What Happens If You Miss a Mortgage Payment?

What You Should Know

- Most lenders give you a grace period of 15 days from the missed payment date to make a payment without any penalty.

- If you don’t make a payment for 30 days from the payment due date, the payment is considered missed.

- If you know you are going to miss a payment, you should talk to your lender before the payment date.

- Missing mortgage payments can hurt your credit score.

Missing a mortgage payment can have a detrimental effect on your credit score, and if you continue missing your mortgage payments, your lender may even proceed with a power of sale or foreclosure. Read below to find out the consequences of missing a mortgage payment, and what to do if you are going to miss a payment or have already missed a payment.

What Happens If You Miss a Mortgage Payment?

Most lenders in Canada give a grace period of 15 days, which means that the payment is not considered missed if you pay up within this time. After the 15-day period, the lender can take legal action against you. However, in most cases, lenders don’t take legal action until about 90 days from the date of a missed payment.

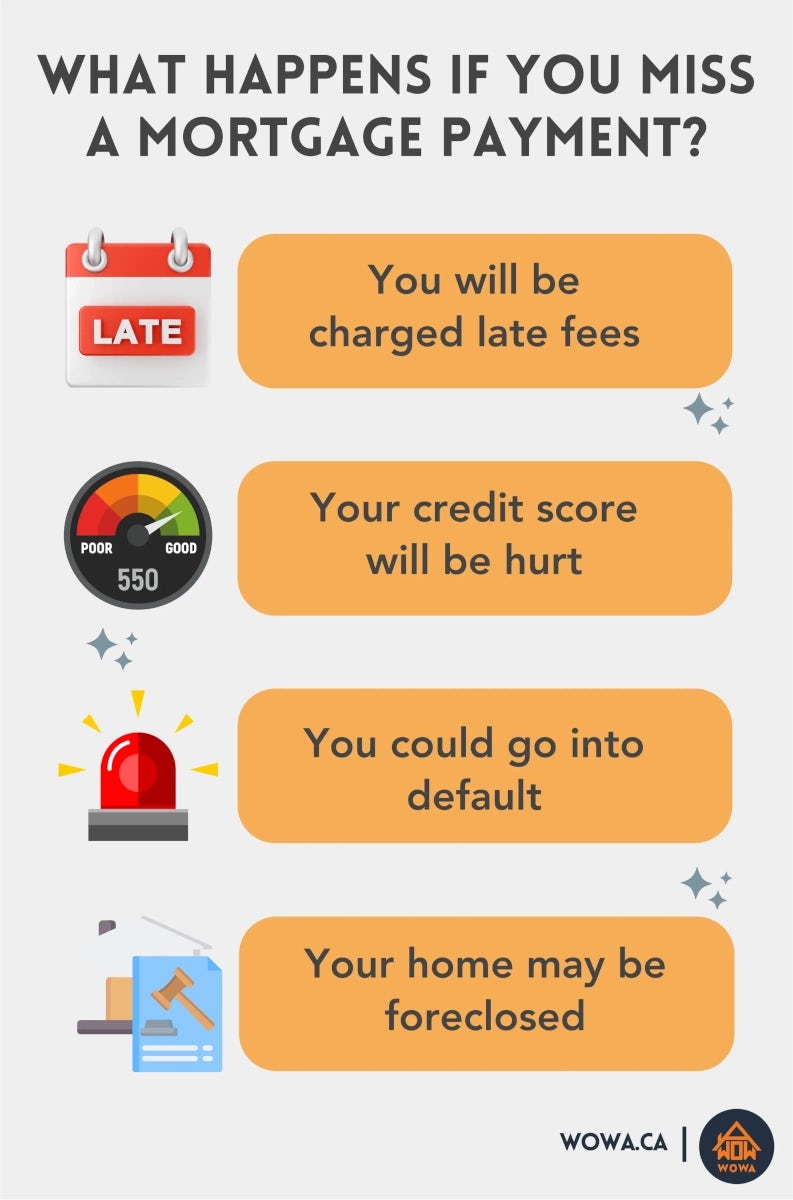

- 1. You may be charged late fees

Mortgage contracts include terms for late payments and outline the fees you would need to pay in the event of a late mortgage payment. The amount varies depending on your lender but most lenders charge a late fee of $25 to $50. Lenders usually give you a grace period of 15 days, after which the payment would be considered missed. If you make the payment within this period, the lenders typically don’t charge a late fee. - 2. You may be charged late fees

