Guide to Pre-Construction Condos in Toronto

This Page's Content Was Last Updated: November 1, 2022

WOWA Trusted and Transparent

All You Need to Know About Pre-Construction Condos

Pre-construction condos can be a great way to enter Toronto's real estate market, but the process of buying and financing them is very different from buying a typical resale home. Our guide covers how to find and buy a pre-construction condo, the different stages of a project from Friends and Family to Platinum and VIP, how you can finance a pre-construction condo, HST taxes, and much more.

What You Should Know

- It is very difficult for individual home buyers to get pre-construction condo units and usually have to use an experienced broker or brokerage firm. WOWA is partnered with Platinum Level brokers who can get you access to exclusive pre-construction projects.

- Pre-construction condo units are reserved while the building is being developed. Once construction is completed, ownership is transferred to the home buyer.

- Pre-construction condo units are distributed in 4 stages where at each state, exclusivity decreases and price increases.

- The down payment is split into separate payments spread over several months throughout construction.

- Before ownership is transferred, home buyers can move into or rent out their unit during the occupancy period.

Buying a Pre-Construction Condo

How does buying a pre-construction condo work?

You can find a pre-construction condo unit through brokers, brokerage firms, and condo developer websites. Platinum level brokers and brokerage firms can give their home buyers exclusive access to projects during the Platinum and VIP Stages before they are public. They have specialized experience in the pre-construction industry and can help you find the best condo units.

When you sign your purchase agreement, ownership of the property is not transferred immediately. Instead, you are given a unit assignment, which acts as a reservation on a specific unit when construction is completed. Once your unit is finished, which takes multiple years, you can move into your unit during the occupancy period and once this period ends, you will receive full ownership of the unit.

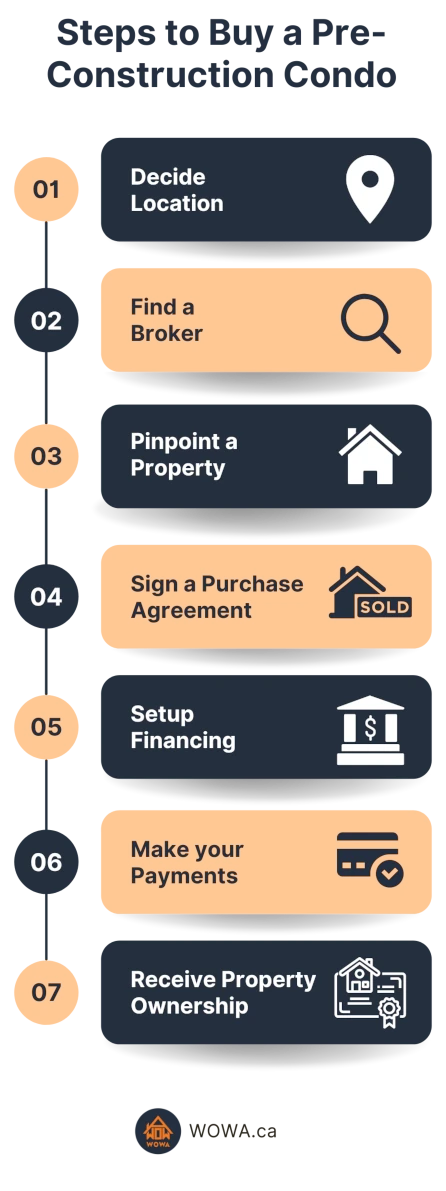

How to Buy Pre-Construction Condos

1. Location

Decide where you want to live. Location is the most important factor in any real estate decision and there are many places that you can get a condo within the GTA.

2. Find a broker

Find a broker or brokerage with experience in pre-construction. Look for a broker that has Platinum Access to upcoming projects. Although no single broker has Platinum Access to every project, brokers often share units between each other. You can apply for the Platinum Stage of many different projects through a very well-connected broker.

3. Find a property

Tell them what location you want to live in so they can focus on projects in that area. You can then further narrow your choice down by giving them certain specifications like the square footage, building features, etc. This will help your broker find a condo project that suits you.

4. Sign a purchase agreement

Sign a contract that gives you future ownership of the condo unit once the building is registered with the city. You will most likely have to make a $5,000 down payment at signing as well.

5. Setup financing

10 days after signing the contract, you will have to pay an initial down deposit to secure your unit. This initial deposit is part of your total down payment and is usually 5% of the condo unit price. You will also need to get pre-approved for a mortgage loan. Banks will only guarantee the mortgage principal amount, so you will have to wait until about 3 months before the closing date before you can lock in a mortgage rate.

6. Make your payments

Continue to make deposits. While you are given the key, you still do not own the unit. However, you can live in the condo unit during the occupancy period and with the builder’s permission, you can also rent out the unit to someone else. At this point, you do not make mortgage payments, but you will have to pay monthly occupancy fees.

