Best Options for Sending Money in Canada

What You Should Know

- Online money transfer options include Intrabank transfer, electronic funds transfer (EFT), Interac transfer, wire transfer and digital wallets.

- EFT includes Direct deposit, bank-to-bank (interbank) transfer and bill payment.

- Intrabank transfer of money is easier, faster and cheaper than transferring money between different banks.

- Many non-bank players compete to transfer your money; among them, PayPal is the most popular.

Money Transfer Options

Transaction Type | Transfer Time | Transfer Limits | Cost | Required Recipient’s Information |

|---|---|---|---|---|

| Intra Bank Transfer | Immediate | Your account limit | An account transaction | Name, Account number, branch number |

| Interac e-Transfer | Up to 30 min | Often $3,000 per transfer | 0-$1.50 | Email address or cellphone number |

| Direct Deposit | 2-5 business days | NA | An account transaction | Name, Account number, financial institution number, branch number |

| Bank to Bank Transfer | 2-5 business days | Your account limit | An account transaction | Log on credentials for your online banking or Account number, institution number and branch number |

| Bill Payment | 2-5 business days | Your account limit | An account transaction | Credit card issuer and number, or line of credit provider and number |

| Wire Transfer | Varies by destination | Not limited | $15 - $50 | See wire transfer section |

| PayPal | Under 30 Min | $10,000 per 24 hours | Sending money from PayPal balance or bank account is free | Either email address or cellphone number |

Most of us frequently need to send money to another person. We might want to support a family member or a friend, or we might want to pay for a good or service (rent, price of something bought on Facebook Market or Kijiji, etc.) to one of our peers. This page provides you with information about various payment options available in Canada. The Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) and the Canada Revenue Agency (CRA) often monitor transactions exceeding $10,000.

This page only considers electronic means of transferring money. But you always have the old way of transferring money. You can still write and hand over or post a personal cheque. Most financial institutions allow customers to cash cheques via their bank's mobile app. This means that you do not have to send your cheque with snail mail; you can send it instantly using fax or email.

Intrabank Transfer

Intrabank transfers are fast and cheap, but they are limited to transfers between people using the same bank.

Assume Alice wants to send $1,000 to Bob. This process will be straightforward if Alice and Bob have Bank C accounts. All that needs to be done is for bank C to reduce Alice’s account balance by $1,000 and increase Bob’s account balance by $1,000.

In internet banking and mobile banking, there is generally a tab for bill payment. Here you can search the name of your payee (a financial institution offering lines of credit or credit cards, a utility company or any other business registered for bill payment service). After finding your payee, you would enter your account number and save your payee.

To send money to someone using the same bank as you, you can define them as a personal payee. In some banks like RBC, you can define personal payees through internet banking, while in other banks like TD, you would need to call your bank to set up a personal payee. It would require knowing the person's name, account number and branch transit number. After your personal payee is defined, you can pay the same way you would pay your credit card or line of credit with another bank.

Interac e-Transfer

When transferring a small sum of money, Interac e-Transfer is fast, cheap and convenient.

