CMLS Financial Mortgage Rates & Reviews

CMLS Background

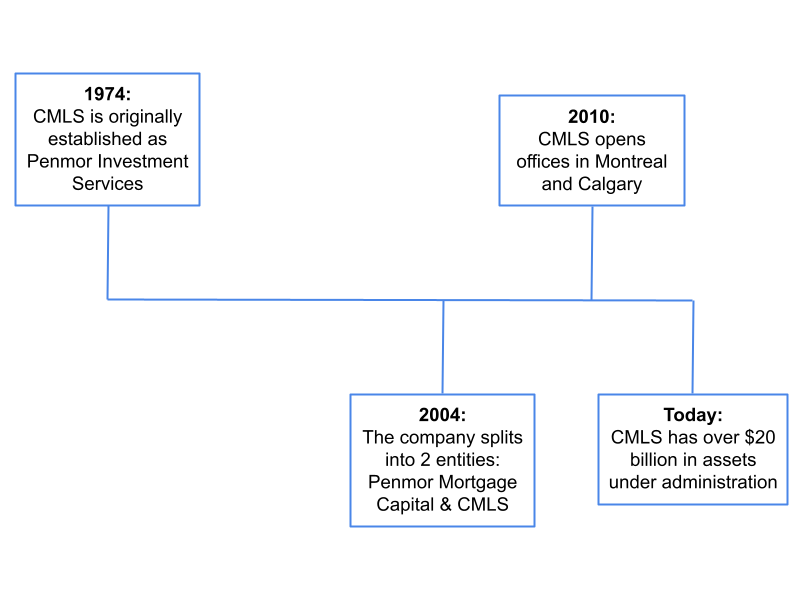

CMLS is a privately owned mortgage services company founded in 1974 and is headquartered in Vancouver, British Columbia. The firm specializes in all mortgage-related activities, such as residential mortgages, advisory services, institutional services, capital market activities, and asset management. The company has a portfolio exceeding $20 billion in assets under administration, with mortgage originations being over $5 billion per year.

Rocket Mortgage

As of May 31, 2025, Rocket Mortgage has officially ended its operations in Canada. To ensure a smooth transition, CMLS Financial is now supporting all existing Rocket Mortgage clients.

If you're a Rocket Mortgage customer seeking assistance, please contact CMLS Financial at:

- Phone: 1-888-995-2657

- Email: service@cmls.ca

CMLS Financial Fixed Mortgage Rates

Getting a fixed rate CMLS Financial mortgage will give you the benefit of keeping the same CMLS mortgage rate for your entire term. This gives many homebuyers the peace of mind they need to feel comfortable taking out a mortgage, especially for first time home buyers. The only time that you will be affected by a change in mortgage rates with a fixed rate mortgage is when you go to renew your mortgage. Because of this, longer terms such as the 5 year fixed mortgage and the 3 year fixed mortgage are very popular with homebuyers.

| Term | CMLS Rate | Canada's Lowest Rate |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

CMLS Financial Variable Mortgage Rates

A variable rate mortgage from CMLS Financial will allow you to benefit if CMLS mortgage rates fall, however will cost you more in interest payments if they rise. No matter what happens with your mortgage rate, you will still have the same monthly mortgage payment, with the only difference being in the breakdown of the payment. If the prime rate and mortgage rates rise, you will owe more towards interest payments and will be paying less to the principal balance, while if interest rates fall, more will go towards the principal and less to interest.

| Term | CMLS Rate | Canada's Lowest Rate |

|---|

The rates shown are for insured mortgages with a down payment of less than 20%. You may get a different rate if you have a low credit score or a conventional mortgage. Rates may change at any time.

CMLS Financial Prime Rate

CMLS Financial's prime rate is used as the basis when calculating a variable mortgage rate, which is determined by combining the prime rate with a spread. This spread can be positive or negative, and in most cases is negative. This is because variable rate mortgages are fairly low risk for the lender, with the mortgage having the home as collateral.

Current CMLS Financial Prime Rate: 4.45%

CMLS Financial History

CMLS Mortgage Break Penalty

If you decide to break your current mortgage early, you will owe a prepayment penalty. This penalty will likely be thousands of dollars, depending on your mortgage term length, mortgage amount, and interest rate.

| Bank or Lender | Variable Rate Mortgage | Fixed Rate Mortgage |

|---|---|---|

| Lesser of 3 Months’ Interest or, the remaining interest to be paid on your mortgage. | Greater of the IRD amount, and, the lesser of 3 Months’ Interest, or, the remaining interest to be paid on your mortgage. |

The IRD is used to calculate a fixed rate mortgage prepayment penalty for almost all lenders in Canada. The way it is calculated is by finding the difference between the posted rate for the time left on your term, and your current mortgage rate. This difference then is multiplied by how long is remaining on your term to get your interest rate differential prepayment penalty.