7. Take assignment of the property

Once the building is completed, pay the final closing costs and start making monthly mortgage payments. At this stage, the ownership is transferred to you and it is officially your property.

Some Neighbourhoods Have Monthly Rental Income Growing over 50% in 5 Years

What are occupancy periods and occupancy costs?

Since you are buying an unbuilt condo unit, the developer needs time to finish the project. You receive ownership of the unit when the building is completed and registered with the city, but you can move in about 3-6 months before this date. This period is called the occupancy period or the interim-occupancy period.

The occupancy period starts when your municipality declares the building as “fit for occupancy”. During this period, you live in the unit without owning it. With the builder’s permission, you can also rent this unit out to tenants. The occupancy period typically lasts for 3-6 months, but is shorter if you live on higher floors since these units are constructed last.

During the occupancy period, you will also be required to pay occupancy costs or interim occupancy fees, which are monthly payments to your developer. You are effectively renting the unit from the developer until you receive ownership. You can use your tenants’ rent to cover this fee if you rent the unit out. The Condominium Act prohibits developers from profiting using this fee, but you can still profit by collecting rent payments. Any interest earned on this fee is paid back to you and taxes are calculated after consideration for any amount repaid. Generally, you can expect to pay an occupancy fee close to interest payments on a mortgage plus any municipal taxes or condominium fees.

Example

If you had a mortgage on a $400,000 unit and you have already made a 20% down payment, then your occupancy costs would approximately be the mortgage interest paid on a $320,000 mortgage. The property taxes on a condo in Toronto will cost you roughly .66% per year or .055% per month. On the same home from the example, this would amount to $220 per month. Condo maintenance fees vary depending on your building, but the average condo fee in Toronto is about 60 cents per square foot. However, you may be charged a much higher fee for high-end condos. These are required to keep essential services running in the condo even during the construction phase.

Top Pre-Construction Builders in Toronto

Who are the top pre-construction developers in Toronto?

There are hundreds of condo developers in the GTA. There are not many major differences between developers. There are no limitations or guidelines on how to build condos. Instead, it is best to look at a developer’s past projects. This will give you a good indication of the quality and prices of the condo units. Large and experienced developers will also have higher quality buildings because of their resources and experience. The top 6 developers in Toronto are: Tridel, Concord Pacific, Daniels, Great Gulf, Menkes, and Pinnacle International.

Daniels

Daniels was founded in 1983 by former Cadillac Fairview executive, John H. Daniels. Since its inception, the company has developed more than 35,000 units. The Daniels Corporation has also funded Toronto Taste, and holds the record for largest land donation to Habitat for Humanity in Canada.

- Daniels FirstHome™: Some developments from Daniels are considered FirstHome Communities. These neighbourhoods offer a gradual deposit payment plan. Instead of needing a 5% down payment when you initially register for the building, you can make gradual payments. This allows you to get on the property ladder sooner without waiting for a sufficient down payment first.

OMG2

Mississauga Rd & Olivia Marie Rd, Brampton

Building Type: Low-rise Condo

Sales Started: February 2022

Selling Status: Preregistration

Builder(s): Daniels

Down Payment: 10%

Regent Park (Phase 3)

365 Parliament St, Toronto

Building Type: High-Rise Condo

Sales Started: Fall 2022

Selling Status: Preregistration

Builder(s): Daniels

Oakville Yards

Trafalgar & Dundas St East, Oakville

Building Type: Condo

Sales Started: Fall 2022

Selling Status: Preregistration

Builder(s): Daniels

Tridel

Tridel is the largest developer of condominiums in the Greater Toronto Area Housing Market. The company was founded in 1934 and has built over 85,000 units across 500 employees. In 2004, Tridel introduced LEED technology into all their developments and has now built over 20% of LEED-certified commercial buildings in Canada.

MRKT Alexandra Park

Denison Avenue & Dundas Street West, Toronto

Building Type: Condo

Units: 175

Sales Start: Winter/Spring 2021

Selling Status: Preconstruction

Builder(s): Tridel

Est. Completion: 2024

Westerly Condos

25 Cordova Avenue, Toronto

Building Type: Condo

Units: 257

Sales Start: Winter/Spring 2021

Selling Status: Preconstruction

Builder(s): Tridel

Est. Completion: 2025

Great Gulf

Great Gulf is the residential development arm of the Great Gulf Group, which also owns the Taboo Resort in Muskoka, Ontario. Great Gulf was founded in 1975 when they developed a small lot in Cambridge, Ontario. Since then, Great Gulf has built over 85,000 homes. Most notably, Great Gulf is the developer behind One Bloor in Toronto, which is the 2nd largest residential building in Canada and 40th in the world.

