What is a FICO Credit Score?

WOWA® Simply Know Your Options

What You Should Know

- FICO Score is a credit score calculated using FICO’s proprietary scoring models.

- There are different FICO scoring models developed by FICO over the years, the popular ones being FICO 2, FICO 4, FICO 5, and FICO 8.

- FICO Score can help determine the creditworthiness of a person.

- FICO Scores in Canada generally range from 300-900.

FICO (NYSE:FICO), formerly known as Fair Isaac Corporation, is a U.S.-based data analytics company known for creating credit scoring models that are used to determine the credit scores of individuals. FICO Scores are the most widely used scores by lenders in credit risk evaluation. Having a good FICO score will help you get a loan on favourable terms and give you access to the best mortgage rates offered by lenders. According to FICO, 90% of Canadian lenders use its score as one of the measures of a person’s creditworthiness.

What Is a FICO Score?

A FICO Score is a three-digit number derived using FICO’s scoring system that is used to determine a person’s credit risk and creditworthiness. These credit scores are used by lenders to make lending decisions like if and how much credit can be extended to a person and at what interest rate. The score is calculated on the basis of information on your credit reports of the two credit reporting agencies or bureaus — Equifax and TransUnion, including particulars about your credit accounts, credit inquiries, public record, and collections. FICO itself isn’t a credit bureau, and it doesn’t collect your credit data or store your personal information. You should monitor your credit report regularly and ensure that the information on it is accurate. If you find any errors, you must immediately contact the credit reporting agency or the institution that reported the wrong information to them.

FICO has developed several scoring models since its inception, with the latest being FICO Score 10 Suite. Different models are often used to determine creditworthiness for different industries; for example, the scoring model used to determine creditworthiness for revolving credit is usually different from the one used to determine creditworthiness for a mortgage.

Unlike in the U.S., consumers in Canada do not have direct access to their FICO Scores. The bureaus provide FICO Scores to lenders on your credit reports. However, FICO has introduced the FICO Scores Open Access Program in Canada, which aims to provide consumers with access to their FICO Scores through their lenders. The adoption of the program is dependent on the lenders, though.

Credit Scores From Different Providers

The two credit bureaus – Equifax and Transunion, also have their own credit scores. Consumers can request their own credit report from one of the bureaus. Equifax offers this service for free, while TransUnion lets you order a credit report for $25 or get a monthly subscription for $25 per month. The report displays the bureau’s credit score, which is different from FICO scores. You may notice that your TransUnion credit score is different from your Equifax credit score, which is because of the different scoring models.

Websites such as Borrowell and Credit Karma and online banking websites of major banks like RBC and Scotiabank give you access to your credit scores for free. However, these credit scores are also taken from TransUnion or Equifax, which are not your FICO Scores. The bureaus provide FICO Scores only to lenders and not to consumers.

FICO Score Range

FICO Scores in Canada generally range from 300 to 900. According to FICO, the scores can be broken down into five ranges. A score of 579 or less is considered low, and lenders usually consider borrowers with this score as risky. A score in the range of 580 - 699 is considered fair, and a few lenders may be willing to extend credit to borrowers with this score. A score in the range of 670 - 739 is near average and is considered a good score by most lenders. A score of 740 - 799 represents a very good credit score, and borrowers with a score in this range are generally considered low risk. Those with a credit score of over 800 are considered very low risk by lenders, and such borrowers usually get credit at the most favourable terms.

| Poor | Fair | Good | Very Good | Exceptional |

|---|---|---|---|---|

| 579 and below | 580 to 669 | 670 to 739 | 740 to 799 | 800 and above |

It is also noteworthy that all lenders have their own criteria for extending credit. While one mortgage lender may offer its best interest rate to individuals with a credit score of over 720, another may offer the best rates only to those with a credit score of over 750. Lenders also take into account other information while reviewing credit applications, such as delinquencies recorded on your credit report and your income.

FICO Score Calculation

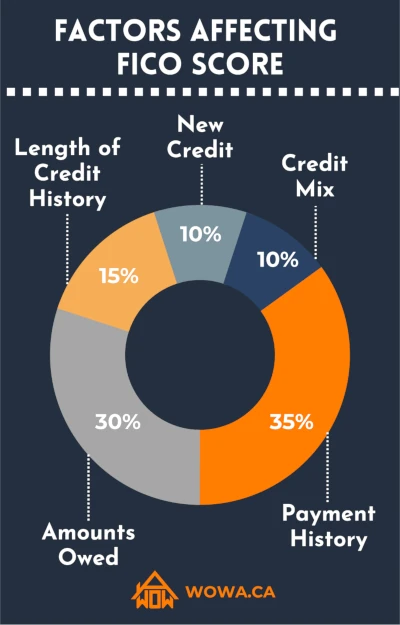

FICO Scores are calculated using the information on your credit report. This information is divided into five categories, each of which has a different weightage in the determination of credit score. For example, the payment history has a general weightage of 35%, which means that 35% of your credit score is determined by your payment history. FICO weighs the categories differently for different individuals; however, a general weightage of the categories is listed below.

