How to Buy a Property in the U.S. as a Canadian

This Page's Content Was Last Updated: March 5, 2024

It's no surprise that more and more Canadians are looking to buy or invest in property in the United States. With its diverse landscapes, bustling cities, and endless opportunities, the U.S. is an attractive destination for Canadians to live, work, and play. However, navigating the process of buying property in a foreign country can be daunting. That's why we've put together this guide to help Canadian buyers understand the ins and outs of purchasing property in the U.S.

- Canadians can finance the purchase of U.S. property through a cross-border mortgage using their Canadian credit history with a minimum down payment of 20%.

- You’ll need to provide the same documents as you would when applying for a Canadian mortgage, such as proof of employment and income.

- U.S. homes are commonly bought by Canadians as vacation homes, residences, or rental properties.

- You can close your U.S. mortgage from Canada with a mail-away closing or even virtually with some lenders in certain states.

1. Research the U.S. Real Estate Market

Do you know where you want to buy a home in the U.S.? Research different states and cities to find the best location for your needs. Consider factors such as cost of living, weather, and amenities. If you’re moving to the U.S. for work, check to see commute times and modes of transportation available.

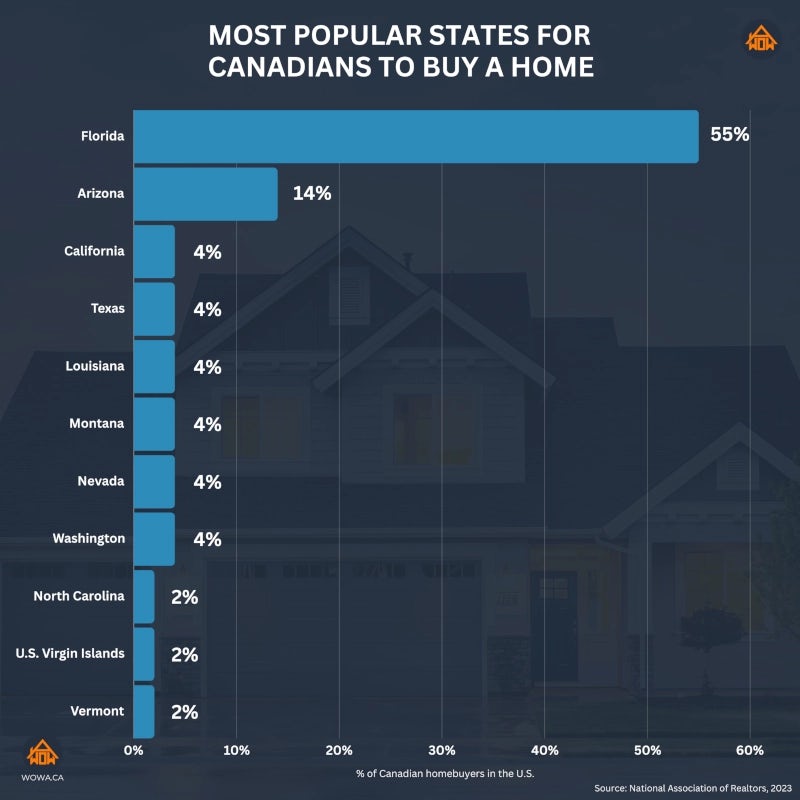

The most popular states for Canadians to purchase property in the U.S. include Florida, Arizona, California, and Texas. Many Canadians buy a home in Florida and other states that feature warm weather, perfect for Canadian snowbirds, with plenty of activities, attractions, and possibly lower cost of living compared to major Canadian cities. There’s a lot to learn about being a snowbird, so make sure that temporarily living abroad is right for you.

In 2023, Florida was the most popular state for Canadians to buy a home in, with 55% of Canadian homebuyers in the U.S. settling in the state. According to the National Association of Realtors, the second most popular was buying a home in Arizona, followed by California, Texas, Louisiana, Montana, Nevada, and Washington.

2. Get Pre-Approved for Financing

If you plan on financing your U.S. property purchase, it's important to get pre-approved for a mortgage from either a Canadian lender that offers cross-border home financing, or with a U.S. lender. Many real estate agents in the U.S. will require a pre-approval letter before showing you properties. This will also give you a better idea of your budget and what properties you can afford.

RBC Bank offers U.S. pre-approvals using your Canadian credit history that are valid for up to 120 days. Applying only takes a few minutes, and you can get a pre-approval within 1 to 2 business days.

Your lender may also help connect you with professionals to assist with the legal and tax aspects of buying property in the U.S. For example, RBC U.S. HomePlus Advantage connects you to cross-border mortgage advisors, tax and legal experts on issues such as immigration and taxes, home insurance providers, as well as U.S. real estate agents.

3. Work with a U.S. Real Estate Agent

It's important to work with a real estate agent based in the U.S. who has experience with cross-border transactions. They can guide you through the differences between the Canadian and U.S. real estate markets and help you find the best property for your needs.

When searching for the perfect property, there are several considerations to keep in mind. First and foremost, consider the location. Look into the safety of the neighborhood, proximity to amenities such as shops, public transportation, and other facilities. Second, think about the property's potential for future appreciation. Research the area's growth trends and future development plans.

Third, consider the property's condition. A professional home inspection can shed light on potential issues such as structural defects or needed repairs. If you’re planning to retire and looking to use the property as a snowbird, consider accessibility and the potential for future modifications. You may want to consider an active adult community or a property with features that accommodate aging in place.

Lastly, consider your budget and affordability. Ensure that the cost of the property, along with potential property taxes and maintenance costs, is affordable. Renting out the property when not in use can help offset costs.