411 King St. West

411 King St. West, Toronto

Building Type: Condo

Units: 615

Sales Start: Spring/Summer 2021

Selling Status: Registration

Builder(s): Great Gulf and Terracap

Est. Completion: 2024

The Claire Residences

1421 Yonge St., Toronto

Building Type: Condo

Units: 198

Sales Start: TBA

Selling Status: Registration

Builder(s): Great Gulf and Terracap

Est. Completion: 2024

Menkes Developments

Menkes was founded by Murray Menkes in 1954. Menkes began with developing small single-family homes and grew to large-scale condos and offices across Canada. Some of the firm's notable developments include the Four Seasons Hotel and Sun Life Financial Tower in Toronto. As of 2013, they had developed over 15,000 homes.

The Whitfield

180 Front Street East, Toronto

Building Type: High-Rise Condo

Units: 470

Sales Start: Fall 2021

Selling Status: Registration

Builder(s): Menkes & Core Development

Est. Completion: Spring 2025

Adagio Condos

771 Yonge Street, Toronto

Building Type: High-Rise Condo

Units: 202

Sales Start: Fall 2021

Selling Status: Registration

Builder(s): Menkes

Est. Completion: TBD

Pinnacle International

Pinnacle focuses on developing luxury condos, hotels and office space across the GTA, San Diego and Vancouver housing markets. Pinnacle International is also the developer behind One Yonge Street, which is the Toronto Star newspaper office.

SkyTower

1 Yonge Street Toronto

Building Type: High-Rise Condo

Units: 834

Sales Start: 2021

Selling Status: Selling

Builder(s): Pinnacle International

Est. Completion: Nov 2024

Gemma

15 Watergarden Drive, Mississauga

Building Type: High-Rise Condo

Units: 406

Sales Start: Winter 2021

Selling Status: Selling

Builder(s): Pinnacle International

Est. Completion: Oct 2023

Finding a Pre-Construction Condo

How to find pre-construction condos

Developers have two main methods of distributing their units:

- Brokers: Developers will distribute their units to real estate brokers who sell these units to home buyers.

- Brokerage Firms: Developers may partner with brokerage firms who advertise the projects and sell units through their brokers. Some large developers may even use their own real estate teams.

Units are typically distributed in 4 stages, but this can change between projects:

| Stage | Accessibility | Duration |

|---|---|---|

| The Friends and Family Stage | Private | Developer’s Discretion |

| The Platinum Stage | Platinum Level Brokers | About 2 - 3 Weeks |

| The VIP Stage | VIP Brokers | About 3 months - 2 Years |

| The Public Stage | Public | Indefinite |

1. The Family and Friends Stage

During this unofficial stage, developers give the first 10-12 units to personal connections at a discount. The duration and timing of this stage is decided entirely by the project developer.

Price: Highest Discount

The price at the Family and Friends Stage is discounted at the developer’s discretion. Developers test market conditions by using these units to determine what prices should be set at later stages.

Access: Exclusive

The Friends and Family Stage is private. It only includes certain VIP real estate brokers, employees, project contractors, and the developer’s family and friends.

2. The Platinum/VVIP Stage

At the Platinum Stage, also known as the Very Very Important Persons (VVIP) stage, developers issue units to Platinum Level brokers or VVIP agents. This is the most sought-after stage because home buyers receive a generous discount. Typically, this stage lasts a couple of weeks, but it is up to the developer’s discretion. Developers typically release about 10-50% of their inventory and brokers have as short as a few days to distribute units to their clients. Once the project is launched, home buyers must finalize their deals within a short period of time.

Price: 3-8% Discount

Condo units at the Platinum Stage are generally cheaper because the project is still in its early phases of being sold. The lower price is the most attractive feature of buying a condo unit at the Platinum Stage.

Access: Very Limited

The Platinum Stage is limited to the developer’s network of about 10-50 real estate brokers (20 on average). Considered Platinum Level, these real estate brokers have pre-existing relationships with the developer. To buy a pre-construction condo unit at the Platinum Stage, contact a broker with Platinum Access. Developers also share units between each other, so a well-connected broker can have access to many more Platinum Stages.

3. The VIP Stage

The Very Important Persons (VIP) Stage is the last private round of offerings to home buyers and usually lasts between 3 months and 2 years at the developer’s discretion. Developers will release about 50-100% of their inventory. Condo units often sell out by the end of this stage. There are usually incentives associated with units sold during the VIP stage.

Price: Limited Discount

The VIP Stage offers a smaller discount than the Platinum Stage. Developers will also periodically increase the price at their discretion. The primary benefit of getting access at the VIP stage is that you can buy units before they are publicly available.

Access: Available

Real estate brokers have access to the VIP Stage if they have sold for the developer before. Condos are sold on a first-come, first-serve basis through brokers and brokerage firms. You can buy a pre-construction condo at the VIP stage by speaking with any real estate broker with VIP Access.

4. The Public Stage

Any units that have not been sold during the previous 3 stages are sold during the Public Stage. Developers will list units on their websites, but brokers can help you find the best units and search for other projects at the Platinum Stage or the VIP Stage.

