Toronto Vacant Home Tax Calculator 2026

What You Should Know

- If a home is vacant for six months or more in a particular year, the Vacant Home Tax for the property is payable in the following year.

- The current tax rate is set at 3% of the property's Current Value Assessment (CVA) by MPAC.

- All homeowners in Toronto are required to declare the occupancy status of their property annually.

- The declaration for 2025 must be submitted by April 30, 2026.

What Is the Toronto Vacant Home Tax?

The City of Toronto has implemented a Vacant Home Tax (VHT) starting in 2022. The VHT took effect in 2023 and required owners of homes that were vacant for six months or more in 2022 to pay this tax. The tax rate was initially set at 1% of the assessed value, which was increased to 3% in 2024. The key details of the VHT are as follows:

- Each year, the City of Toronto will issue a notice to all homeowners, asking them to declare the occupancy status of their property.

- To be deemed vacant, the home should have been vacant for six months or more in a calendar year.

- All property owners must declare the occupancy status of their property by the deadline.

- If they fail to do so, their property may be deemed vacant, and they may have to pay the VHT even if the property was occupied throughout the year.

- The tax is payable in addition to the annual property tax that homeowners pay.

The VHT was introduced by the city to increase the supply of housing within the city by discouraging homeowners from leaving their properties vacant. As of October 2025, the home vacancy rate in the City of Toronto was 3% as per CMHC’s rental market report. The City of Toronto allocated the revenue collected from the VHT towards affordable housing initiatives.

Who Should Pay the Vacant Home Tax?

The Toronto VHT is payable by homeowners whose property was declared, deemed, or determined to be vacant for six months or longer within a year. The tax does not apply to a property if:

- The property was the homeowner’s principal residence during the year

- The property was the principal residence of a tenant or a permitted occupant during the year

- The property qualifies for an exemption

Homeowners must complete the occupancy declaration by the deadline, irrespective of the occupancy status of their property. Failure to complete the declaration in time may result in fines.

Toronto Vacant Home Tax Rate

As of 2025, the Toronto Vacant Home Tax rate is 3%, and the tax is calculated based on the Current Value Assessment (CVA) of the property. For example, the CVA of a property is $1,000,000, and the property remained vacant for more than six months in 2025. Then, the Vacant Home Tax payable in 2026 is -

3% x $1,000,000 = $30,000

The following table shows the tax rate for every year starting from 2022:

| Reference Year | Vacant Home Tax Rate |

|---|---|

| 2022 | 1% |

| 2023 | 1% |

| 2024 | 3% |

| 2025 | 3% |

The CVA is determined by the Municipal Property Assessment Corporation (MPAC). This is the assessed value of your property and is mentioned on your property tax notice as well.

Occupancy Status Declaration

All homeowners must declare the occupancy status of their home by the deadline, regardless of the actual occupancy status. The declaration should be made by the homeowners themselves or by someone authorized to act on their behalf.

How to Declare?

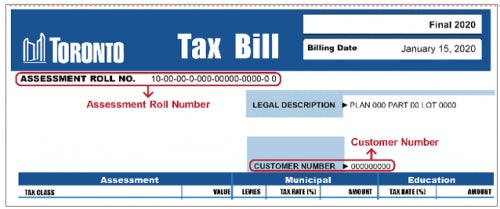

Online: The declaration can be completed online through the City’s declaration portal using your 21-digit assessment roll number and customer number, both of which can be found on the declaration notice, your property tax bill and your property tax account statement.

Paper Declaration: Homeowners can complete and submit a paper declaration form. The paper declaration can be mailed to the City Revenue Services or submitted in person at City Hall or at one of the Inquiry and Payment Counters. The addresses or links to addresses can be found on the form itself.

Consequences of Failing to Declare

If a homeowner fails to declare the status of their property by the deadline, the property may be deemed vacant, and the homeowner will be billed a VHT for the year. Additionally, failing to make a declaration in time or making a false declaration can result in fines of up to $10,000.

Paying the Vacant Home Tax in Toronto

As of 2026, the Vacant Home Tax for the previous year is payable in three equal installments, due on September 15, October 15 and November 16, 2026. The payments can be made in the following ways:

- Financial Institutions: You can pay the tax directly from your bank account using online banking, telephone banking, at an ATM, or in person at a branch. To pay using online banking, you will need the 21-digit assessment roll number on the Vacant Home Tax Notice. You can then log in to your online banking portal, select the relevant payee and make the payment.

- Mail-In Payment: You can send in post-dated cheques payable to the ‘Treasurer, City of Toronto’ at the following address:Treasurer, City of Toronto

Box 5000

Toronto, ON M2N 5V1 - Inquiry & Payment Counters and Drop Box: You can pay in person by cash, cheque, money order, or debit card at one of the Inquiry and Payment Counters located across the city. Alternatively, you can use the drop box to pay by cheque or money order.

Toronto Vacant Home Tax Exemptions

Homes that were vacant for more than six months in a year may be exempt from the VHT if the property was vacant due to the following reasons:

- Death of the registered property owner.

- The property owner was in a care facility, such as a hospital.

- The property owner had a principal residence outside the GTA but was required to occupy the property for a total of at least six months for employment purposes.

- A court order prohibited the occupancy of the property.

- Renovation or repairs to the property.

- Transfer of the property’s legal ownership.

- Newly constructed unit exemption for up to two consecutive years.

Change of Ownership Rules for the Vacant Home Tax

When a property is sold, responsibility for the Vacant Home Tax (VHT) depends on when the closing occurs. Both parties must ensure the occupancy status declaration is handled properly, as the VHT forms a lien on the property and any unpaid tax becomes the purchaser’s responsibility.

Who Must Declare?

- If the closing occurs before the declaration deadline

The vendor must submit the occupancy status declaration for the prior year and provide:

- A copy of the filed declaration

- A statutory declaration confirming its accuracy

- If the closing occurs after the declaration deadline

The purchaser must submit the declaration the following year. The purchaser will typically qualify for an exemption under “transfer of legal ownership.”

Key Notes

- Purchasers and/or vendors must make arrangements to ensure the declaration is filed on time.

- Failure to declare may result in the property being deemed vacant.

- Any unpaid VHT remains attached to the property and transfers to the new owner.

Disputing a Vacant Home Tax Assessment

Owners of homes deemed vacant will receive a Vacant Home Tax Notice of Assessment. If you receive such a notice and disagree with the assessment, you can file a Notice of Complaint. This initiates the City’s formal review of your property’s vacancy status.

You may file a complaint if:

- You missed the declaration deadline, and your home wasn’t vacant in the year in question,

- You made an error in the declaration,

- You want to dispute the VHT levied, or

- Your property was deemed vacant through an audit or otherwise, and you wish to challenge the assessment.

Important Notes

- Complaints must be filed within 90 days of the date on the Notice of Assessment.

- Supporting documentation may be required (e.g., tenancy proof, utility statements, permits).

- Filing a complaint does not pause interest on any unpaid Vacant Home Tax.

- If the complaint is denied, owners may request a further review, subject to City appeal procedures.

Final Thoughts on the Vacant Home Tax

Toronto’s Vacant Home Tax is designed to encourage property occupancy and improve the supply of housing. With the tax rate rising to 3% of a home’s CVA beginning in the 2024 tax year, homeowners should ensure they submit their occupancy declaration by the annual deadline and understand whether their property qualifies as vacant or exempt. Staying compliant and aware of timelines helps avoid unnecessary penalties, interest, or incorrect vacancy assessments.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.