What is RESP?

What You Should Know

- An RESP is a savings account with the purpose of funding a child’s further education.

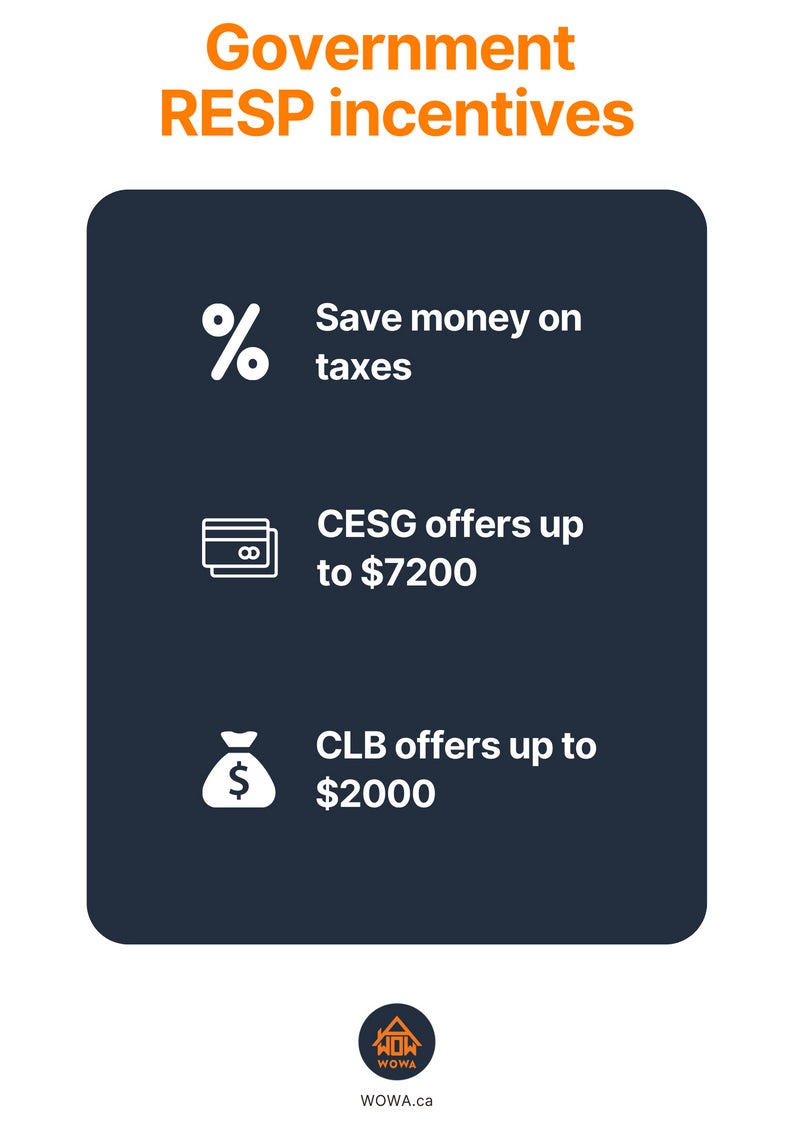

- You can recieve up to $600 a year in Canada Education Savings Grants (CESG) and $100 a year in Canada Learning Bonds (CLB) by investing in an RESP, with potential for more from provincial grants.

- You can receive a total of $7200 from CESG and $2000 from CLB.

- Your investment profits will not be taxed while within an RESP account.

- However, there will be downsides if the child does not pursue further education.

What is a Registered Education Savings Plan (RESP)?

A Registered Education Savings Plan is a tax-privileged investment account, set up to fund someone’s post-secondary education. An RESP is a type of Registered Savings Plan (RSP) that allows you to invest and earn interest tax-free while also receiving contributions from the government. When the beneficiary enrolls in a recognized post-secondary institution such as a university, college, or trade school, they can retrieve the RESP.