Price: Full Price

This is the most expensive stage to buy a pre-construction condo. Developers may still increase or decrease the price at their discretion, but this is generally the final unit price.

Access: Widely Available

Units are available to the general public. Home buyers can see units specifications and prices directly on the developer’s websites. You can also talk to a real estate broker that can help you find the best deals and options.

How to pick a pre-construction condo

When looking at different units, you should consider multiple factors. There is little risk associated with getting a unit, but the quality of your unit can vary. Here are some things to consider:

What to look for

- Affordability: While condos are cheaper than freestanding units, buying one in Canada is still a significant purchase. You should make sure you have enough saved for deposits and that you can afford a mortgage. Understanding how much you can afford will help you decide between different units.

- Good Developers: The developer behind the project should be a key factor in your decision. Ultimately, they have control over the construction over your unit, so you should make sure that the one you pick is good. Make sure that the developer’s past condos meet your standard, which includes everything from their finishes to the building design.

- Price vs Location: More popular locations are usually more expensive. The reputation of the developer will not affect prices, so consider the trade-off between a good location and the increased price.

What to avoid

- Past Cancellations: If the developer has cancelled projects in the past, the risk that they will cancel their current project is much higher. Even with deposit protection, you may still lose part of your deposit and you will have to find a new unit.

- Small/Inexperienced Developers: If you cannot find past projects of theirs, they may not have any. The risk of both a cancellation and the project turning out poorly increases if the developer does not have the resources or experience to guarantee a high-quality building.

- Previous Lawsuits: Check the developer’s history and avoid them if they have been sued because of their buildings. Lawsuits generally arise because developers fail to meet building expectations.

Financing a Pre-Construction Condo

How do pre-construction condo down payments work?

Down payments for pre-construction condos are not one-time lump sum payments like a regular mortgage down payment. Pre-construction down payments are usually split into 4 equal payments of 5% of the unit price with a $5,000 deposit at signing. Most projects will follow this general guideline, but it is entirely up to the developer.

- $5,000 when you sign your contract (If you cancel your contract within the cooling off period - 10 days, this is returned to you)

- 5% minus $5,000 within 30 days

- 5% within 3-6 months

- 5% within 9-18 months

- 5% during the occupancy period

This structure is not fixed and only a reference for home buyers. Developers may change the down payment requirements or reduce the frequency of payments as part of promotions. For example, a developer may say that for a limited time, the minimum down payment requirement is only 10% or that deposits are delayed by a month.

During the occupancy period, you will also be required to pay occupancy costs or interim occupancy fees (rent), which are paid on a monthly basis before you own the condo unit. These payments are determined by the developer and are effectively rent payments that let you live in the unit until ownership transfers to you. The Condominium Act prohibits any profit-seeking activities using this fee, so you are not paying any extra money to the developer.

How to sell pre-construction condos

There are two ways to sell your pre-construction condo unit. The method that you use depends on the timing of your sale.

1. Sell the Condo Assignment

Before you own a condo unit, you enter into an agreement of purchase that gives you ownership when the building is completed. At this point, you do not own the condo unit, but you are given a unit assignment (future ownership of a specific unit). You can sell this to another home buyer, which gives them the future ownership and payment obligations associated with the condo unit.

2. Sell the Condo After Taking Ownership

When the occupancy period ends, the developer will register the building with the city. A date and time is then set that determines when you can transfer ownership of the property. The key difference is at the time of sale, you own the property and are selling a personal asset.

Depending on how you sell your unit, you may have to pay more taxes or you may be eligible for a tax rebate. If you have any questions regarding HST taxes, Capital Gains taxes, or Selling Your Unit, speak with your real estate broker.

What if pre-construction condos are cancelled?

In rare cases, a developer might not finish the condo project even though you have already bought a pre-construction condo unit. If this happens, your deposit is partially protected.

Tarion Deposit Protection

Tarion is a not-for-profit organization established by the Ontario Government that protects home buyers. Their deposit protection insures deposits if your purchase agreement is terminated by the builder. This includes if the developer goes bankrupt, they fundamentally breach your purchase agreement, or you have a statutory right to treat your purchase agreement as terminated.

Your deposit must be returned within 10 days following the termination of your agreement by the developer. If it is not returned, Tarion provides deposit insurance of up to $20,000. In this case, you must contact a lawyer to submit your claim.

Pros & Cons of Buying Pre-Construction Condos

Advantages

- New Home: Since you are buying the condo before it’s built, your condo unit is brand new. It will be equipped with advanced technology and building systems that make your living experience more comfortable.

- Extended Deposit Structure: The deposits for a down payment are spread over several months.

- Discount: You can get discounts and incentives at the Platinum Stage and the VIP Stage.

- Today’s Prices, Tomorrow’s Value: The condo unit is priced using today’s market value. However, during construction, your condo may appreciate in value, providing you with home equity.