Lenders usually report missed payments to credit bureaus after 30 days of the payment due date. Missed payments have a negative effect on your credit score, and your credit score is likely to drop in such a situation. On-time payments is one of the factors considered by credit bureaus (TransUnion and Equifax) for calculating credit scores. Your credit score determines your creditworthiness, and therefore it is extremely important to make timely payments and maintain a healthy credit score. - 3. Your loan could go into default

Mortgage default occurs when the borrower breaks any term of the mortgage contract, such as when they stop making monthly payments. Your mortgage will go into default when you don’t make a payment for 30 days after the payment due date. A loan default can lead to serious damage to credit scores and might even lead to foreclosure. - 4. You might lose your house

Your mortgage is a loan secured by the home as collateral. When you fail to make the mortgage payments, your lender can legally take your home and recover the mortgage amount by selling it. Depending on the province, the lender can carry out the process of foreclosure or power of sale. The commonly used term used to describe this process is foreclosure.Power of Sale vs. Foreclosure

Power of sale means that the lender has the power to sell your property if you stop making mortgage payments. Power of sale is applicable in Ontario, Prince Edward Island, New Brunswick, and Newfoundland and Labrador. Typically the lender will give you written notice before initiating a power of sale and you have the opportunity to stop the process by bringing your mortgage back into good standing or to pay it off during the notice period. After the lender sells the home, the money left over after the mortgage and fees are paid off goes to the homeowner. At the same time, if the sale does not recover the mortgage and selling fees, the homeowner will be on the hook to pay the shortfall.

In Quebec, British Columbia, Alberta, Manitoba, Saskatchewan, Nova Scotia, and the 3 territories, the process of foreclosure is carried out instead. This is a lengthier process than the power of sale. The lender needs to go to the civil court and get a foreclosure order that transfers the title and right of the home to the lender. The lender can now sell the home and keep the profit or bear the loss of the sale.

How Late Can a Payment Be Before Being Considered Missed?

In Canada, most lenders give the borrower a grace period of 15 days before being considered as missed. If you make the payment within the grace period, you are not charged the late payment fee. If you don’t make any payment within 30 days of the payment due date, the lender will report a missed payment to credit bureaus. The missed payment will appear on your credit report and negatively impact your credit score.

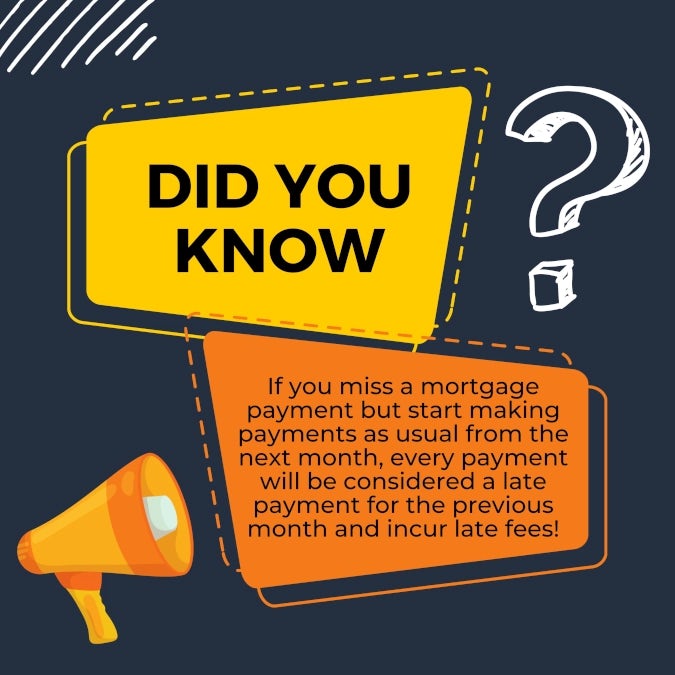

What Is a Rolling Late?