Once you have found a suitable property, work with your real estate agent to make an offer and negotiate the purchase terms. They can provide valuable insight into market trends and help you make a competitive offer.

When buying a home in the U.S., Canadians are more likely to pay for the purchase in cash rather than getting a mortgage. According to the National Association of Realtors, 69% of Canadians made an all-cash purchase in 2022. That number decreased in 2023, when 51% of Canadians made an all-cash purchase.

Financing a U.S. home purchase with a mortgage isn’t quite as common for Canadians, but it’s still an option, and it can come with benefits. For example, if you plan on renting out the property, you may be able to deduct mortgage interest and other expenses from your rental income for tax purposes. Making a down payment of just 20% for your residence or 25% for investment properties can also free up your cash and reduce the amount of money that you need to convert to U.S. Dollars.

4. Apply for a U.S. Mortgage

Even if you've already been pre-approved for a mortgage, you will still need to apply for a U.S. mortgage after finalizing the purchase of the property. This will secure the financing needed and ensure that all necessary paperwork is in order. It can take 40 to 45 days to close on a U.S. mortgage, so be sure to plan accordingly to avoid any delays or complications.

When working with a Canadian lender that offers cross-border U.S. home financing, be prepared to provide financial documents, such as bank statements, tax returns, and proof of income. Your lender may also ask for a deposit to cover the cost of a home appraisal.

With RBC Bank’s U.S. mortgage options, you can complete your mortgage application and submit documents online. You won’t need to visit a branch to sign documents. To apply, you will need to provide the following:

- Passport/Work Visa

- Canadian Social Insurance Card/U.S. Social Security Card

- Confirmation of income, such as pay stubs and the most recent two years of T4s, or T1s and T2s for self-employed borrowers, or pension statements and T1 General for retirees

- Purchase agreement/contract

- Mortgage/line of credit statements, if you have any existing mortgages in Canada or abroad

- Insurance, property tax, and HOA/condo fee statements, if you own any properties in Canada or abroad

- Statements for the most recent two years for bank accounts, RSP accounts, and investment/brokerage or line of credit accounts if those funds will be used to close the new home

- Homeowner’s insurance policy

While RBC Bank processes your U.S. mortgage application, they will give you a conditional approval letter that is valid for 60 days. RBC Bank will have a home appraisal conducted to determine the value of the property and ensure it meets its lending criteria. You will also have to pay for title insurance.

5. Close on Your U.S. Mortgage

Once you have been approved for a U.S. mortgage, the final step is to close on your mortgage. This involves signing all necessary documents and paying closing costs and fees. In the U.S., closing costs usually start from 2.5% of the home’s purchase price. You’ll need to make a down payment of at least 20%, or 25%, if it will be an investment property.

Before the closing date, be sure to carefully review all of the loan documents provided by your lender. It's important to understand the terms of your mortgage, including mortgage interest rates and repayment terms.

For those who want to close on their mortgage from Canada, there are a few ways that you can close on your mortgage without traveling to the U.S. The first is with a mail-away closing, where documents are sent to you for you to sign before a notary public and then returned by mail. The second is with a power of attorney, where a designated representative, such as a family member in the U.S., can sign the documents on your behalf. Finally, some states, such as Florida, allow for completely virtual closings with a Remote Online Notary (RON).

Once all documents are signed and payments have been made, your mortgage will be funded, and the property will officially be yours. Congratulations, you are now a homeowner in the U.S.! It's important to note that closing procedures may vary depending on the state and specific lender, so be sure to consult with your real estate agent or lender for exact instructions.

Remember to keep all documents related to your U.S. mortgage in a safe place for future reference. You will also need to report any income generated from the property on your taxes in both Canada and the U.S., so it's important to stay organized and keep track of all necessary paperwork.

Did you know that you can buy a home in the U.S. without having to visit the property physically or even leave the country? It is now possible to complete the entire U.S. home-buying process from Canada. This means you can search for properties, attend virtual showings, and even sign contracts all from the comfort of your own home.

Some lenders, such as RBC Bank, let you apply for a U.S. mortgage and sign documents online. For closing, you can do a mail-away closing where you sign and send the documents back from Canada. This can be a great option for those who are unable to travel to the U.S. or prefer to complete the process remotely.

You can finance the purchase of single-family homes, townhomes, condos, and multi-unit rental properties with a cross-border mortgage. Usually, lenders will not let you finance the purchase of timeshares, houseboats, mobile homes, and co-ops.

Yes, it is possible to get a U.S. mortgage without having an established credit history in the United States. When working with a Canadian lender, they’ll look at your Canadian credit history instead.

When purchasing property in the U.S., you will need to pay land transfer tax, and on-going property tax.

When selling a U.S. property, you may be subject to capital gains tax in the U.S., and possibly in Canada as well. You may also be required to pay a Foreign Investment in Real Property Tax Act (FIRPTA) withholding tax. Depending on the home’s value, you may be subject to U.S. withholding taxes of up to 15%, which is meant to ensure that capital gains taxes are paid.

Yes, many Canadian homeowners choose to rent out their U.S. properties while they are not using them. In fact, 7% of Canadian homebuyers in the U.S. purchased a home solely as a rental property. Renting out your U.S. home while you are not using it, whether as a short-term rental or long-term rental, can provide a source of income to help offset the costs of property ownership. However, rental income may be subject to U.S. income tax.

A visa is not required for Canadians to purchase property in the U.S., but it may be required for extended stays or if you plan on working in the U.S.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.