After the money is withdrawn, it is considered taxable income belonging to the beneficiary. However, because the beneficiary is a student and probably not earning other income, their overall income is often low enough that no tax will be paid on it.

This all makes the RESP a very powerful financial tool that can be leveraged to wisely plan for you and your child's future. To calculate approximately how much money an RESP account can save, you can visit our RESP calculator.

An RESP will involve 3 parties:

How Does the Government Support the RESP?

Saving on taxes

The first method the government uses to to encourage investment in an RESP is through various tax incentives. While the money is within the RESP, you will probably have a variety of options on how to invest it. You can allocate it into mutual funds, ETFs, GICs, stocks, bonds, or a combination of the above, and any capital gains which you make will not be taxed. This is a significant advantage over traditional trading accounts, where you must pay income taxes on half of the capital gains that you have made over that year. Additionally, when the beneficiary decides to withdraw the money from the account when they attend higher education, the money withdrawn is considered their own income. This is advantageous because of the students’ low income from other sources, which means that many students can eliminate the need to pay tax altogether, or else only have to pay a small amount.

One common misconception is that you get a tax deduction for the amount of money that you invest into an RESP. You will not recieve a tax deduction for any money invested.

Canada Education Savings Grant (CESG)

Another method the government uses to incentivize investment in RESPs is through the Canada Education Savings Grant program. This program adds up to 20% of the annual contribution into the RESP. The yearly limit that the government will provide is $500, which means that you should aim to deposit $2500 into the RESP every year to receive the full CESG amount for that year.

The government can give additional CESG depending on your family income. A family income of less than $49,020 attracts an extra 20% pay-out from the government on the first $500 contributed and a family income of between $49,020 and $98,040 attracts an extra 10% grant.

However, families of all incomes have a lifetime grant limit total of $7,200 for one child. This means lower income families can contribute less and still receive more government aid money in their RESP, but not beyond the $7200 limit. Bear in mind that the exact family income brackets are determined year-to-year depending on inflation and other adjustment factors. One restriction of the CESG is that the beneficiary must be under 18 to receive it. Thus, it is best to start investing into an RESP early to reach the maximum allowable amount of $7,200.

| Family Income | CESG on first $500 contribution | CESG on full $2500 contribution |

|---|---|---|

| Less than $49,020 | $200 | $600 |

| Between $49,020 and $98,040 | $150 | $550 |

| More than $98,040 | $100 | $500 |

Canada Learning Bond (CLB)

Canada Learning Bonds are another government incentive for investment into RESP accounts. They are specifically directed towards encouraging lower-income families to begin to invest in their RESPs. This money is deposited into the child’s RESP directly, initially only $500 for the first year followed by an additional $100 every year after for up to 15 years until the limit of $2000 is reached. The exact income threshold to qualify for CLB is dependent on the number of children within the family. For a family with one child, the family qualifies if their annual income is less than or equal to $49,020. Note that the thresholds may also change year-to-year due to inflation and other adjustment factors. Additionally, the child in question must be born during or after 2004.

A unique aspect of Canada Learning Bonds is that they are retroactive. This means that a child of any age born after 2004 can qualify for Canada Learning Bonds. If they are over 18, they themselves can apply for CLBs and receive money retroactively for however many years their family has qualified, once again up to $2000 dollars. They can apply up until age 21.

Provincial RESP grants

Aside from benefits provided by the federal government, two provincial governments also offer their own incentives for residents of those specific provinces to invest into an RESP.

| Province | Requirements | Incentives |

|---|---|---|

| British Columbia | The British Columbia Training and Education Savings Grant (BCTESG) requires that the beneficiary is born after 2006. In addition, the RESP has to be held with a partnered financial institution. | The grant provides the beneficiary with an additional $1,200. |

| Quebec | The Quebec Education Savings Incentive (QESI) requires the RESP to be held with a partnered financial institution. The child must be under 18. | The grant matches 10% of annual RESP contribution up to an annual limit of $250 and a lifetime limit of $3,600. Low income families can receive an additional $250 per year. |

Opening an RESP Account

Now that you have learned about the benefits of an RESP account, you may be wondering how you can open an RESP account.