- Payment History (35%)

This category includes your payment information related to your credit cards, loans, retail accounts, and finance company accounts. It also includes information regarding delinquencies (late or missed payments), public records, and collection items. The on-time payments are also taken into account. It is recommended that you always make payments on time, as late payments can have detrimental effects on your credit score.

- Amounts Owed (30%)

This category includes information about the amount owed on all your credit accounts. Information such as the number of accounts that have a balance and credit utilization on revolving credit accounts are also taken into account. The balance on installment loans compared to the original loan amount is also considered.

Credit Utilization Ratio

Credit utilization ratio refers to the ratio of the credit you use to the total credit available to you. For example, if your credit card has a credit limit of $10,000, and you use $2,000, your credit utilization ratio will be 20%. It is recommended that you keep the credit utilization of your revolving credit accounts, like credit cards and lines of credit, under 30%.

- Length of Credit History (15%)

In general, having a long credit history has a positive impact on your credit score. FICO Score takes into consideration the age of your oldest credit account and the average age of all accounts. The length of some specific accounts also matters.

- New Credit (10%)

Making multiple credit applications in a short time frame makes you look risky and has a negative impact on FICO Scores. Newly opened credit accounts, credit inquiries made by lenders and time since a new account was opened have an impact on your FICO Score.

It is recommended that you space out your credit applications, as each inquiry will reduce your credit score by a few points. One exception is shopping around for a mortgage or auto loan. If you intend to get just one loan but are just shopping around for a better rate, any inquiries of the same type made within 30 days are counted as one. This does not apply to credit inquiries for credit card applications.

Hard Vs Soft Credit Inquiries

Hard and soft credit checks occur under different circumstances and have different impacts on your credit score. Every time you make a credit application, you authorize the lenders to pull your credit report. This inquiry is noted on your credit file and is visible to anyone who pulls your credit report after that. This is known as a hard inquiry, and it lowers your credit score by a few points.

On the other hand, when you pull your own credit report to monitor it, the inquiry does not hurt your credit score and is called a soft inquiry.

- Credit Mix (10%)

Credit mix refers to the variety of credit accounts that appear on your credit report. Generally, individuals with a good mix of credit accounts such as credit cards, installment loans, mortgages, and retail accounts in good standing tend to have higher credit scores than those with only one or two credit accounts.

While you may not have access to your FICO score directly, you can maintain a healthy FICO Score by doing the following.

- Always make credit payments on time.

- Keep credit utilization on revolving credit accounts under 30%.

- Keep a gap of three to six months between credit applications.

- When shopping around for a mortgage or auto loan, get quotes from lenders within a two-week span.

- Check your credit reports for inaccuracies regularly and dispute any inaccuracies as soon as you spot one.

- Avoid closing credit accounts, as this will decrease the length of your credit history.

If your credit score is low, you can follow the measures listed above to improve your credit score. Additionally, you can check out credit builder programs offered by some Canadian companies, such as Borrowell and KOHO, or get a secured credit card that can help you build credit.

FAQs

FICO is a U.S.-based data analytics company known for creating widely used credit scoring models. FICO Scores are used by many lenders and creditors in Canada and several other countries to assess credit risk and make lending decisions.

What is a good FICO Score?According to FICO’s general guide, a good FICO Score is of 670 or above. However, some lenders may consider even a lower score to be good, while some other lenders may require your score to be higher to be considered good. In general, a score above 740 is considered very good, and over 800 is considered exceptional.

How do I get my FICO score Canada?You can check your credit scores for free from websites like Borrowell and Credit Karma. However, these scores are different from FICO Scores. Borrowell gets your credit score from Equifax, while Credit Karma gets it from TransUnion. The credit bureaus have their own proprietary credit scoring models to generate this score. The bureaus also provide FICO Scores to lenders on your credit report; however, consumers don’t have access to this score. FICO has introduced the FICO Score Open Access Program in Canada, which allows lenders to provide FICO Scores to their customers for free. The Canadian lending companies goPeer and Parachute are said to be the early adopters of this program.

How often is FICO Score updated?FICO Score is updated approximately once a month. However, based on the number of credit accounts you have, your FICO score may update more frequently.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.