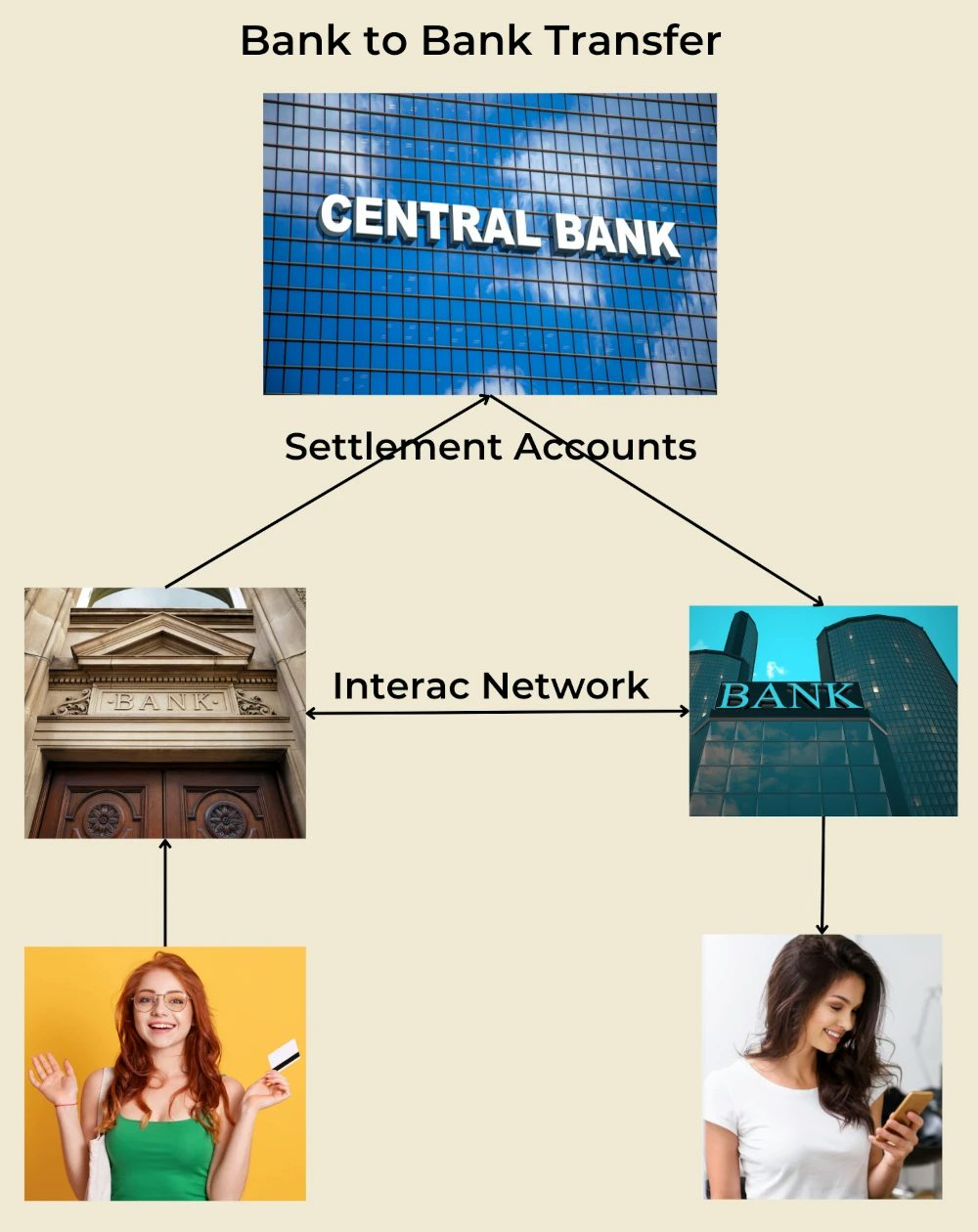

In the last section, we saw how money transfers could be done among customers of a single bank. The situation is slightly more complicated for money transfers between customers of different banks. Here, bank C should reduce the balance of Alice’s account while bank D should increase the balance of Bob’s account. For this process to work out, two additional components are needed. 1- A network where banks C and D coordinate their action, and 2- A mechanism for transferring money between banks.

Interac Association was launched in 1984 as a cooperative venture between five financial institutions, RBC, TD, CIBC, Scotiabank and Desjardins, to provide the first component, namely the needed network. At that time, the aim of launching Interac was to enable debit payments. Each financial institution keeps a settlement account with the Bank of Canada to provide the second component, namely a means for settling any net transfer between various financial institutions.

Interac Association later changed to Interac Corporation. Currently, in addition to e-Transfers, Interac Corporation manages Interac Direct Payment (IDP) and Shared Cash Dispensing (SCD). IDP is Canada’s debit card service, and SCD allows us to use an Automated Banking Machine (ABM), which does not belong to our bank.

To make an e-Transfer, the sender and recipient both would need 1- an account with a participating bank or credit union, and 2- an active email address or mobile phone number. When you log into your internet banking or mobile banking app, it should be easy to find the Interac e-Transfer tab. Under that tab, it should be easy to find your recipient's email address or mobile phone number if they are already entered. When you enter a recipient's mobile number or email address, your bank will remember that information for future transfers. You would choose the recipient and enter the amount of money you want to transfer.

The next step, which is to guarantee the security of your transfer, would depend on whether the phone number or email address you are using to transfer funds is registered in the Interac database or not. If it is registered on the database, you will see the name of the recipient of funds as recorded with their bank on your screen. If this is the person you want to transfer money to, just approve it, and the funds will be transferred to their account in less than 30 minutes. They will be notified of the transfer by email or text message. And you will receive a receipt for the money sent.

If the phone number or email address you are using to transfer funds is not registered in the Interac database, you will need to type a security question and its answer; you would either select a question which can be answered by your recipient but not by a potential eavesdropper or more likely you would need to communicate your answer to the recipient via a secure channel.

A recipient who has not set up auto-deposit will receive an email or text message with instructions for depositing the money into their bank account. Treat e-Transfer as you would treat a cash transaction, as the transfer cannot be reversed after being accepted by the recipient.