- Flexibility: Typically, you can select between different unit packages. Some developers also allow customizing the unit with different finishes or upgrades, however, these are much more expensive.

- Urban Location: Pre-construction condos are usually located in dense cities with plenty of opportunities. Condos are the only way to reasonably live in these areas and pre-construction condos get you a premium spot.

Disadvantages

- Blind Purchase: You are buying property before it is built. You can only use the developer’s past projects as a frame of reference.

- Delays: Construction of any kind usually faces many delays. You should expect your condo to be finished later than planned.

- Interim-Occupancy Living: During the occupancy period, you are required to live in a building that is still being constructed.

- Cancellation Risk: In rare cases, the developer might be unable to finish a project. You will lose your unit assignment and you may lose part of your deposit.

- Future Mortgage Rates: Your mortgage starts when the building is finished, so you must use future mortgage rates. Banks can only guarantee the mortgage principal amount. The interest rate can only be locked for 3 months before the closing date.

Pre-Construction Condo Purchase Costs and Fees

Pre-Construction Condo Closing Costs

Average Cost per Square Foot in Toronto (2019)

| Pre-Construction: $967 |

| Resale: $737 |

Real estate investments and transactions will often have many closing costs that aren’t included in the sticker price or market price of the property. These costs will become due on your closing date or when ownership of the property is transferred to you. You should be made aware of this date when the builder notifies your lawyer and you should inform your mortgage lender as well. There are no clearly defined rules for pre-construction condo closing costs because you may have to pay different amounts or different costs depending on your unit and building. However, for the average 2021 pre-construction condo in Toronto, expect closing costs to total at least 10% of the purchase price. While closing costs cannot be summarized into one percentage of the purchase price, many common closing costs are shared among pre-construction condo purchases.

Statement of Adjustments

Many home buyers will be caught off-guard by the closing costs because they differ from regular buyer closing costs. One notable difference is the “Statement of Adjustments”. This is a key document that highlights any financial considerations for your condo unit incurred throughout the construction process. Among other things, this includes:

- Adjustments for property tax payments

- Adjustments for condominium fees

- Construction changes (expenses incurred due to a request for your unit to be customized)

Any condo-related fees that you have overpaid for will be subtracted from the purchase price and any fees that the builder was responsible for would be added to the price. Contrary to common belief, any extra fees you pay should have been included in your previous payments, and any fees you receive already belong to you, so you aren’t paying extra or getting a discount. The “Adjusted Purchase Price” is the purchase price that accounts for any fees over or underpaid by either you or the developer, so it is the fair price of your unit. If there are any fees that you do not recognize, consult your real estate lawyer who can explain them to you in detail.

Development Charges

Development charges or development levies are by far the largest fee that home buyers should expect to pay. These are charges levied upon condominium developers by the municipality (Toronto) when the builder receives a building permit. Developers will usually include this charge as part of your closing costs and it could cost you about $60,000 in the GTA, which amounts to approximately 11% of the total purchase price. While development charges are cheaper for condo units, they are the largest financial consideration that many home buyers fail to account for. In recent years, development charges have increased rapidly as cities look for new sources of income. Development charges can be broken down into multiple separate levies all paid to your municipality. These include:

- Education Levies

- Zoning Approval Levies

- Public Art Levies

- Park Levies

- Other Municipal Levies

Land Transfer Tax

In Toronto, you are required to pay a land transfer tax when transacting property. In the case of a condo unit, this burden will usually be placed upon you (the buyer) and stands to be one of the largest charges during the closing process. In Toronto, there is a 1% provincial transfer tax and a 1% municipal transfer tax. As your home price increases, the marginal transfer tax rate increases as well. You should expect to pay more than $10,000 for the land transfer tax and much more for high-end condo units.

Recurring Fees

Upon closing, you should be ready to pay the first payment of any recurring condo-related fees. For example, you will be required to pay maintenance or condo fees that could cost you about $500 per month. You will also be required to pay property taxes, which would cost you upwards of $300 per month on the average pre-construction condo unit in Toronto. These recurring fees must be paid periodically as long as you own the unit, but upon closing, you should be ready to make your first payment. In the case of property taxes, developers are allowed to request up to 2 years of property taxes to be paid in advance upon closing. While this amount is eventually given to your municipality, the large lump sum payment could catch you off-guard during closing.

Legal Fees

In Ontario, real estate transactions require that you have a lawyer who handles the closing process. This expense is not unique to condos and finding the right lawyer can be quite beneficial. Your lawyer will handle all the paperwork related to buying the unit and getting a mortgage. The exact fee varies between lawyers, but you can expect to pay about $2,000 in legal fees. If you are new to buying pre-construction condos, finding a good lawyer is much more important than finding a cheap one. When searching for a lawyer, you should ensure that they have experience with pre-construction units so they can help you navigate through the different procedures and regulations. Their expertise in handling the transaction and ability to guide you through could save you much more than any additional amount you have to spend to get quality legal assistance.

