survivor benefits may be paid to the surviving spouse or common-law partner of a deceased CPP contributor, while disability benefits may be available to contributors who have a severe and prolonged disability that prevents them from working regularly.

The CPP survivor’s pension depends on the deceased contributor’s CPP record, the survivor’s age, and whether the survivor already receives other CPP benefits. If the survivor is 65 or older and does not receive other CPP benefits, they may receive up to 60% of the deceased contributor’s retirement pension. If the survivor is under 65, the benefit generally includes a flat-rate portion plus 37.5% of the deceased contributor’s retirement pension.

CPP may also provide a one-time death benefit and monthly benefits for dependent children of a deceased or disabled contributor.

Contributory Period:

You must have made contributions over a certain period (at least one contribution). This period is often referred to as the "contributory period." The longer the contributory period, the greater your retirement benefit.

Portability:

CPP benefits are portable. Your CPP contributions remain attached to your record even if you move to another province, territory, or country. Once you qualify for CPP, you can apply for and receive your pension regardless of where you live.

Quebec operates its own public pension plan, the Quebec Pension Plan (QPP), instead of CPP. If you worked only in Quebec, you generally contributed to QPP and will receive QPP benefits. If you worked both in Quebec and elsewhere in Canada, your CPP and QPP contributions are coordinated so that your contribution history under both plans is recognized. In most cases, you apply through Retraite Québec if you live in Quebec when applying, and through Service Canada if you live elsewhere in Canada. If you live outside Canada, the application process generally depends on your last province of residence in Canada.

CPP and QPP are similar contributory public pension programs, but they are administered separately and may have different contribution rates, benefit rules, and application procedures.

Taxation:

CPP benefits are considered taxable income, meaning that individuals receiving them may need to pay income tax on them.

CPP Enhancement

The CPP enhancement includes a first additional component, phased in between 2019 and 2023, and a second additional component (CPP2), phased in over 2024 and 2025. Together, the enhancement gradually raises the retirement pension from replacing about 25% of eligible earnings to about 33% of the worker's average pensionable earnings in constant dollars (earnings are adjusted because inflation erodes the purchasing power of the dollar over time). The higher replacement rate builds up over many years, so the full effect applies to workers who contribute at the enhanced rates over most of their careers. Once you start receiving your pension, your monthly payment is adjusted each year in line with the Consumer Price Index (CPI) for All Items.

Post Retirement Benefit

If you continue to work and contribute to CPP after you start receiving your pension, you become eligible for an increase in your monthly allowance called “Post Retirement Benefit (PRB).” Each year of contribution, after you begin receiving a CPP pension, would automatically increase your monthly benefit from the following year. You can choose to stop contributing to CPP anytime at or after the age of 65. You cannot contribute to CPP when you reach 70.

Canada Pension Plan Investment Board (CPPIB)

The Canada Pension Plan Investment Board, operating as CPP Investments, manages CPP funds that are not currently needed to pay benefits. CPP Investments was created by the Canada Pension Plan Investment Board Act and operates at arm’s length from federal and provincial governments.

CPP Investments’ mandate is to invest CPP assets with a view to achieving a maximum rate of return without undue risk of loss. It was established in 1997 as part of reforms designed to strengthen the long-term sustainability of the CPP. The fund is invested globally across public equities, private equities, real estate, infrastructure, credit, and other asset classes.

As of March 31, 2026, CPP Investments reported net assets of $793.3 billion, up from $714.4 billion one year earlier. The organization does not set CPP contribution rates or benefit amounts; its role is to invest CPP assets to help support the long-term funding of the plan.

CPP Supplements:

Old Age Security

Old Age Security (OAS) is a federal pension program for eligible seniors aged 65 and older. Unlike the Canada Pension Plan (CPP), OAS is not based on your employment history or CPP contributions. Instead, eligibility depends mainly on your age, legal status, years of residence in Canada after age 18, and income.

To qualify for OAS while living in Canada, you must generally be at least 65, be a Canadian citizen or legal resident, and have lived in Canada for at least 10 years after age 18. If you live outside Canada, the residence requirement is generally 20 years after age 18. OAS can also be deferred until age 70, which increases the monthly payment.

OAS is a taxable monthly benefit that is reviewed quarterly for inflation. For July to September 2026, the maximum monthly OAS pension is $751.97 for seniors aged 65 to 74 and $827.17 for seniors aged 75 and older.

Higher-income seniors may have to repay part or all of their OAS through the OAS recovery tax, commonly called the OAS clawback. For the July 2026 to June 2027 recovery-tax period, the clawback begins when 2025 net world income exceeds $93,454.

Low-income OAS recipients may also qualify for the Guaranteed Income Supplement (GIS), a non-taxable monthly benefit. For July to September 2026, a single, widowed, or divorced senior can receive up to $1,123.17 per month in GIS if their annual income is below $22,800.