RESP legal requirements

There are some legal requirements to opening a new RESP account. First, the beneficiary of the RESP has to be a Canadian resident. Permanent residents and Canadian citizens both qualify. Second, the beneficiary must have a social insurance number (SIN). Canadian residents can apply for a SIN on the Canadian government website if they do not have one already.

Types of RESPs

There are 3 types of RESP plans.

| Individual RESP Plan | |

| Family RESP Plan | |

| Group RESP Plan |

Contributing to an RESP Account

With the RESP account created, the next step is to allocate money into it.

RESP contribution limits

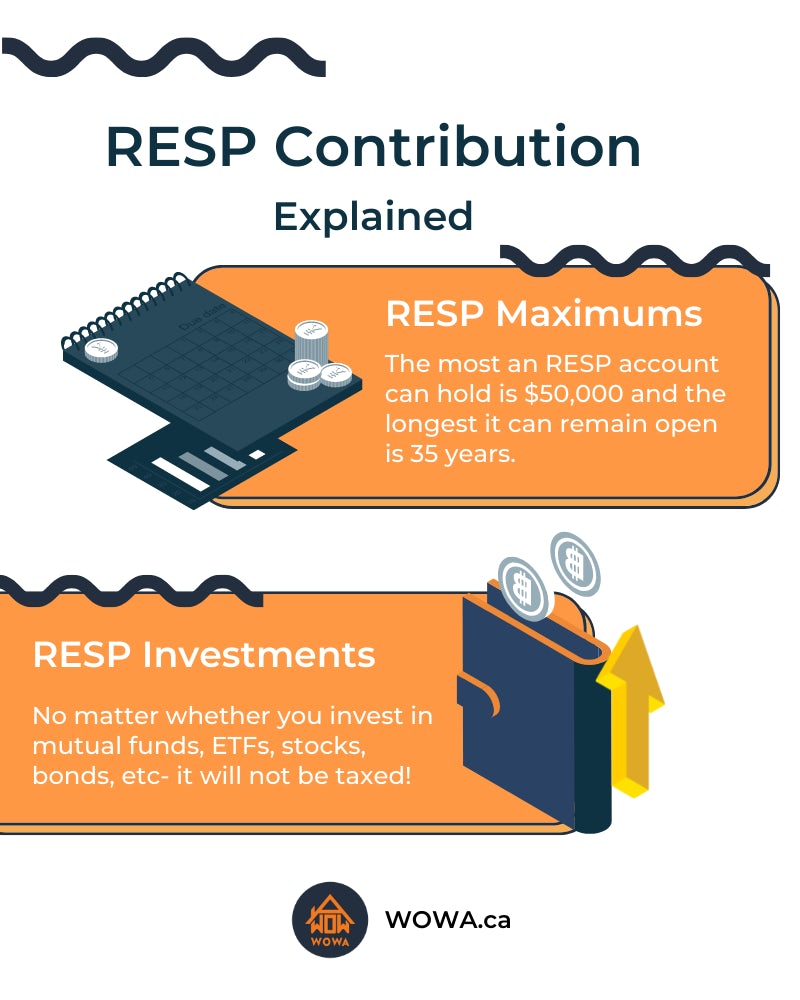

The RESP has a lifetime contribution room of $50,000 and there is no annual contribution limit into the plan. Thinking about the tax-incentives, it may make sense to invest as much money into the plan as early as possible: capital gains on money invested within the RESP is tax-privileged. However, there are downsides to contributing all $50,000 in one year. Since there is no annual contribution limit, you can pay all the $50,000 at once into the plan but doing so would mean that you’re forfeiting about $6,700 of free government money. Since each year only 20% of the first $2,500 of contributions ($500) would be paid by the government as CESG.