Tarion Warranty

In addition to Tarion’s Deposit Protection, Tarion provides several protections following the Ontario New Home Warranties Plan Act. Tarion helps pre-construction home buyers and developers resolve disputes and fix issues. The Ontario New Home Warranties Plan Act provides protection for only new homes and not homes that have been previously renovated or occupied. It also does not cover issues that arise due to regular usage of the home, third-party damage, or poor maintenance. The three types of warranties are issued for one, two, and seven years, which also includes deposit protection and delayed closing compensation (payment for closing falling behind schedule). The first warranty (1 year) protects home buyers from construction malpractice and defects, unauthorized substitutions, and inhabitable circumstances. The second warranty (2 years) protects against defects and violations related to the Ontario Building Code, which addresses health and safety. The third warranty (7 years) protects home buyers from major structural issues. Warranty protection can be used for up to $300,000, but the Tarion Warranty fee is just $385-$1,500 depending on the home price. This fee includes all three warranties and additional protections. Generally, the developer will automatically pay for Tarion warranty protection and the fee will be factored into the unit purchase price.

HST*

HST is usually included in the purchase price and will be rebated in the form of a price discount if you either move into the unit yourself or someone in your immediate family moves into the unit as their principal residence. If you plan on renting out the unit or holding the property as an investor, you are ineligible for any HST rebates, but you can get an HST New Residential Rental Property Rebate.

CMHC Insurance Premiums*

If you make a cumulative down payment of less than 20% (spread out throughout construction) once the closing date arrives, you will be required to pay for CMHC mortgage insurance, which protects your lender in case you default on your mortgage payments. In many cases, this fee is included in your mortgage, but you should keep it in mind. For most pre-construction condo developments, your unit assignment is contingent on being able to make a cumulative down payment of 20%, so you will probably not have to worry about mortgage insurance.

Capping Closing Costs

If at all possible, you should get as many of your closing costs capped in the purchase agreement. Many of these costs are more than significant and in the case of development charges, surprise increases could be the difference between affording the property and defaulting on payments. Toronto changes its development costs regularly and in recent years, these costs have been rising rapidly. Many things can change while your unit is being constructed and by setting a maximum limit on closing costs, you limit your exposure to unexpected increases in your final expenses.

If you ever hear the term “hard cap” or “soft cap”, make sure that you opt for a hard cap on closing costs. A “hard cap” sets a maximum limit on the final amount of development charges while a “soft cap” only sets a limit on the increase in development charges. This means that even if you have a soft cap on your development charges, you could be responsible for paying the original development charge amount plus the full soft cap amount if the municipality increases development charges by this much.

HST Rebates

HST is included in the purchase price when you move into the unit or you get one of your immediate family members to move in for the first year. The GST/HST New Housing Rebate (NHR) lets you recover part of the HST tax in the form of a price discount. The full HST tax is 5% GST and 8% PST. For homes under $350,000, the rebate amounts to 36% of the GST tax and 75% of the PST tax (up to $30,000). For homes between $350,000 and $450,000, there is a sliding tax rate and for homes above $450,000, the rebate is a flat $24,000. If you sell the unit before the first year ends, the CRA requires that you repay the full HST rebate. To qualify, you must belong to one of the following categories:

- you purchased a new or substantially renovated house (building and land) from a builder

- you purchased a new or substantially renovated mobile home or a new floating home from a builder (this includes the manufacturer or vendor)

- you purchased a share of the capital stock of a co-operative housing corporation (co-op) where the co-op has paid tax in respect of a new or substantially renovated house

- you purchased a new or substantially renovated house from a builder where you leased the land from that builder under the same agreement to buy the house and the lease is for 20 years or more or gives you the option to buy the land

Source: CRA

Unfortunately, real estate investors will have to pay an additional HST tax on closing. In this case or if the developer does not include HST into the purchase price, you should expect to pay an average of 7.8% of the purchase price during closing for units under $350,000 or a fixed $24,000 for units over $450,000. Fortunately, you should be able to recover some of this cost from the CRA in no more than a month as long as you file for an HST New Residential Rental Property Rebate within 1 year and prove that you rent out the unit with a rental lease agreement. This serves as an incentive for the unit to be occupied, which is similar to a “vacancy cost” if you fail to find a tenant.

Maintenance fees are ongoing monthly expenses required to help the building and its essential services. While this fee does not exist if you purchase a standalone home, it is recommended that each month, homeowners set aside a sum of money for home maintenance and repairs. In a condo, this fee exists to make sure that every resident contributes their fair share to the proper maintenance and services of the building. Your monthly fee is used to pay for:

- Indoor and outdoor common areas

- Building maintenance and repairs

- Shared amenities available to all residents

- Building management and employees

- Certain utilities (can include hydro, water, gas, and more, but this varies between buildings)

- A required contribution to your condos reserve fund as per the Condominium Act

There are also optional monthly fees that would be added to your maintenance fee. These pay for certain amenities such as:

- Building parking ($50 - $100)

- Lockers ($15 - $25)

Make sure that your lawyer informs you of what your maintenance fee pays for because maintenance fees vary. On average, you should expect to pay 65¢ per square foot in the GTA, which will cost about $500 per month for a normal condo unit.