Caution

Setting up an auto-deposit is strongly recommended because taking money with an auto-deposit is safer. When receiving an unexpected e-Transfer, check it with the sender. When receiving a suspicious e-Transfer communication, avoid clicking on any link and forward it to phishing@interac.ca.

Receiving money would entail signing into your internet or mobile banking and answering the security question. More than 250 Canadian financial institutions are participating in the e-Transfer program; thus, it is improbable that your financial institution is not participating. Banks used to charge for doing e-Transfers, but competition has forced them to drop this fee for most of their accounts.

Currently, among major banks, only TD and CIBC charge respectively $1 and $1.50 for doing an e-Transfer from their cheapest chequing accounts. e-Transfer from most chequing accounts is free, but it often counts as one of your transactions if you have a limited number of free transactions in your plan. Doing e-Transfer from a non-chequing account (e.g., savings account or line of credit) often involves a charge. Note that cancelling a transfer before being accepted and reclaiming a transfer which is not accepted might entail paying a fee.

Interac e-Transfer limits

| Bank | Per transaction | Per 24 hours | Per 7 days | Per 30 days |

|---|---|---|---|---|

| TD | $3,000 | $3,000 | $10,000 | $20,000 |

| BMO | $3,000 | $3,000 | $10,000 | $20,000 |

| CIBC | $3,000 | $3,000 | $10,000 | $30,000 |

| HSBC | $7,000 | $7,000 | $10,000 | $40,000 |

| Tangerine | $3,000 | $3,000 | $10,000 | $20,000 |

| Simplii Financial | $3,000 | $3,000 | $10,000 | $30,000 |

| National Bank | $5,000 | $5,000 | $25,000 | NA |

| Scotiabank | Limits can differ for different customers. Each customer can see their transfer limit through their online banking portal. | |||

| RBC | Limits can differ for different customers. Each customer can see their transfer limit through their online banking portal. | |||

Interac e-Transfer is a prominent payment system subject to oversight by the Bank of Canada. The amount of money you can transfer is limited by the withdrawal limit on your card or account. In addition, many banks limit the amount of money sent via Interac e-Transfer.

You can also use the Interac network to request money. The person you are requesting money from will receive an email or text message with instructions for making an e-Transfer to you.

RBC accounts are typically limited to $5,000 ($25,000 for customers with a security token) worth of daily transactions. This limit can be temporarily increased three times a year via internet banking.

Direct Deposit

Direct deposits are fast, cheap and convenient for government and businesses to make payments and for people to receive payments.

Direct deposit is a form of electronic funds transfer (EFT) used by institutions and businesses to make their payments. They are, in effect, electronic cheques which, instead of coming to your address, directly go to your bank account. Tax returns, benefit payments and salaries are often paid by direct deposit.

Interbank Transfer (Bank to Bank Transfer)

Interbank transfer is ideal for transferring money between the accounts of a person in different financial institutions. This includes sending money to your high-interest savings account and your stock broker.

Before making a bank-to-bank transfer, the accounts need to be linked to one another. You must enter your other bank’s account information to link accounts. Then your financial institution needs to verify the connected account. To confirm that the linked account is indeed related to you, they would make two very small deposits into the account you are trying to link. In a few days, the accounts are linked by entering the amounts of those deposits in your online banking portal.

Some banks might complete/verify the linking process by asking for your online account credentials in the other bank to speed up the process. After linking, you can either push money to or pull money from your linked account. Often there is a limitation on how much money can leave your account in an internet bank to bank transfer. Larger transfers can be made by calling your bank.

Wire Transfer

Wire transfer is the go-to way to transfer large sums of money relatively fast.

Wire transfer is the best option for transferring large amounts of time-critical funds to any destination. Wire transfers are quick, safe and reliable. Lynx is Canada’s high-value payment system which is used for sending Canadian dollar wire transfers as well as the Canadian leg of international wire transfers. Unlike checks, Lynx transfers have real-time settlement finality. Payments Canada provides Lynx. Wire transfers between customers of the same financial institution are known as “on us.” They are dealt with internally and do not go through the Lynx. Completeness, accuracy and formatting of the information provided enable straight-through processing (STP). You will likely face processing delays and added fees if manual intervention becomes necessary. For a wire transfer, you should provide:

- Name and address of sender

- FI name, branch address and five-digit transit number for the financial institution from which the funds will be sent

- Account number from which the funds will be sent

- Name on the beneficiary's account

- Address of the beneficiary

- Bank account number along with the transit number for the branch where the funds are to be deposited.

- Beneficiary's financial institution name and branch address, including postal code and SWIFT Business Identifier Code (BIC) if available.

