4-Year Fixed Mortgage Rates

| Lender | Rates |

|---|---|

4-Year Fixed Mortgage in Canada: Full Guide

This Page's Content Was Last Updated: November 8th, 2022

What You Should Know

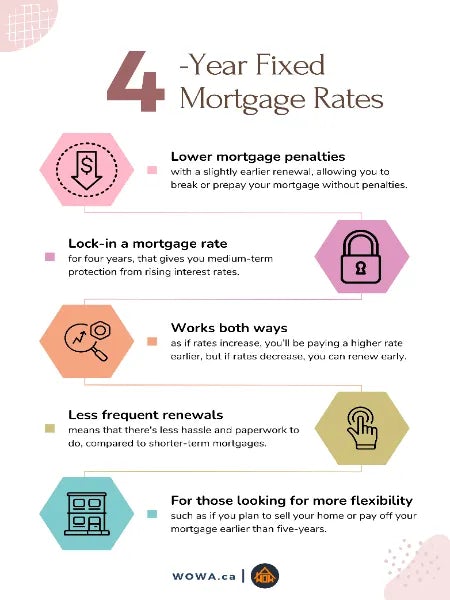

- 4-year mortgages offer medium-term protection from rising interest rates.

- While not as popular as 5-year fixed mortgages, 4-year fixed mortgages can be used by those expecting rates to rise in the near future.

- Being shorter-term when compared to a 5-year mortgage might mean you’ll be able to get a better rate, depending on where interest rates are headed.

All About 4-Year Fixed Mortgages in Canada

A 4-year fixed mortgage is a home loan with a term of four years. In Canada, aspects of your mortgage such as the mortgage payment amount and the mortgage interest rate are tied to your term. For example, with a 4-year fixed mortgage term, your interest rate, and consequently your mortgage payment amount, is fixed for four years. In other words, your mortgage rate and payment won’t change during this 4-year term.

If you are thinking of getting a 4-year fixed mortgage, there are other things to consider besides just the mortgage rate available. This page will take a look at what a 4-year mortgage means to you, the pros and cons, and how it compares to the standard 5-year mortgage term.

4-Year Fixed Mortgages in Canada: The Pros and Cons

The most common term length in Canada is five years. However, there are some reasons why you should consider a mortgage with a shorter term length. Here are the pros and cons of a 4-year fixed mortgage term.

Pros:

- Usually, you might find that shorter mortgage terms have a lower interest rate than longer mortgage terms. This can save you money.

- A slightly shorter term gives you more flexibility, as you might be able to refinance or make prepayments with lower mortgage penalties, or renew earlier.

Cons:

- If rates have risen, you’ll be forced to renew at a higher rate, rather than having a lower rate locked in for longer with a 5-year term.

- Those looking for more flexibility, such as if you plan to sell your home or to pay off your mortgage early, might be better off with a shorter-term mortgage.

Pros and Cons of a 4-Year vs. 5-Year Mortgage

| 4-Year Mortgage | 5-Year Mortgage | |

| Pros |

|

|

| Cons |

|

|

Comparing Average Mortgage Rates by Term Length (August 2022)

| Less than 1 year | 1 to less than 3 years | 3 to less than 5 years | 5 years and more | |

| Interest rate | 6.78% | 4.47% | 4.36% | 4.34% |

Source: Government of Canada

What to Consider Before Getting a 4-Year Fixed Mortgage in Canada

Here are some questions to ask yourself before making a decision:

Do you plan on staying in your home for at least four years?

Paying mortgage prepayment penalties isn’t pleasant, especially if you can avoid them. Mortgage penalties can also be a significant expense for those with a closed mortgage. If you might move in the near future, where you’ll need to pay off your current mortgage in full, then it might make more sense to get a shorter mortgage term.

Where are interest rates heading?

In a rising interest rate environment, you’ll want to lock in your mortgage rate for as long as possible. The opposite is true in a decreasing interest rate environment.

If rates are rising, a 4-year mortgage term provides enough time to generate interest cost savings while not being long enough for the locked-in rate to be priced at a premium. Longer mortgage terms have higher interest rates because mortgage lenders charge a premium for the ability to lock in an interest rate for a long period of time. However, if the rate difference is small between a 4-year mortgage and a 5-year mortgage, you may want to consider locking in for a longer term.

If rates are falling, a shorter term lets you renew into a lower rate earlier, rather than being locked into your higher rate for longer.

Do I need a fixed rate?

Choosing between a fixed vs. variable mortgage comes down to where you think rates are headed. Fixed mortgage rates offer predictability, as you’ll know exactly how much you need to pay. With a variable rate, your interest rate can change at any time, which affects how much interest you’ll need to pay. While this might not always affect your current mortgage payments, this can cause you to have to catch up on your mortgage amortization later if rates rise, often in the form of increased payments in the future. However, variable mortgage rates are often priced at a discount compared to fixed mortgage rates. You’ll also benefit if rates decrease during your term.

Disclaimer:

- Any analysis or commentary reflects the opinions of WOWA.ca analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. WOWA® does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Financial institutions and brokerages may compensate us for connecting customers to them through payments for advertisements, clicks, and leads.

- Interest rates are sourced from financial institutions' websites or provided to us directly. Real estate data is sourced from the Canadian Real Estate Association (CREA) and regional boards' websites and documents.