During the first two years following construction, the developer pays for any budget deficiencies, but after these two years, residents take responsibility for this extra expense. You should expect your maintenance fee to increase by 10-20% after your first two years of residence. You should also expect maintenance fees to increase over time as the building accumulates higher costs.

Investing in a Pre-Construction Condo Unit

Pre-Construction Units as an Investment

In North America, Toronto is one of the fastest-growing cities and currently the 4th most populated city. Even with continuous condo construction, the housing demand of Toronto far exceeds the speed at which condos are being built. This means that demand outweighs supply, and real estate prices have been rapidly increasing, which makes condos seem like the only source of affordable housing.

While pre-construction condo units are a good investment, buying a condo unit yet to be constructed should be seen as an investment rather than a living arrangement. Investing in pre-construction condos carries a large amount of risk that buying a unit of residence outright does not. For example, developers can cancel projects, change the design, and will inevitably delay construction. Pre-construction condos should not be considered reliable future housing and if you decide to purchase a pre-construction condo unit, you should ensure you have stable housing elsewhere for the foreseeable future.

Pre-Construction Condo Market Overview

Much like the rest of the real estate market, the pre-construction condo market operates as a function of supply and demand. When demand is low and supply is high, prices are low. When demand is high and supply is low, prices rise as is the case in Toronto. Toronto is the second most expensive city in Canada next to Vancouver. Condos are no exception as their easier accessibility in high-density and urban locations puts them in high demand. However, demand for condo units and pre-construction units spiked recently because of two major factors.

- COVID-19: COVID-19 caused governments to decrease interest rates to all-time lows. This made getting a mortgage significantly cheaper and gave home buyers much more buying power. Additionally, condo prices fell during COVID-19 by as much as 13% during the first quarter of 2020 as urban residents moved to less populated areas to work from home. With Toronto’s high real estate prices, many investors saw this as an opportunity to get some cheap property with a low-cost mortgage and condo prices have once again begun increasing rapidly with the average sold price of a condo at $683,479 in June 2021.

- Population: Even in the face of COVID-19, the Canadian government is still committed to its goal of bringing more than 1.2 million immigrants by the end of 2023. This will significantly increase Toronto’s population and demand for real estate will follow. Toronto is a notorious seller’s market because of the high population density and the relatively slow rate of real estate construction. With the new immigrants and Toronto’s already high population growth of .93% annually, the housing shortage is expected to increase.

Toronto is known for having a low supply of new homes even with constant construction. With COVID-19 ending and employees returning to their offices, the demand surge will overwhelm the capacity of current pre-construction projects. In the fourth quarter of 2020, there were over 78,000 pre-construction condo units throughout all stages of development, but this is unlikely to match the impending demand increases. Pre-construction condo unit prices will likely continue to rise throughout 2022.

Financing a Pre-Construction Condo Purchase

Nearly everyone who buys a pre-construction condo unit will need to finance their purchase with a mortgage. By using a mortgage to buy a pre-construction condo, you can invest in this asset and take advantage of rising real estate prices. Current mortgage rates are at all-time lows with the lowest 5-year fixed mortgage rate in Canada at 2.43%. However, buying a pre-construction condo is a heavy financial burden and there are many things you should consider when making the purchase.

- Minimum Down Payment: While many mortgage programs reduce your minimum down payment to as low as 5%, with a pre-construction condo unit, you will have to make a minimum down payment of 20% in most cases by the time construction is completed. Fortunately, the down payment is spread out over multiple payments and the property is priced at today’s fair market value. By the time you finish making your down payments, the house will have appreciated and you can benefit from the profits.

- Mortgage Pre-Approval: Most pre-construction condo developments will require that you get pre-approved for a mortgage if you want to secure a unit assignment. This gives the developer some guarantee that you will follow through with the unit purchase, and have the required mortgage documents. If the developer has sold most of the units and has enough people financing the construction, developers may allow you to get a unit without a pre-approval.

Generally, developers will request mortgage pre-approvals within the first 30-90 days after signing your agreement, but you should aim to secure financing within the 10-day cooling-off period. This way, you can back out of the purchase if you have trouble with your finances. To receive a mortgage from a Canadian lender you will need to prove you have condo insurance.

- Credit History: One of the most important things lenders will look at is your credit history. Past payments and debt obligations demonstrate how much of a credit risk you are going forward. You should regularly maintain your credit score because many lenders and mortgages have minimum credit score requirements. Generally, you need a minimum credit score of 600 for most banks, 550 for B-lenders, none for private lenders, and 600 for CMHC insured mortgages. However, you should aim for a credit score above 680 for better mortgage rates, which is considered good, and above 760 to get the lowest mortgage rates.