- Amount

- Date

- Details of charges

A wire transfer between two Canadian banks can be done in a few hours. TD allows you to receive a wire transfer for $17.50 and to send a wire transfer to another TD account number for $16. But sending a wire transfer to an account in another bank would set you back $50. Using TD Global Transfer (electronic banking) TD performs a wire transfer for $25 or less. CIBC allows you to receive a wire transfer for a $15 fee but to send a wire transfer you need to pay $30 (for sending $10,000 or less), $50 (for sending more than $10,000 but less than or equal to $50,000) or $80 (for sending more than $50,000).

With RBC, you can receive a wire transfer either from other RBC customers or for less than $50 free of charge, while you need to pay $17 to receive a wire transfer from a non-RBC account. Each outgoing wire transfer would cost RBC customers at least $45 (depending on the destination). Scotiabank charges $15 for receiving a wire transfer (unless it is a pension payment). BMO charges you $14 for receiving a wire transfer while it sets you back $50 for outgoing wire transfers. HSBC customers receive wire transfers for a fee of $17. They can send a wire transfer to a different currency account with a value of less than $10,000 for free. Wire transfer fees for sending money to an account with the same currency and transfers to different currency accounts with values greater than $10,000 can cost from $35 to $90. Depending on the value transferred and whether it is done online or in the branch.

Wire Transfer Cost

| Bank | Incoming/Outgoing | Limitation | Cost or Fee |

|---|---|---|---|

TD | Incoming | Any | $17.50 |

| Outgoing | To TD | $16 | |

| To non-TD | $50 | ||

CIBC | Incoming | Any | $15 |

| Outgoing | <= $10,000 | $30 | |

| $10,000 & <= $50,000 | $50 | ||

| > $50,000 | $80 | ||

RBC | Incoming | From RBC | Free |

| From non-RBC | $17 | ||

| Outgoing | Any | $45 | |

BMO | Incoming | $14 | |

| Outgoing | $50 | ||

Scotiabank | Incoming | $15 | |

| Outgoing | -- |

Bill Payment

You can make a bill payment to the credit card or line of credit of the person you want to send funds to. If their account has no balance, they can transfer this money to their chequing account (with the same bank), likely without charge. In doing so, the recipient needs to be wary of incurring a cash advance charge.

PayPal

PayPal can be considered the oldest and most successful digital wallet which facilitates payment and money transfer.

PayPal is the most successful and widespread digital wallet. It has a peer-to-peer payment platform called “PayPal.Me”. PayPal is one of the most trusted brands in the world. It is licenced as a Humburg-based bank in the European Union. It is free to make a PayPal account by going to paypal.ca or the PayPal app and clicking/tapping signup. You start by providing your email and creating a strong password, and follow on with typing some personal information.

You can link your bank account, credit card, and debit card to your account. You would enter the institution, transit, and account numbers to connect your bank account. A few days later, you would need to confirm your account by providing the value of the two small deposits made by PayPal to your account. PayPal can send money to other persons or pay for many goods and services offered by online vendors. When using PayPal to send money to other persons, you can use their PayPal.me link or their email address to transfer money to their PayPal account.

Certain smaller online vendors may be unable to process credit card payments, and you may be hesitant to share your credit or debit card information with unfamiliar or untrusted online vendors. PayPal offers a convenient solution for receiving payments in online transactions for small vendors. It also provides a secure method for making payments without the need to disclose any sensitive financial information.

In addition to facilitating the transaction, PayPal offers a limited warranty on your transactions through PayPal. The way it works is that if you pay for an online purchase through PayPal and either you do not receive your purchase, or you receive something materially different from its online description, and the seller refuses to resolve the dispute, you can use PayPal's dispute resolution mechanism to receive a partial or total refund.

Suppose you are sending money to a commercial account. In that case, the receiver has to give a slice of their cash (2.9% of the transacted amount + $0.30 per transaction for domestic exchanges) to PayPal to facilitate the transaction. But if you send money to a personal account, PayPal is willing to facilitate the transaction for free if the money is coming from your PayPal account or your bank account. But if you use a card to fund the transaction, PayPal has to pay for this transaction, and it will charge you 2.9% of the transacted amount + $0.30 per transaction for domestic exchanges.

Any change of currency entails a 4% exchange fee, and sending money from Canada to the US or Europe would have an added $3 charge. Sending money to regions other than the US and Europe would entail an added $5 fee. There is no fee for receiving a personal payment through PayPal. To withdraw your money from PayPal, you can be patient and pay no cost for a standard EFT to your bank account. For transferring money instantly to your debit card, you would incur a 1% charge. You would have a daily and weekly withdrawal limit of $5,000 and a monthly withdrawal limit of $10,000.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.