If you miss a payment and make a payment as usual in the following month, the payment will be considered a late payment for the previous month. This payment will not be considered an on-time payment, and you will be charged a late fee for this payment. Every payment you make after this will be considered a late payment for the month before, and you will be charged a late payment fee each month. This is known as rolling late. You could avoid this situation by making a double payment or talking to your lender. The lender might let you defer or skip one payment and continue your payments from the following month.

How Many Mortgage Payments Can You Miss Before Foreclosure?

Most lenders will give you an opportunity to get your payments on track before proceeding to foreclosure. Most lenders do not proceed to take any legal action for about 90 days from the date of your first missed payment. Instead, they will send you reminder letters after 30, 60, and 90 days. If you keep missing your payments, and do not respond to their letters, the lender will likely proceed with the foreclosure process after 90 or 120 days have passed.

What to Do if You Think You’re Going to Miss a Mortgage Payment?

Keeping your lender in the loop is key to reducing the consequences of a missed mortgage payment. If you think you are going to miss a mortgage payment, you should immediately talk to your mortgage lender.

Inform your mortgage lender

Most lenders will work with you and offer you a solution if you talk to them before you miss a payment. Lenders prefer to avoid foreclosures and are more likely to cooperate and compromise before you have defaulted rather than after you have missed a payment. They may even reduce or forgive your late payment penalty if you are going to pay up soon or offer you an alternate payment plan if you are experiencing financial hardship.

Consider mortgage deferral and skip-a-payment options

You must also determine if your problem is temporary or if you are likely to miss payments going forward as well. For a short-term issue, the lender may offer you a solution, such as skipping a payment or a mortgage deferral, allowing you to defer the payments for a specific amount of time.

Increase amortization, refinance or get a second mortgage

If you are experiencing financial hardships due to an issue such as loss of job, illness or injury which is likely to impact you for a long time, the lender may offer you solutions such as extending your amortization period, which would allow you to make smaller payments for a longer duration of time. Some other solutions include interest-only payments, mortgage capitalization, second mortgages, mortgage refinancing, and more.

What to Do When You’ve Already Missed a Mortgage Payment?

If you have already missed a payment, you still have options to get back on track. You could do the following when you miss a payment.

Contact your lender and discuss repayment options

If you missed your payment and have not contacted your lender yet, you should do that as soon as possible. If you don’t do that, the lender will definitely contact you. You should not avoid talking to the lender and rather work with them to find a solution. The lender will want to discuss the issue and offer you repayment options. Foreclosure is usually the last option for lenders, and most lenders will offer you multiple options before going for foreclosure.

Avoid a ‘Rolling Late’

As discussed earlier, if you miss a payment and then start paying as usual from the next month, every payment will be considered a late payment for the previous month and accrue late fees. Avoid this by informing your lender in advance as most lenders offer the option to skip-a-payment.

Talk to your lawyer

If you think you will not be able to pay your monthly payments going forward due to a sudden change in your financial situation, you should take advice from a lawyer or mortgage broker. It may be better to sell your home rather than go into foreclosure or bankruptcy, as they can severely damage your credit score. It could take you several years to rebuild your credit in such a situation.

Bottom Line

To maintain your mortgage in good standing, you must make your mortgage payments on time. However, if you are unable to make a payment and are afraid you will miss the payment, you should contact your lender at the earliest and discuss your options. Missed mortgage payments can have serious consequences, and you may also end up losing your home. Additionally, your credit score can be majorly impacted, and you could spend years rebuilding your credit.