How long an RESP account can remain open

An RESP account can remain open for 35 years. This allows freedom for the beneficiary to attend university when they feel ready to. However, it is best to contribute to the plan when they are under 18 years of age, as then the beneficiary would qualify for different grants from the government and province. It will also be best to withdraw from the RESP when the beneficiary does not hold a job. This is to minimize potential taxation on capital gains made in the RESP account.

RESP investments

While the money is within the RESP, you will probably have a variety of options on how to invest it. You can allocate it into mutual funds, ETFs, GICs, stocks, bonds, or a combination of the above and any capital gains which you make will not be taxed. In addition, you can choose to invest the RESP individually, but many financial institutions will also invest it for you at a low cost. How you choose to invest your money will depend on your risk tolerance as well as the approximate time until withdrawal.

Multiple RESP accounts for one individual

As mentioned in the group RESP plan section, an alternative to the group RESP plan is for a single beneficiary to have multiple individual RESP plans with different subscribers. However, the lifetime contribution of $50,000 per beneficiary still holds for all of the RESPs combined. For a beneficiary with more than one RESP account, CESG grants are paid into the first RESP account where the contributions are first made. If contributions are made into two accounts on the same day, the CESG payment is divided in half and split across both plans.

Withdrawing from an RESP Account

Now it is time to reap the benefits of your foresight and confidently withdraw from your RESP account. However, there are multiple ways to withdraw, each with their own withdrawal rules that you will need to follow.

Types of withdrawals

| Educational Assistance Payment (EAP) | |

| Refund of Contributions (ROC) | |

| Accumulated Income Payment (AIP) |

The Beneficiary is not Attending Higher Education

You are taking a risk by setting up an RESP, so you should know what happens to your money if your child refuses to go to a post-secondary institution such as a college, university, or trade school. The first thing to do is not to panic as RESP accounts can remain open for 36 years. If using a family plan, the money can be transferred to another child’s plan provided their contribution hasn’t been maxed out up to the $50,000 limit. Also bear in mind that each child cannot access CESG above $7,200. Each child’s plan including contribution and grants is managed separately within the family plan.

If this isn’t possible, you can withdraw all your original contribution from the RESP tax-free and in the form of Refunds of Contributions (ROC) and return all CESG or CLB money to the government. Your capital gains, interest, or dividend payments from investments are paid out to you as Accumulated Income Payment (AIP).

Choosing an RESP Provider

An important consideration when deciding to begin investing in an RESP is which financial institution to invest with. This is an important decision because of the different fees associated with managing an RESP, which differ bank to bank. Before signing a contract with any one bank, you should take a look at what other banks are offering, as well as reviews of these different RESP accounts online to make the best decision. Below are some popular financial institutions which you can begin an RESP with. You can also find other brokerages that offer RESPs in our list of the best trading platforms in Canada.

FAQ

RESP is taxable, but it is tax-deferred. The original amount deposited by the sponsor(s) is not taxed when the money is withdrawn. However, incentives deposited by the government and investment profits of the account are taxed as regular income in the hands of the beneficiary.

The RESP is not tax deductible. Amounts deposited into the account can not be deducted from the subscriber’s income taxes.

The age limit will be different for different RESP plans. A family plan will have an age limit of 21 to be added. The other plans have no age requirements. However, certain incentives provided by the government will have different age limits. For example, the CESG has an age limit of 18, so it is best to invest early.

Yes, you can withdraw the RESP anytime. However, there will be consequences to withdrawing the money before the beneficiary attends higher education. Incentives provided to the account must be returned to the government. Additionally, there will be a higher tax rate on investment profits in the account.

The RESP and RRSP (Registered Retirement Savings Plan) are both savings accounts. However, the RESP is meant to fund a minor’s education, while an RRSP is meant to fund an individual’s retirement. They both have tax benefits and other incentives.

A TFSA (Tax-free Savings Account) is a much more general savings account. It can be used to save for a child’s future education, but it won’t receive the RESP-specific government incentives such as the CESG and CLB. One benefit of a TFSA is that there will not be consequences if your child decides not to pursue further education.