- Debt Service Ratio: Lenders will factor your Gross Debt Service (GDS) and Total Debt Service (TDS) ratio into your mortgage eligibility. These Debt Service Ratios help lenders determine how well you can cover your monthly debt obligations and affect your mortgage rate and eligibility. If you want to buy a pre-construction condo unit, you should ensure that you have paid off as many of your other debts as possible before applying for a mortgage.

Key Factors in a Pre-Construction Condo Purchase Agreement

Your purchase agreement (Purchase and Sale’s pre-construction Agreement) is the most important document to understand with a pre-construction condo unit. It covers your rights, the developer’s rights, your assigned unit, and the development. It highlights all your legal and financial obligations and protections. You should have your lawyer carefully review your purchase agreement and inform you of any relevant details. Namely, these are the most important things to look for in a purchase agreement:

- Unit price and deposit amount/details

- Possession date - when you receive ownership of the property

- Details about your assignment rights and limitations, plus any assignment-related costs

- Occupancy period details including if you have permission to rent out the unit during the occupancy period and the occupancy fees

- Caps on various closing costs and utility installments

- Administrative fees

- First-year maintenance fees

- Contingencies like a mortgage pre-approval

Frequently Asked Questions (FAQ)

Are pre-construction condos cheaper than resale condos?

With a pre-construction condo, you’re purchasing a newer building in high-density areas. Therefore, pre-construction condo units will typically be more expensive than their resold counterparts. In the past, pre-construction condo units were cheaper because of the risk that the development would be delayed or canceled, but with rising demand for housing, pre-construction condo home prices have surged. In 2019, the average price per square foot of a pre-construction condo unit was 30% higher than the price per square foot of a resale unit. However, there are some price benefits because you can avoid bidding wars for pre-construction units. With high demand for Toronto real estate, bidding wars often break out over properties, but with a pre-construction unit, you buy the unit at the sticker price (the price quoted by the developer).

Can I customize a pre-construction condo unit?

Approximately one year before construction is completed, you can customize your unit for an added cost. You can adjust your unit’s finishes and colour schemes, but you can make structural changes as well. This includes flooring, window blinds, cabinets, appliances, countertops, and lighting. You can even go as far as to remove a wall if your builder allows it. While these upgrades will cost you much more than regular renovations, they provide the flexibility to add value as you see fit.

Will my actual unit be the same as the floor plan?

During construction, developers will often make changes to your unit that stray from the original floor plan without notice. For example, they could add support pillars, shafts, or layout changes that affect your unit size and shape. The extent to which developers can change your unit is highlighted in your purchase agreement. Ask your lawyer to explain what changes could be made as the terms used in your contract may be loosely defined.

Can I cancel my purchase agreement?

Within the first 10 days, you can cancel your purchase agreement without penalty during the “cooling-off period”. By providing written notice of your intent to cancel your Purchase Agreement, your builder or lawyer will cancel it. Unfortunately, after these 10 days, you may face serious consequences for canceling your purchase agreement. It is a legally binding contract and not adhering to it could cost you your deposit and you could even be sued by the developer.

What are pre-construction incentives?

To encourage buyers to purchase their pre-construction units, developers and brokers may offer incentives to buyers that add value to the unit or the purchase process. This can include different deposit structures (extended or reduced), discounts on parking and storage lockers, free unit assignments, or reduced assignments fees. There is a broad range of incentives that vary depending on the building, but they should not be the only consideration. If incentives are being offered, there is likely some reason that the developer was unable to sell their units.

What if I miss a deposit?

If you miss a down payment deposit, your purchase agreement should highlight exactly what happens. In most cases, if a cheque bounces, you should be given a certain amount of time to submit a new cheque. If you miss a down payment and you do not settle your account, then you have violated your contract, which means your developer can reclaim their unit. In any case, you will likely face a penalty of between $300-$500 if you fail to make a payment on time.

Do I receive interest on my pre-construction deposit?

The Condominium Act states that developers must pay interest on any deposit amounts paid by you, the buyer. This serves as an incentive for builders to complete their projects on time and to avoid delays. Interest starts accruing as soon as the developer receives the money. Unfortunately, this interest rate is set at “2% per annum below the bank rate”. With a current Bank of Canada rate of 0.25%, the interest rate you “earn” is 0%. You should not expect to earn any interest on your deposits as the bank rate has not been above 2% since 2008.

Information displayed is for reference only. WOWA Leads, Inc. does not guarantee the accuracy of our information and is not liable for its use or misuse. Illustrations are artist’s concepts and may not be representative of the final product.

The calculators and content on this page are provided for general information purposes only. WOWA does not guarantee the accuracy of information shown and is not responsible for any consequences of the use of the calculator.