To see how much you can expect to pay in prepayment charges, utilize the Desjardins mortgage penalty calculator below:

Are you looking to pay off your mortgage early? Or refinance the terms of your mortgage at a lower interest rate? Maybe you sold your home. Whatever the case, you most likely will have to pay a mortgage break penalty set by your lender. Whatever the situation, our calculator will help you determine the cost to break your mortgage so you can be confident about your mortgage decisions.

What is the remaining balance on your mortgage?

What is your current regular mortgage payment amount?

What is the term-length and type of your current mortgage?

What is your current mortgage interest rate?

If applicable, what was the rate discount you received when you signed your current mortgage agreement?

When did your current mortgage start?

Is the Property:

Who is your current mortgage lender?

What is CMLS Financial's current interest rate for a 1-year fixed rate mortgage?

What would you like to do?

Please complete all fields before calculating.

By using the calculator, you agree to our Terms of Service

CMLS Mortgage Features

Home System Warranty Program

This add-on coverage will cover damages that occur to your home and that need repair, covering your AC & heating, electrical system, water heater, and plumbing. The only cost you will incur will be the $50 consultation fee, and you will be covered for up to $10,000 in repair bills. CMLS will provide you with complimentary coverage for your first 12 months, meaning you will not need to worry about costly repair bills as you get into your home.

Skip-A-Payment

Every calendar year, you will be able to skip one regular mortgage payment. This is only allowed if you have prepaid at least the same amount as the amount you are skipping a payment on. This can be a good option to help you get breathing room in the event of an unexpected event, such as a family emergency, job loss, or unexpected expense.

Prepayment Privileges

There are 2 ways that you can prepay your mortgage early, which includes:

- Increase your regular payments: At any time, you can increase your mortgage payment by up to 20% at any time. This can help you to pay off your mortgage early, saving you thousands of dollars in interest, especially if you have the money leftover in your budget.

- Annual 20% prepayment allowance: Every calendar year, you will be able to prepay up to 20% of your original mortgage balance without incurring a penalty. This can be prepaid at any time during the year, and you can make multiple payments.

CMLS Combination HELOC

Did you know that you can get an insured mortgage, at a low mortgage rate that's given to insured mortgages, along with a HELOC? The CMLS Combination HELOC combines an insured or insurable first mortgage with a home equity line of credit (HELOC). The mortgage can be for up to 50% of the value of the home, while the maximum loan-to-value (LTV) of both the mortgage and HELOC is 80%.

While the loan limit is combined, the Combination HELOC is made as two separate mortgage applications: one for the first mortgage, and one for the HELOC. This means that you can have an insured mortgage while still borrowing money with a HELOC. The minimum amount you can borrow with the HELOC is $10,000 at an interest rate of Prime + 0.5%. Just like other HELOCs, the minimum payment is interest-only.

Since it's an insured or insurable mortgage, it has to meet certain CMHC rules. For example, the maximum property value allowed is $1 million. You'll need a minimum credit score of 600, and the maximum amortization period is 25 years.

The CMLS Combination HELOC is only available for new purchases or transfers/switches in Ontario, British Columbia, Quebec, Alberta, and Saskatchewan.

Getting a CMLS Mortgage

You are able to get a mortgage from CMLS Financial directly through a mortgage broker. CMLS works with mortgage brokers across the country, meaning that you will have plenty of options to get a CMLS Financial mortgage. As well, with your current mortgage with CMLS, you are able to access all your information online, through the CMLS mortgage portal.

CMLS Office Locations

| City | Location |

|---|---|

| Vancouver | Coal Harbour: 1066 West Hastings Street #2110 |

| Toronto | South Core: 18 York Street |

| Calgary | Downtown Calgary: 333 7 Avenue SW #2130 |

| Montreal | Downtown Montreal: René-Lévesque Boulevard West |

| Ottawa | Old Ottawa East: 1101 Elgin St, Ottawa, ON |

| Halifax | Waterfront: 2000 Barrington St #1307 |

| London | Westmount: 785 Wonderland Rd S #225 |

| Winnipeg | South Portage: 202 Garry Street |

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.