Many seniors are automatically enrolled in OAS. If Service Canada does not send you an automatic enrollment letter around age 64, you may need to apply through Service Canada.

| Feature | CPP | OAS | GIS |

|---|---|---|---|

| Based on work contributions? | Yes | No | No |

| Main eligibility age | 60–70, standard 65 | 65+ | 65+ |

| Taxable? | Yes | Yes | No |

| Income-tested? | No, but taxable | Recovery tax for higher income | Yes |

| Available in Quebec? | CPP outside Quebec; QPP in Quebec | Yes | Yes |

| Indexed to inflation? | Yes | Yes | Yes |

Registered Retirement Savings Account

A Registered Retirement Savings Account (RRSP) in Canada is a government-regulated, tax-advantaged savings vehicle designed to help individuals save for retirement. It allows Canadians to contribute a portion of their income into the account, where the investments can grow on a tax-deferred basis until withdrawal, typically during retirement. Key points about Registered Retirement Savings Accounts (RRSPs) in Canada include:

Tax Advantages:

Contributions to an RRSP are tax-deductible, meaning the amount you contribute can be subtracted from your annual taxable income. This can result in immediate tax savings, as your reported income for tax purposes is reduced.

Tax-Deferred Growth:

Investments held within an RRSP can grow tax-free until they are withdrawn. This allows your savings to accumulate more over time than investments in a regular taxable account, where you would be subject to annual taxes on gains.

Contribution Limits:

There is a maximum yearly contribution limit for RRSPs, equal to 18% of your previous year's earned income, up to an annual dollar ceiling set by the CRA. For 2026, that ceiling is $33,810. Your available room is the lower of the two, plus any unused room carried forward from prior years. Contributions that exceed your limit by more than the $2,000 lifetime buffer may be subject to a penalty tax.

Investment Options:

RRSPs offer a range of investment options, including stocks, bonds, mutual funds, exchange-traded funds (ETFs), and more. This allows you to create a diversified investment portfolio tailored to your risk tolerance and financial goals.

Withdrawals and Taxation:

Withdrawals from an RRSP are considered taxable income in the year when they are withdrawn. This is because you received a tax deduction when you made the contributions. However, RRSPs are primarily designed for retirement savings. Hence, there are penalties for withdrawing funds before retirement age, except for specific circumstances such as the Home Buyers' Plan (HBP) or the Lifelong Learning Plan (LLP).

Spousal RRSP:

A spousal RRSP allows one spouse to contribute to an RRSP in the other spouse's name. This can be advantageous for income splitting in retirement, potentially reducing overall tax liabilities.

Conversion to Registered Retirement Income Fund (RRIF):

By the end of the year, when you turn 71, you must convert your RRSP into a Registered Retirement Income Fund (RRIF) or use the funds to purchase an annuity. This transition allows you to start withdrawing retirement income while still enjoying some tax deferral.

Tax-Free Savings Account

A Tax-Free Savings Account (TFSA) in Canada is a government-regulated financial account that allows individuals to save and invest money without paying taxes on investment earnings or withdrawals. It's designed to provide Canadians with a flexible and tax-efficient way to grow their savings for various financial goals.

Key points about Tax-Free Savings Accounts (TFSAs) in Canada include:

Tax-Free Growth:

Any investment income earned within a TFSA, such as interest, stock dividends, and capital gains, is not subject to taxation. This means you can grow your savings without worrying about annual taxes on your gains.

Contribution Room:

Each year, the Canadian government sets a TFSA contribution limit. Any unused contribution room can be carried forward to future years, allowing you to catch up on contributions if you haven't maximized your TFSA in previous years.

Flexibility:

TFSAs can hold various investments, including savings accounts, guaranteed investment certificates, stocks, bonds, mutual funds, ETFs, and more. This flexibility enables you to tailor your TFSA portfolio to your investment preferences and risk tolerance.

Withdrawals:

You can withdraw money from your TFSA anytime without incurring taxes or penalties. The amount you withdraw is also added back to your contribution room the following year, allowing you to recontribute it if desired.

No Age Limit:

Unlike some other tax shelters, TFSAs do not have age restrictions. You can continue to contribute to your TFSA beyond age 71, which is the age at which you are required to convert other retirement accounts like RRSPs into income-generating vehicles.

Not Tax-Deductible:

Unlike Registered Retirement Savings Accounts (RRSPs), contributions to a TFSA are not tax-deductible. However, the major benefit lies in tax-free growth and tax-free withdrawals.

Accumulated Room:

TFSA contribution room accumulates yearly, even if you do not contribute. This means that if you have not contributed to a TFSA since its inception in 2009, you could potentially have significant unused contribution room.

Real Estate Investments

Real estate investing can provide retirement income through rent, property appreciation, or indirect exposure to real estate assets. Investors may buy residential rental properties, commercial properties, or shares of real estate investment trusts (REITs), which allow investors to gain exposure to income-producing real estate without directly owning a property.

More active strategies include property renovation and resale, short-term rentals, student housing, land development, and real estate syndication. These can offer higher potential returns, but they also involve higher risk, financing costs, taxes, regulation, and active management. For most retirees, real estate should be viewed as a supplement to CPP and other retirement income, not a replacement for a stable pension.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.